Paying yourself dividends is a cornerstone of running a tax-efficient UK limited company, but it’s a process that needs to be handled correctly. It's not just about transferring cash; it’s a formal procedure that involves confirming your company has enough distributable profits, holding a board meeting to declare the dividend, and creating the right legal paperwork.

Following this structured approach is key to maximising your take-home pay while keeping everything above board with HMRC.

As a limited company director, getting to grips with how to pay yourself dividends is far more than just moving money from the business account to your personal one. It’s a fundamental part of a smart remuneration strategy, usually blending a small salary with dividend payments to lower your overall tax bill.

Here’s the critical distinction: a salary is a business expense, but a dividend is a distribution of profits to shareholders after the company has paid its Corporation Tax.

This means you can't just pick a number out of thin air and pay it out. Any dividend has to be funded by your company’s retained earnings—that’s the accumulated profit left in the business after all expenses and tax liabilities have been sorted.

The absolute foundation of paying any dividend is having enough distributable profits. If you don't, any payment you make could be flagged by HMRC as an 'illegal dividend,' which can lead to some serious headaches.

And this isn't about how much cash you have sitting in the business bank account. It’s all about the profit shown on your company's balance sheet.

To stay compliant, you must tick these boxes:

This careful calculation protects both you and your business by ensuring you’re not taking out more money than the company has legitimately earned. The scale of this is huge; UK companies paid out a staggering £94.3 billion in dividends in a recent year, which just goes to show how central this method is to the UK economy.

Key Takeaway: Always base your dividend payments on your company's retained earnings, not its bank balance. Keeping accurate, up-to-date accounts isn't just good practice—it's non-negotiable for making this decision correctly and avoiding penalties.

For most company directors, the most effective strategy is taking a small salary topped up with dividends. The salary is usually set at a level that qualifies you for National Insurance credits without triggering a big tax bill. Any further income is then drawn as dividends, which, crucially, are not subject to National Insurance contributions.

This blended approach is a cornerstone of tax planning for limited companies and ensures you get to keep more of your hard-earned money.

The main reason company directors favour a dividend-and-salary mix over taking a straight salary boils down to one powerful factor: tax efficiency. When you get the structure right, this approach can seriously reduce your personal tax bill, leaving much more of your hard-earned money in your pocket.

It all comes down to how HMRC treats each type of income, and the big difference is National Insurance.

A salary is subject to both Income Tax and National Insurance Contributions (NICs) – not just for you as the employee, but for your company as the employer, too. Dividends, on the other hand, are not subject to National Insurance at all. This single distinction creates a substantial tax saving right from the start.

Every UK taxpayer gets a Dividend Allowance each year. Think of it as a tax-free head start on your dividend income. It's a specific amount you can receive without paying a penny of tax on it, no matter what your other income is.

The exact allowance can change from year to year, but making full use of it is a cornerstone of any good tax-planning strategy. For the latest figures, check out our complete guide to the UK Dividend Allowance. Using this allowance means the first chunk of profit you take from your company costs you nothing in personal tax.

