Opening a business bank account is one of those foundational moments for any UK entrepreneur. It's not just about ticking a box for compliance; it’s about drawing a clear line in the sand between your personal and business finances. This single step protects your personal assets, makes bookkeeping infinitely easier, and frankly, makes you look more professional from day one.

Trying to run a business out of your personal account? It’s a recipe for a headache, especially for limited companies where blurring those lines can put your personal assets at risk.

This guide is your complete roadmap. We'll walk you through everything you need to do, from gathering your documents to picking the right bank, so you can get it done right the first time.

Forget a dry list of instructions. We’re diving into the real-world practicalities of getting your account open. We'll cover the essentials:

Think of this as your personal checklist for getting your UK business bank account sorted. By the end, you'll know exactly what to expect, how to avoid common pitfalls, and how to get your business finances organised efficiently.

Whether you're a freelancer just starting out or a newly formed limited company, the core principles are the same. Let's get your business financially organised.

Before you even start thinking about filling in applications, it’s worth taking a moment to check you actually meet the bank’s eligibility criteria. It sounds obvious, but you'd be surprised how many people waste time applying to banks that would never accept them.

Each bank has its own set of rules, and these can change quite a bit depending on your business structure. Knowing what they're looking for upfront will save you a headache and the sting of an unnecessary rejection. Really, the first step in opening a business bank account is making sure you’re a good fit for the bank you have your eye on.

If you’re a sole trader, the process is usually the most straightforward. Think of a freelance consultant working under their own name. For you, most banks will focus on your personal details: being over 18, a UK resident, and your personal credit history.

Things get a bit more involved for a limited company. Banks will want to see that your company is properly registered with Companies House. They’ll also need the details of all directors and anyone who owns a significant chunk of the business (typically over a 25% stake). Every single director will need to prove their identity, address, and residency status.

The way your business is set up has a massive impact on what the bank needs to see. It’s all about risk and legal responsibility from their perspective.

Sole Traders: You are the business. This means the eligibility checks are all about you. A rocky personal credit history can be a hurdle, but don't lose hope—some of the newer digital banks are often more lenient.

Limited Companies: Here, the bank is dealing with a separate legal entity. You'll need your Certificate of Incorporation and Companies House number handy. All your directors must be ready with their personal ID. If you need a refresher on getting your business officially set up, have a look at our complete guide on how to start a business in the UK.

Partnerships: This is quite similar to a limited company. All partners will have to go through identity and residency checks. The bank will also ask to see your Partnership Agreement to get a clear picture of how the business is owned and managed.

No matter what type of business you have, a few things are always on a bank’s checklist. Your personal credit score often comes into play, even for limited companies. Banks see the financial habits of the directors as a clue to how stable the business might be.

Here’s a critical point: all key players in the business—directors, partners, or anyone with significant control—must be able to prove they are UK residents. Having non-resident directors can make opening an account with a traditional high-street bank a real challenge.

Let's imagine a new e-commerce business set up as a limited company. It has all its registration documents in order, but one of its two directors lives abroad. This is a classic stumbling block. Their best bet would be to skip the high-street banks and look directly at specialist international banks or modern fintech providers who are set up to handle these situations.

Knowing about these potential snags ahead of time means you can apply to the right places with confidence.

If there’s one thing I’ve learned from helping businesses get set up, it’s that a smooth bank account application comes down to one simple thing: preparation. Having all your documents ready to go is the single best way to avoid delays and frustration.

Think of it less as a chore and more as your business's first formal introduction to the bank. They aren't just being difficult for the sake of it; they are legally required to verify who you are and what your business does. This is all part of the UK’s anti-money laundering regulations, often known as Know Your Customer (KYC) rules. Showing up prepared proves you’re organised and serious.

First things first, the bank needs to know who you are. Every director, partner, or person with significant control (that usually means owning over 25% of the company) will need to provide personal identification. This part is non-negotiable.

