The UK tax year always runs from 6th April to 5th April. This might seem like a random set of dates, but it’s the bedrock of the entire personal tax system, dictating when you need to report your earnings and pay what you owe to HMRC.

For anyone new to running a business, those dates—6th April to 5th April—often feel a bit strange. Why not just follow the calendar year?

It’s not a modern quirk; it’s a hangover from history. Think of it as your official financial ‘school year’. It's a fixed 12-month period where all your personal income, including earnings from your sole trader business, gets tallied up for tax purposes.

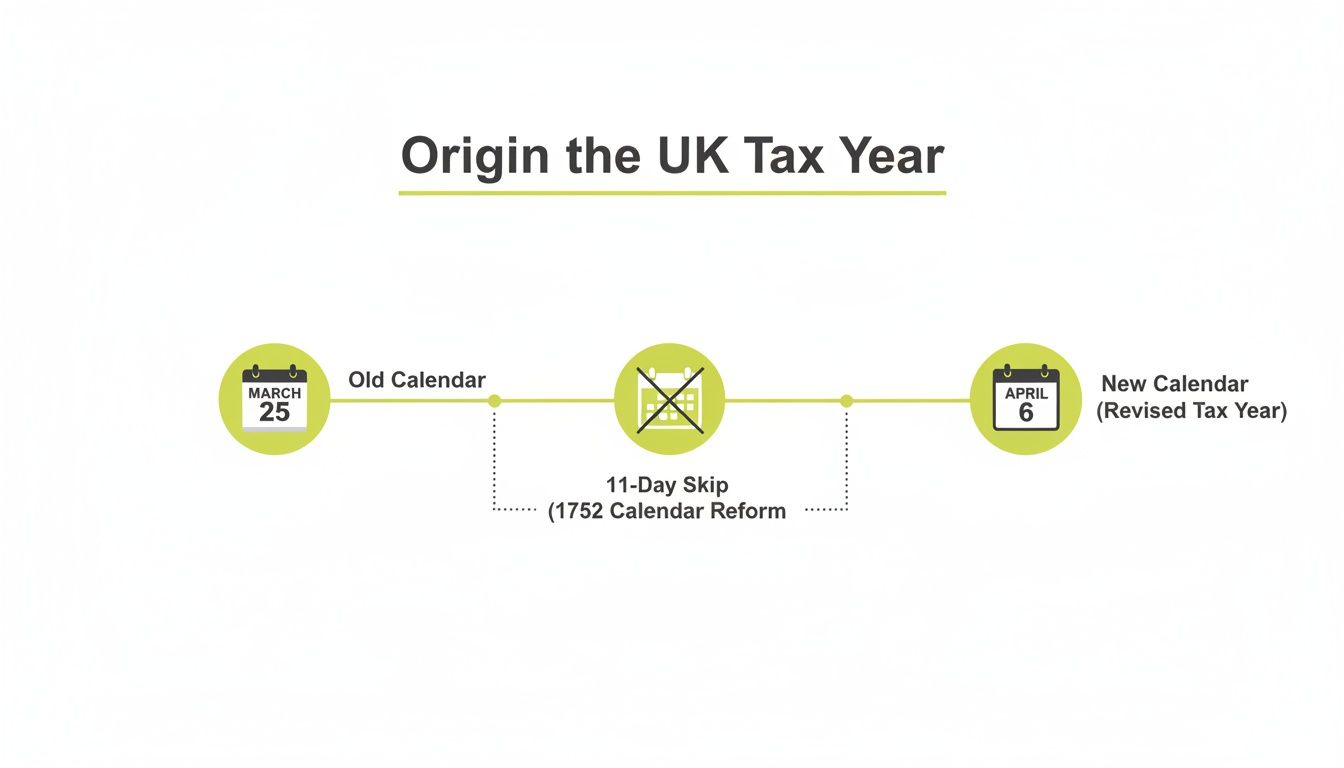

Believe it or not, this timeline is a direct result of a major calendar reform way back in 1752. The UK switched from the Julian to the Gregorian calendar, which meant skipping 11 days to catch up. The financial year originally ended on 25th March (Quarter Day), but to ensure a full year's revenue was collected, the date was pushed forward, eventually settling on the 6th of April. So, a centuries-old decision still shapes our modern tax deadlines.