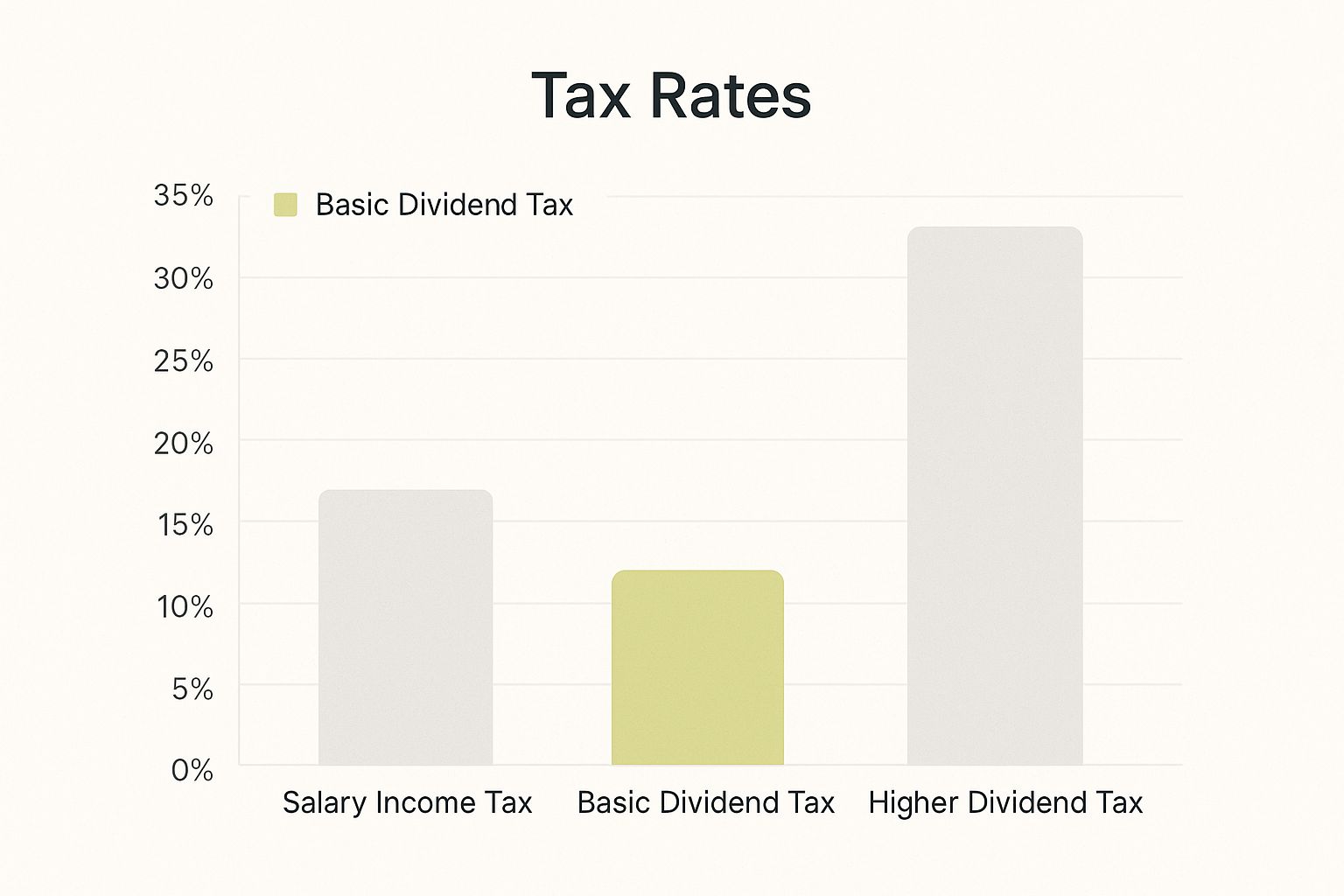

Beyond the tax-free allowance, the tax rates on dividends are simply lower than the rates on salary income across every tax band. Once you've used up your Dividend Allowance, the tax you'll pay is 8.75% for basic rate taxpayers, 33.75% for higher rate, and 39.35% for additional rate taxpayers.

Let's put that into perspective by comparing it directly to the tax paid on salary.

The table below gives you a clear, side-by-side look at just how different the tax rates are for salary income versus dividend income. The savings become obvious very quickly.

As you can see, the dividend tax rate for a basic rate taxpayer is less than half the equivalent income tax rate on a salary. The benefits continue even as you move into the higher tax bands.

Let’s look at how this plays out in the real world.

Real-World Scenario: Sarah the Consultant

Sarah runs a successful consultancy as a limited company and needs to take £50,000 out of the business.

- Option 1 (Salary Only): If she takes the full £50,000 as a salary, she'll face a hefty bill for Income Tax, plus both employee and employer National Insurance.

- Option 2 (Salary + Dividends): Instead, she pays herself a small salary up to the National Insurance threshold (£12,570), which means no tax or NI is due on it. The remaining £37,430 is drawn as dividends. She uses her tax-free Dividend Allowance first, then pays the lower basic rate dividend tax on the rest.

The result? Sarah's take-home pay is significantly higher with the second option. The savings from avoiding National Insurance and taking advantage of the lower dividend tax rates really add up.