For proof of identity, you’ll almost always be asked for one of these:

Next, you'll need proof of your address. This must be a recent document, typically issued within the last three months. Good examples include:

Insider Tip: Check that the name and address on your proof of address documents exactly match your application and your ID. I've seen applications get held up by something as small as "St." instead of "Street." These tiny discrepancies can trigger an automated rejection and cause a real headache.

Once they've confirmed who you are, the bank needs to verify your business as a legitimate, registered entity. The documents you'll need at this stage depend entirely on your business structure. With SMEs making up around 99.9% of the UK's 5.6 million businesses, banks are very used to this process.

If you run a limited company, you'll be asked for:

If you're new to this, getting your head around the initial registration can feel a bit daunting. It’s worth checking a breakdown of the current company registration fees in the UK to understand what’s involved in the official paperwork.

For sole traders, things are a bit simpler because you and your business are legally the same. You'll just need your personal ID and proof of address, plus your Unique Taxpayer Reference (UTR) number. It also helps to have proof you're actively trading, like recent invoices or client contracts.

In some cases, especially if you're applying for an overdraft or loan right away, a bank might ask to see a business plan or some financial forecasts. This is pretty common for new businesses without a trading history. Don’t panic – a simple forecast showing your expected income and major outgoings for the first 12 months is usually all they need.

Picking the right bank is far more than just finding a place to park your company's cash; it's a critical business decision. The right banking partner can make your day-to-day operations feel seamless, while the wrong one can introduce friction and a whole load of unnecessary costs. Ultimately, the best choice will hinge on your specific business model and how you handle money.

The UK banking scene is a crowded one, giving you plenty of choice between traditional high-street names, modern challenger banks, and slick digital-first fintechs. Each comes with its own set of pros and cons, and what works for one business might be a disaster for another.

If you run a brick-and-mortar retail shop, you'll likely be dealing with cash takings several times a week. For you, a traditional high-street bank is almost essential. The convenience of a local branch for depositing cash and getting face-to-face support is something digital-only banks just can't replicate.

On the flip side, imagine you're a freelance consultant or you run a remote-first software company. A digital challenger bank could be a perfect fit. They often come with brilliant mobile apps, smooth integrations with accounting software, and much lower fees for international payments—a massive win if you have clients or suppliers across the globe.

This move towards online options is no longer a niche trend. In fact, a recent study showed that 70% of business leaders are now happy to consider banks without any physical branches. It's a clear signal of how modern businesses are evolving their financial management.

Key Takeaway: Resist the urge to just default to your personal bank. Take a proper look at what your business actually needs—cash deposits, international transfers, software integration—before you commit. Your future self (and your workflow) will thank you for it.

When you're sifting through your options, try to look past the flashy introductory offers. What really matters are the core features and ongoing costs that will impact your business long-term.

Here are the main things to keep on your radar:

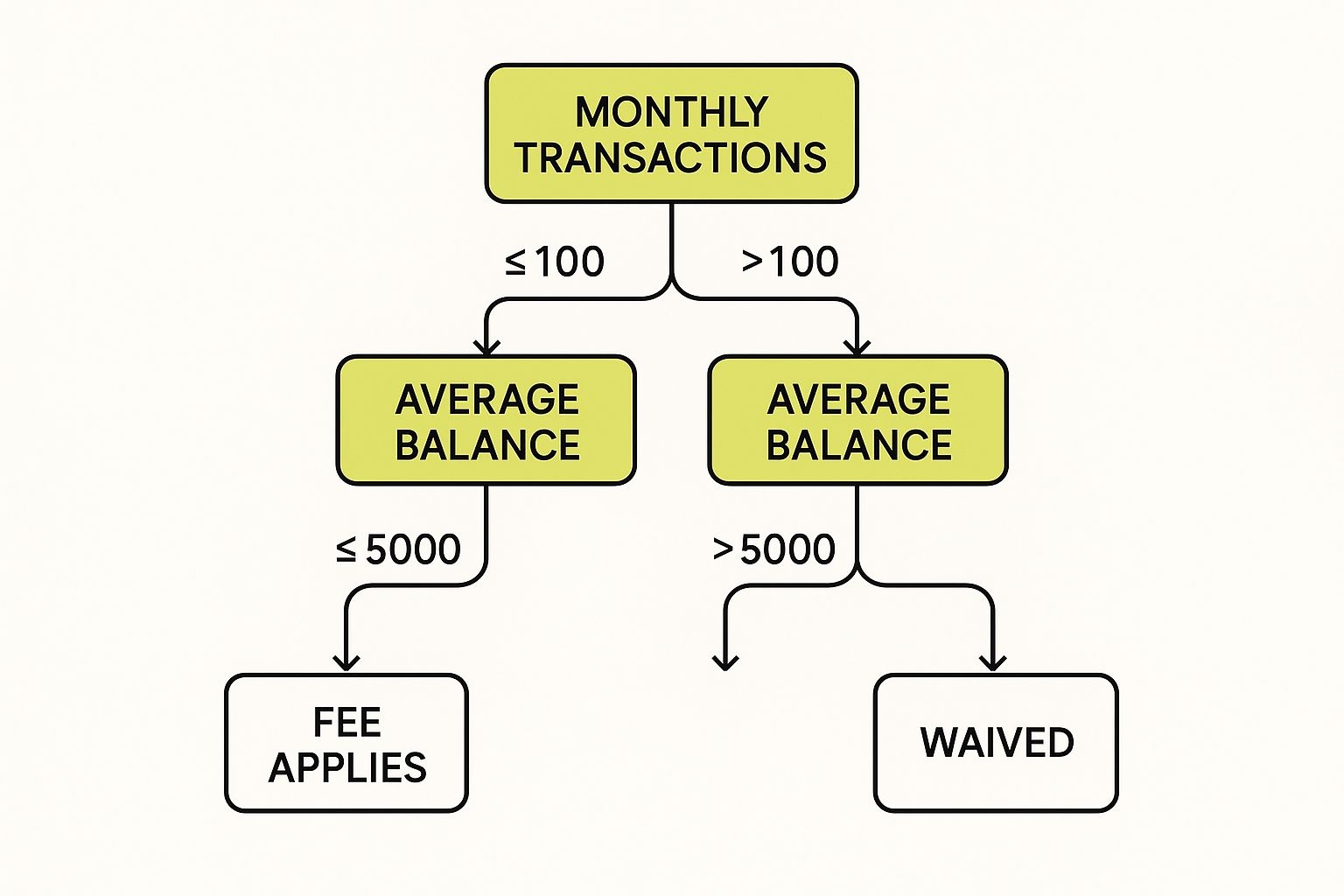

The chart below shows how small details like your transaction volume can be the tipping point between free banking and getting hit with monthly fees.

As you can see, crossing certain thresholds can mean the difference between paying nothing and racking up charges. That's why it's so important to have a realistic forecast of your business activity before you choose.

Alright, you’ve got your documents ready and you’ve picked a bank that feels like the right fit. Now for the main event: the application itself.

Whether you’re clicking through an online form or sitting opposite a bank manager, the basic journey is the same. You'll submit your details, the bank will do its checks, and then hopefully, you'll get the green light. The real secret to a speedy approval is giving them clear, accurate information that paints a professional picture of your business.

This is where a lot of applications stumble. When the form asks for a description of your business, be specific. “I sell stuff online” just won’t cut it and can raise compliance red flags. Instead, try something like, “E-commerce retailer of handmade leather goods, sold via a dedicated website and third-party marketplaces.” It sounds much more professional and leaves no room for doubt.

The same goes for your financial forecasts. When you’re asked to estimate your annual turnover, be realistic. It’s perfectly fine to provide conservative, sensible projections if you’re just starting out. Banks expect this. Wildly optimistic figures, on the other hand, will only invite more scrutiny and questions you might not be ready to answer.

Digital identity checks are another classic hurdle. Most online applications now ask you to snap a selfie and a photo of your ID on your phone. It sounds simple, but poor lighting or a blurry photo can get your application automatically rejected. Take your time, find a well-lit spot, and follow the on-screen prompts carefully.

If your limited company has a more complex ownership structure—think multiple directors, different shareholders, or even a parent company—be prepared for a longer wait. The bank has to perform its due diligence on every key person involved, and that naturally adds time to the process.

