Think of the UK dividend allowance as your personal tax-free limit for investment returns. It’s a set amount of dividend income you can receive each year before you have to pay any tax on it. It’s a simple concept on the surface, but understanding how it works is absolutely crucial for managing your investments tax-efficiently.

The most important thing to get your head around is that the dividend allowance isn’t a deduction that reduces your total income like the Personal Allowance does. Instead, it’s a 0% tax band. This means the first slice of your dividend income is simply taxed at zero, no matter what your other earnings look like. It’s the same for everyone, whether you’re a basic, higher, or additional rate taxpayer.

To picture how this works, imagine your total income is a big measuring jug. Your salary, savings interest, and any other earnings get poured in first, filling it from the bottom. Your dividend income is then poured in on top of all that. The dividend allowance is like a special, tax-free layer right at the top of that income stack.

There are a couple of key details that often trip people up:

This distinction is vital because it means your dividend allowance can push your other income—like your salary or savings interest—into a higher tax bracket. It’s a common point of confusion that can lead to unexpected tax bills if you’re not careful.

The dividend allowance has been slashed in recent years, which makes tax-savvy planning more important than ever. For the current 2025/26 tax year, the allowance is just £500. This is a huge drop from the £5,000 it was when first introduced back in 2016/17.

As publications like Freetrade.io have pointed out, this reduction has a real impact on investors. Any dividend income you earn above this £500 threshold will be taxed. The rate you pay depends entirely on which income tax band that extra dividend income falls into. With such a tight limit, it makes using tax wrappers like ISAs and pensions to shelter your investments from tax even more of a no-brainer.