To see how the numbers could look for your own situation, it's worth plugging your figures into a dividend tax calculator to model a few different scenarios.

Before you even think about paying yourself a dividend, there's a critical question you need to answer: how much profit is actually available to distribute legally? This isn't just about glancing at your business bank account balance. It's a specific calculation based on your company's retained earnings.

Retained earnings are the cumulative profits your company has built up over time, after you’ve already paid out any previous dividends. Think of it as the reservoir from which all future dividends must be drawn. Taking out more than this amount is what HMRC calls an 'illegal dividend,' and that can land you in serious hot water.

To work out the exact amount you can take, you need to get familiar with your company's latest accounts—specifically the profit and loss account. Your starting point is the headline profit your business has generated.

But you can't stop there. From this figure, you have to subtract all of your company's liabilities and expected costs to get to the true distributable profit. This is much more than just your day-to-day running costs.

You absolutely must set aside money for:

When you're working this out, it’s also a good idea to make sure you're taking advantage of all available tax benefits, such as understanding offshore profits exemption claims. This just ensures your final figure is as accurate and efficient as it can be.

Once you have your final distributable profit figure, you face a big decision: how much of it should you actually pay out? While it’s tempting to take the lot, savvy directors often use a 'payout ratio' to strike a healthy balance between personal income and the company's long-term stability.

This ratio is simply the percentage of earnings you decide to distribute. For example, you might choose to pay out 70% of the profits as dividends and leave the remaining 30% in the business. This retained cash can then fund future growth, cover unexpected bills, or just provide a welcome financial cushion.

Expert Insight: Leaving a chunk of the profits in the business is always a smart move. It signals financial health to banks and investors and gives you the capital needed for new equipment, marketing campaigns, or hiring staff without having to borrow.

The average dividend payout ratio for UK-listed companies often sits somewhere in the 70-90% range, which shows that even the big players are constantly balancing shareholder returns with reinvestment. By adopting this same mindset, you're setting your company up to be more robust and ready for whatever comes next.

So, you've checked the numbers and confirmed your company has enough profit to pay a dividend. Great. But you can't just move the money from your business account to your personal one and call it a day.

To do this properly and legally, you need a clear and consistent paper trail. Think of this not as a chore, but as essential armour that protects both you and your company from any future questions from HMRC. This documentation is what proves the payment was a formal, deliberate distribution of profit to a shareholder—not just a random payment, a salary, or a director's loan.

Getting this right every single time is non-negotiable. Luckily, it’s a straightforward process once you know the steps.

Your first piece of the paper trail starts with a directors' meeting. Yes, even if you're the only director and shareholder, you need to hold a "meeting" to formally declare the dividend. It might feel a bit strange talking to yourself, but it's a crucial legal step.

The decision made in this meeting must be recorded in writing as board minutes. These minutes act as the official record that the company's directors have approved the payment.

Your board minutes need to include a few key details:

Keeping these minutes safely on file is your proof that you followed the correct procedure. Without them, HMRC could easily challenge the validity of the payment.

Next up, for every dividend payment made, you must create a corresponding dividend voucher. This is basically a receipt for the dividend, and each shareholder needs one for their personal tax records. It's the key document they’ll refer to when filling out their Self Assessment tax return.

The voucher is the final piece of evidence that connects the board's decision to the actual cash received by the shareholder.

Key Takeaway: Think of board minutes as the authorisation and the dividend voucher as the receipt. You absolutely need both for every single dividend payment, no matter how small. Neglecting this paperwork can turn a legitimate dividend into a compliance headache down the line.

A proper dividend voucher should clearly state:

Once the paperwork is sorted, the physical payment should be made from your company's bank account directly to the shareholder's personal account. If you’re still getting your finances in order, our guide on how to set up a business bank account is a great place to start. Keeping business and personal funds separate makes your financial records much cleaner and easier to manage.

Knowing how to pay yourself dividends correctly is a massive advantage for any director, but it’s surprisingly easy to make small mistakes that can land you in hot water with HMRC. Once you get the hang of it, navigating the rules is pretty straightforward, but you need to be aware of the common pitfalls.