Expert Tip: If your application seems to have vanished into a black hole for more than a couple of days, don’t just sit and wait. Pick up the phone and call the bank’s business support team. A quick chat can often resolve a minor issue, like a typo in an address, that’s holding everything up.

As you work through the application, you'll be asked about how you expect money to move in and out of the account. This isn't just about your turnover; it’s about the bank understanding the rhythm of your business finances. They need this information to meet their legal obligations to monitor for unusual activity.

Get ready to answer questions like:

Being upfront with this information is also brilliant for your own planning. Keeping a clean record of your transactions from the start is vital, especially when you’re getting ready for digital tax reporting. You can find out more about what's involved in our guide to Making Tax Digital for Self Assessment.

Ultimately, being honest and clear at this stage doesn’t just get your account open faster—it builds a solid foundation for a good relationship with your bank.

Right, you’ve got your sort code and account number. Your business bank account is officially open. It’s a great milestone to hit, but the work isn't quite finished. Now’s the time to properly weave the new account into your day-to-day financial operations.

Taking a few proactive steps at this stage will save you countless hours and prevent a lot of headaches down the line. The goal is to make your financial admin as smooth as possible right from the start. This begins with hooking your new account up to your core business systems.

The single most impactful thing you can do right now is link your new bank account to your accounting software. Whether you use Xero, QuickBooks, or another platform, setting up a direct bank feed is non-negotiable. This link automatically pulls in all your transactions, which makes bookkeeping and reconciliation so much simpler.

Instead of messing about with manually uploading statements, your transactions will pop up in your software every day. This gives you a real-time picture of your cash flow and makes getting ready for your tax return significantly less painful.

A well-managed business account is more than just a place for money to sit. Think of it as the foundation of your business's financial health and a key part of building a solid relationship with your bank.

With the digital side sorted, let's turn to the physical tools. Get your business debit cards ordered for yourself and any key team members who need to make company purchases. It’s also worth taking a moment to request a chequebook if you deal with any suppliers who are still a bit old-school.

Finally, sit down and read through your bank's fee schedule one more time. Now that the account is live, you need to be crystal clear on:

Knowing these costs inside-out helps you avoid nasty surprises and manage your banking expenses properly. A strong handle on your finances also puts you in a much better position for future growth. A well-structured business bank account is crucial for getting access to finance, which is vital for expansion. The British Business Bank, for example, supported funding for 24,000 businesses, leading to massive economic contributions. You can explore the impact of accessible finance for UK businesses on their site.

It's completely normal to have a few last-minute questions before you commit to opening a business bank account. Let's walk through some of the most common ones we hear from business owners to help clear things up.

One of the biggest queries always comes from sole traders: do I really need a separate account? While there’s no law forcing you to, mixing your personal and business finances is a recipe for an accounting nightmare down the line. It makes tracking your expenses and figuring out your tax bill a real headache. For a deeper dive, our guide on accounting for sole traders is packed with useful advice. Trust me, keeping things separate is the smart play for clarity, professionalism, and your own sanity.

Another major concern is how long it all takes. Realistically, how quickly can you get an account up and running in the UK? For a simple application with a modern digital bank, you could be approved in as little as 24-48 hours. It can be surprisingly fast. However, if you're going with a high-street bank or your business has a more complex ownership structure, it's safer to budget for one to two weeks.

First off, don't panic if your application gets turned down. The first thing you should do is ask the bank why. Often, it's something simple—a flag on a credit check or a small detail missing from your paperwork.

A rejection from one bank doesn't spell disaster. Every bank has its own risk appetite and lending criteria. The newer digital banks, in particular, can be a lot more flexible than their traditional counterparts.

Go back through your documents with a fine-tooth comb, fix any potential problems, and then try applying with a different provider.

Ready to get your business finances organised and ensure you're compliant from day one? The team of experts at GenTax Accountants is here to help. We offer straightforward, tech-focused accounting services built for the way modern UK businesses operate. Get in touch today for a free consultation.