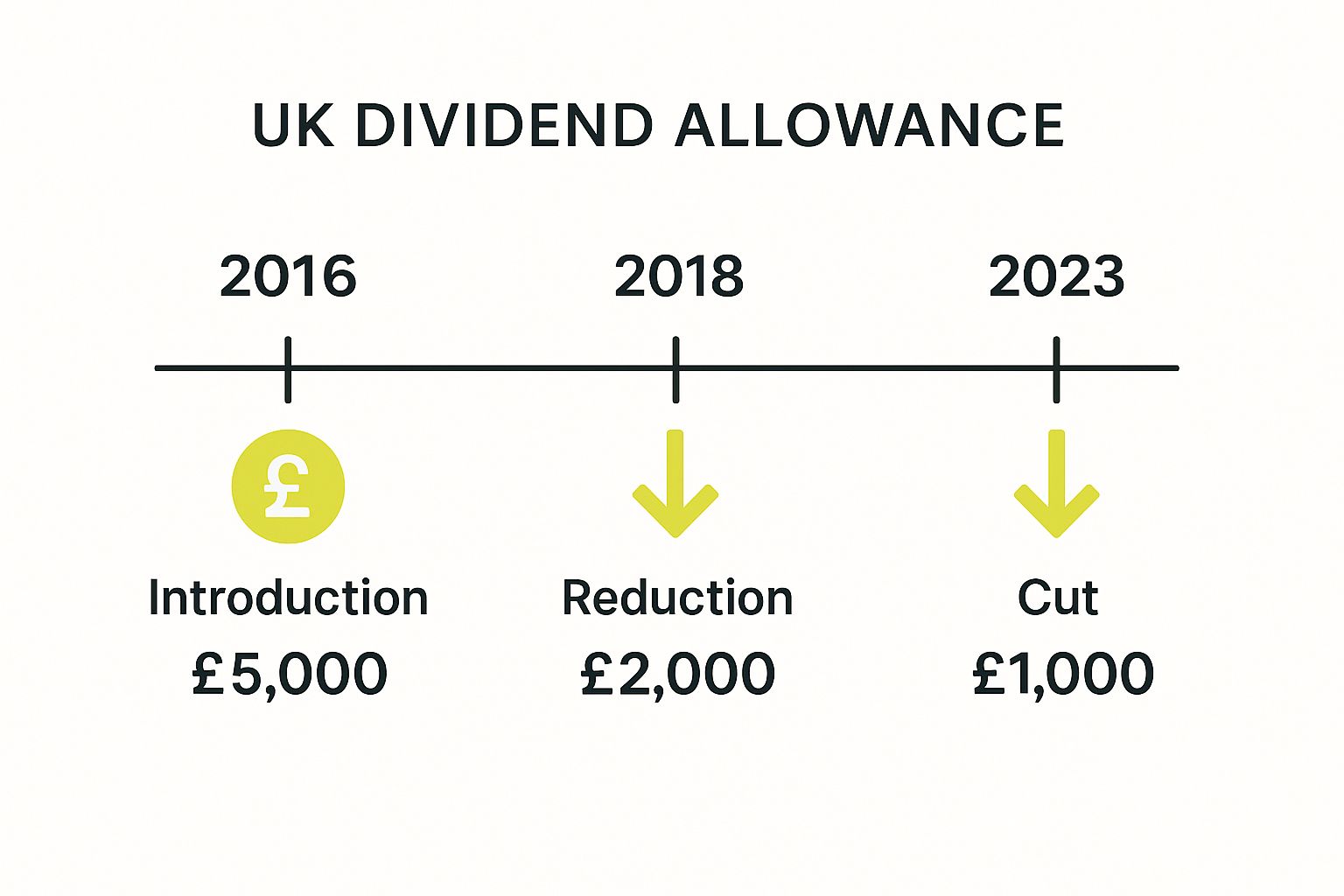

To get a proper grip on today's UK dividend allowance, it’s helpful to take a quick look back at its recent, and rather dramatic, history. This allowance hasn’t always been around, and its value has been on a rollercoaster, reflecting a real shift in government thinking on investment income. Understanding these changes gives you the context for why your own tax bill might look quite different from just a few years ago.

When it first landed in the 2016/17 tax year, the allowance was a pretty generous £5,000. This was great news for most investors, especially those with smaller portfolios, as it meant a decent chunk of dividend income could be earned completely tax-free. But, as we've seen, that didn't last.

The first big shock came in the 2018/19 tax year. The allowance was slashed by a massive 60%, plummeting to just £2,000. It then sat at that level for five years, giving investors a period of relative calm and predictability.

That stability came to an abrupt end recently. For the 2023/24 tax year, the allowance was halved again to £1,000. Then, from the 2024/25 tax year, it was chopped in half once more, landing at its current level of just £500. All told, that’s a 90% nosedive in the tax-free dividend threshold in just a handful of years. Unsurprisingly, this has dragged a lot more people into paying tax on their dividends.

This timeline gives you a stark visual of just how sharply the UK dividend allowance has been cut since it was introduced.

As the infographic makes painfully clear, the drop has been swift and steep. It really underlines the government's move to pull in more tax revenue from investment income.

Knowing this history isn't just a bit of tax trivia; it points to a clear policy direction and has very real consequences for investors and company directors right now.

The bottom line is that an income stream that might have been tax-free a few years ago is now very likely to create a tax bill. This is especially true if you're a limited company director paying yourself with dividends. If you haven't adjusted your payment strategy, you could be facing higher personal tax bills.

For anyone running their own business, this makes getting your finances structured properly from day one more critical than ever. How you set up your company can directly affect your personal tax situation, something we explore in our guide on understanding company registration fees in the UK. This history lesson confirms it: proactive, informed tax planning isn't a luxury anymore—it's a necessity for UK investors.

Figuring out what you might owe HMRC on your dividends can feel a bit like a puzzle at first, but once you get the hang of it, there’s a clear logic. The most important concept to grasp is what accountants call the 'stacking' principle.

Essentially, your dividend income is always treated as the last slice of your total income. It gets stacked right on top of everything else you earn—your salary, any self-employment profits, rental income, you name it.

So, the first step is always to work out your total income from all your non-dividend sources. This number is crucial because it tells you which tax bands your dividend income will spill into. Once you know that, you can apply the right dividend tax rates.

Imagine your income tax bands are like a set of buckets you need to fill up in a specific order. Your regular earnings (salary, pension, etc.) go in first, starting with your tax-free Personal Allowance.

Here's the critical takeaway: even though your dividend allowance is tax-free, it still uses up a portion of your income tax band. This is a detail that many people miss, and it can sometimes be enough to push some of your other income into a higher tax bracket. You have to look at the complete picture.