Getting this right is all about keeping your financial affairs clean, compliant, and above reproach. Let’s walk through the errors I see most often.

This is the big one. The most critical mistake you can make is issuing an illegal dividend. This happens when you pay out more money than your company has available in distributable profits.

It’s a common misconception that if you have cash in the bank, you can pay a dividend. That’s not how it works. The decision must be based on the retained earnings shown on your balance sheet after all your liabilities—especially your Corporation Tax bill—have been accounted for.

If you take an illegal dividend, the payment is legally void. This isn’t just a slap on the wrist; it means you, the director, are personally required to repay the full amount to the company. HMRC can also launch an investigation, which could lead to penalties if they decide you should have known better.

Another frequent shortcut that directors take is skipping the paperwork. It’s tempting to just make a quick bank transfer and call it a day, but without the correct documentation, that payment isn't a legally valid dividend in the eyes of HMRC.

Every single dividend you issue must be backed up by two key documents:

If you can't produce this paperwork, HMRC has the power to reclassify the payment. Instead of a tax-efficient dividend, they might decide it was a salary, which would trigger unexpected PAYE tax and National Insurance liabilities. Not a fun surprise.

Expert Insight: Think of your paperwork as your first line of defence. If HMRC ever opens an enquiry into your accounts, having a complete and accurate record of board minutes and dividend vouchers for every payment immediately shows you’re professional and compliant. It can often stop an investigation in its tracks.

When you take money out of your business, clarity is everything. A common muddle happens when it’s not clear whether a payment is a dividend, a salary, or a director's loan. Each one has completely different tax implications, and blurring the lines can cause serious confusion and potential tax headaches down the road.

For instance, if you take regular, identical payments from the business every month without properly declaring them as dividends, HMRC could argue they're an undeclared salary. This is exactly why following the formal declaration process—board minutes and all—is so crucial. It puts a clear, legal label on the payment.

Keeping your financial records organised is a fundamental part of running a successful company. To help you stay on top of things, our guide offers some great tax advice for small businesses.

When you're trying to apply the dividend rules to your own business, a few common questions always seem to pop up. Let's tackle some of the most frequent queries directors have when figuring out how to pay themselves.

There's actually no legal limit on how often you can pay dividends. Unlike a rigid monthly salary, you can issue them quarterly, annually, or even ad-hoc whenever your company has enough profit. Some directors like the routine of a quarterly payment, while others might declare a larger one-off dividend after a particularly good project.

The real key here isn't the frequency, but the process. Every single dividend payment, no matter how small or how often, must be supported by sufficient distributable profits. It also needs to be properly documented with board meeting minutes and a dividend voucher each time.

An 'illegal' dividend is what happens when you take a payment that’s more than your company’s available distributable profits. The legal fallout is that the payment is considered void. In simple terms, this means the director who received it is personally liable to repay the full amount back to the company.

If HMRC ever investigates and finds that you knew (or really should have known) that the dividend was unlawful, it could lead to more serious scrutiny and potential penalties. This is exactly why keeping your accounts accurate and up-to-date isn't just admin for the sake of it—it's your best defence against making this kind of serious mistake.

While no law says you must use an accountant to handle dividends, it’s very strongly recommended. Think of an experienced accountant as a crucial safety net. They ensure your profit calculations are spot-on, so you aren't at risk of taking an illegal dividend by mistake.

But their value goes way beyond just compliance. A good accountant provides strategic advice. They can help you structure your total pay package—that mix of salary and dividends—for the best possible tax efficiency and make sure all your legal paperwork is watertight. Honestly, their expertise brings invaluable peace of mind and helps you sidestep some very costly errors.

Expert Insight: It’s actually possible to pay a dividend even if your company made a loss this financial year. Dividends are paid from your total accumulated profits, known as 'retained earnings,' which includes profits carried forward from previous years. So, if your company has a healthy pot of retained earnings from prior profitable periods, you may still be able to declare a dividend. Your accountant can confirm the exact figure from your balance sheet.

At GenTax Accountants, we specialise in helping UK directors handle these complexities with complete confidence. Our team makes sure your dividend strategy is both tax-efficient and fully compliant, freeing you up to focus on running your business. Get in touch with us today for expert guidance.