The rate you actually pay on dividends above your £500 allowance is tied directly to your overall income tax band. This table breaks down how the dividend tax rates line up with the standard UK income tax bands for the current tax year.

As you can see, while dividend tax rates are lower than standard income tax rates, they climb significantly as your total income increases. You can find more historical details on the official government guidance page.

Let's walk through a scenario. Meet Sarah, an investor with a £45,000 salary who also received £3,000 in dividends from her investment portfolio this year.

This step-by-step process shows how all the different allowances and tax bands fit together. Getting this right is absolutely fundamental to good financial planning. If you’re ever unsure, getting an expert to handle your personal tax returns can give you complete peace of mind and ensure you’re not overpaying.

Knowing the rules is one thing, but actually using that knowledge to protect your investment returns is where you can make a real difference to your pocket. With the UK dividend allowance now slashed to just £500, simply letting your investments sit there exposed to tax can be a costly mistake.

The good news is, there are several powerful and perfectly legal strategies you can use to shelter your dividend income from HMRC's reach. Most of the best methods involve using special tax-efficient accounts, often called 'tax wrappers', that create a protective shield around your hard-earned money.

For most UK investors, the Stocks and Shares Individual Savings Account (ISA) is the most powerful tool in the box. It’s best to think of it as a tax-proof container for your investments. Any dividends or capital gains made from assets held inside an ISA are completely tax-free, for life.

Each tax year, you can pop up to £20,000 into your ISA. And here’s the crucial part: dividends you receive inside an ISA do not count towards your £500 dividend allowance. This means you could get thousands in dividends from your ISA portfolio and still have your full £500 allowance available for any investments you hold outside of it.

For any investor serious about building long-term wealth, maxing out your ISA allowance each year should be a top priority. It's a simple, use-it-or-lose-it opportunity to build a completely tax-free pot of investment income.

Just like ISAs, pensions are another incredibly effective tax wrapper. With a Self-Invested Personal Pension (SIPP), you can pick your own investments, and any dividends they generate inside the SIPP are shielded from tax. This allows your investments to grow without being dragged down by dividend tax, which massively boosts their compounding potential over the long run.

On top of that, when you pay into a pension, you get tax relief on your contributions at your marginal rate of income tax. This is basically the government topping up your pension pot, giving your investment an immediate boost. Of course, you can’t get your hands on the money until you’re 55 (rising to 57), but it’s an unbeatable strategy for long-term financial planning.

This strategy is remarkably simple but so often overlooked. Spouses and civil partners can transfer assets, including shares, between each other without triggering any Capital Gains Tax. This is a huge advantage when it comes to planning your household's tax position.

By shifting dividend-paying shares to a partner who is in a lower tax bracket or hasn't used up their allowances, you can effectively double your tax-free capacity as a couple.

Making sure these strategies are implemented correctly is key to making the most of your financial position. For business owners, it’s vital to ensure these personal tax strategies also line up with your company's finances. That's why many seek professional help with their company accounts to build a complete and cohesive plan.

Dealing with HMRC can sometimes feel like navigating a maze, but thankfully, telling them about your dividend income is usually pretty simple. The main thing you need to figure out is whether the amount you’ve received is enough to push you into filing a formal Self Assessment tax return.

The magic number here is £10,000. If your dividend income for the tax year crosses this line, you’re legally required to register for Self Assessment and file a return. You’ll need to declare all of your dividend income on it, along with any other money you've earned. HMRC then does its sums and works out your total tax bill, which will include what you owe on your dividends.

Now, even if your dividends are well under that £10,000 mark, you might still find yourself needing to do a tax return. This often happens if you're self-employed or have other untaxed income, like from a rental property.

If you're already in the Self Assessment system for another reason, you have to include all your dividend income on your return, no matter how small the amount. It's all about giving HMRC a complete and accurate picture of your finances for the year. And with things moving more and more online, which we explore in our guide on Making Tax Digital for Self Assessment, getting those figures right is more important than ever.

To get your tax return right, you'll need the dividend vouchers or statements from the companies you hold shares in. These little documents are crucial – they confirm how much you were paid and when. Make sure you keep them organised, as they’re your official proof of income.

So what happens if you’re in that middle ground? Your dividends are over the £500 UK dividend allowance but less than the £10,000 reporting threshold, and you don’t normally do a tax return. Good news – you've got a much easier option.

You don't need to go through the hassle of registering for Self Assessment. All you have to do is get in touch with HMRC and ask them to adjust your tax code.

It works like this:

This is a really handy way to sort out your tax bill on smaller amounts of dividend income without the admin of a full-blown tax return.

When it comes to taxes, a simple misunderstanding can end up being surprisingly costly. The UK dividend allowance is a classic example, surrounded by a few stubborn myths that trip up even seasoned investors. Let's clear the air and get these sorted.

The single biggest misconception is thinking the dividend allowance works like your Personal Allowance, where it's deducted from your total income to lower your tax bill. It doesn't. In reality, it’s a 0% tax band.

This might sound like splitting hairs, but it's a critical distinction. The first £500 of your dividends are indeed tax-free, but that income still uses up a slice of your income tax band. This can have a knock-on effect on how much tax you pay on your other earnings.

Another common point of confusion is how the dividend allowance interacts with other tax-free allowances. It’s easy to get them jumbled up, but they each have very different jobs.

Dividend Allowance vs Personal Savings Allowance: The dividend allowance is purely for income from company shares. The Personal Savings Allowance (PSA), on the other hand, is for interest you earn from places like bank accounts, building societies, or corporate bonds. They are two entirely separate pots.

The ISA Myth: This one is huge. A lot of people believe that any dividends they earn from investments held inside a Stocks and Shares ISA will eat into their dividend allowance. They absolutely do not.

Think of an ISA as a tax-proof wrapper for your investments. Any dividends generated inside that wrapper are completely shielded from tax and have zero impact on your £500 dividend allowance. This is what makes ISAs such a powerful tool for growing your investments tax-efficiently.

Getting these details right is the bedrock of smart financial planning. If you're running a business or your financial affairs are a bit more complex, trying to navigate these rules can feel like a minefield. The expert team at GenTax Accountants is here to provide clarity and help you make the right decisions for your money. You can learn more about our approach to helping clients succeed anytime.

By properly understanding what the dividend allowance is—and, just as importantly, what it isn't—you can steer clear of common mistakes and make sure your investments are structured in the most tax-efficient way possible.

To wrap things up, let’s go over some of the questions that crop up time and time again when talking about the UK dividend allowance. Think of this as a quick-fire round to clear up any lingering confusion.

If your total dividend income for the tax year comes in under the £500 allowance, you can breathe a sigh of relief. The good news is you won't owe a penny of tax on it.

Better still, you don't even need to tell HMRC about it, unless you're already filling out a Self Assessment tax return for other income. It’s simply your money to keep, completely tax-free.

Yes, they absolutely do. The UK dividend allowance is a single pot for all your dividend income, and that includes any payments from shares in foreign companies. You’ll need to add them to your UK dividends to get your total figure.

Just be mindful that dividends from overseas might have already had some tax taken off in their country of origin. To avoid being taxed twice on the same income, you can usually claim this back as a foreign tax credit on your Self Assessment return.

It's a classic mistake to overlook dividends from overseas investments. Always tally up every bit of dividend income, no matter where the company is based, before you work out what, if any, tax you owe.

Your dividend income doesn't directly eat into your main Personal Allowance of £12,570. However, your total income, including those dividends, can have a knock-on effect.

The issue arises if your 'adjusted net income'—which is basically all your taxable income added together—tips over the £100,000 mark. Once that happens, your Personal Allowance starts to shrink. It’s reduced by £1 for every £2 of income you earn above this threshold, eventually disappearing entirely once your income hits £125,140.

Getting your head around the interplay between dividend tax and personal allowances can be tricky, and that's where expert guidance really pays off. GenTax Accountants can help you structure your finances to be as tax-efficient as possible while keeping you fully compliant. Discover how our fixed-price, online accounting services can support your financial goals at https://www.gentax.uk.