Getting your head around this is the first real step to mastering your tax obligations. It’s the foundation that every other personal tax deadline is built on.

Whether you're a freelancer, a contractor, or the director of your own limited company, the 6th April to 5th April period is your personal tax anchor. Any income you receive personally within these dates—from self-employment, dividends, or even renting out a property—falls squarely into that specific tax year.

The trick is to mentally separate your personal tax duties from your limited company's financial calendar. Your company has its own financial year for Corporation Tax, but your personal Self-Assessment tax return always follows the standard 6th April to 5th April schedule.

This is a massive point of confusion for new directors, but it’s vital to get it right. Keeping these two calendars separate is key to good planning and is a cornerstone of solid tax advice for small businesses.

To make things clearer, here’s a quick summary of how the tax year works for different types of businesses.

This table breaks down the key concepts and shows who is most affected by the different financial calendars in the UK.

As you can see, while your limited company runs on its own schedule, your personal tax obligations are always tied to that classic 6th April to 5th April timeframe.

For anyone who’s a sole trader, freelancer, or even a company director sorting out their personal tax, the Self Assessment calendar is your roadmap. It can feel like a list of scary dates, but once you get the hang of it, you’ll see it’s just a predictable cycle. Think of it as your annual financial rhythm.

That rhythm kicks off right after the tax year wraps up on 5th April. But your first big milestone isn’t about paying tax – it’s about getting registered. If you’ve just gone self-employed or started renting out a property, this is your first crucial step.

The very first date to circle in your diary is 5th October. This is your deadline to tell HMRC you need to file a Self Assessment tax return for the tax year that just finished.

So, for example, if you set up as a sole trader in June 2024 (that’s in the 2024/25 tax year), you’ve got until 5th October 2025 to register. Miss this, and you’re starting on the back foot with potential penalties. It’s basically your way of officially saying to HMRC, "Hi, I'm here, and I'll be sending you a tax return."

Ever wondered why our tax year is so peculiar? This diagram explains the quirky bit of history that landed us with a 6th April start date.

Back in 1752, the calendar was adjusted by skipping 11 days. This nudged the old financial new year from 25th March all the way to 6th April, and we’ve been stuck with it ever since!

Once you’re registered, your attention needs to turn to the two most important dates in the Self Assessment year. These aren’t flexible, and missing them comes with hefty, automatic penalties.

The 31st January deadline is non-negotiable. If you miss it, you're looking at a late penalty that starts at 7.5% and only gets worse after 30 days. And don’t forget that 5th October registration deadline for anyone new to the system; it’s key to making sure you can hit your other deadlines without a panic.

Here's the catch: you can't possibly know your final tax bill until your return is finished. That’s why leaving it all until the last week of January is a recipe for stress, rushed calculations, and mistakes.

But the story doesn't end on 31st January. If your tax bill comes to more than £1,000 and less than 80% of it was already paid through a salary (PAYE), HMRC will ask you to make advance payments towards your next tax bill. These are called Payments on Account.

It’s a simple system: each payment is 50% of your previous year's tax bill. The deadlines are:

Let's say your tax bill for the 2023/24 tax year was £3,000. By 31st January 2025, you'd need to pay that £3,000. But you’d also have to pay £1,500 towards your next bill (2024/25), followed by another £1,500 on 31st July 2025. It’s HMRC’s way of spreading the load, so you don't face one massive lump sum each year.

Keeping on top of this is so much easier when your books are in good order, which is the whole idea behind Making Tax Digital for Self Assessment.

When you're a limited company director, you have to get used to a completely different rhythm for your taxes. While your own tax affairs stick to the usual UK tax year, your company marches to the beat of its own drum. This separation is probably one of the most important concepts for any director to get their head around.

Think of your company’s financial year as its own 'birthday'. It’s a 12-month period that you choose when you first incorporate, and that date is called your accounting reference date. It becomes the anchor for all your key corporate deadlines, dictating when your accounts are due, when you file your tax return, and when you pay your Corporation Tax.

When you first set up your business, Companies House automatically gives you a year-end. It's set to the last day of the month, one year after your company was formed. So, if you registered your company on 10th May 2024, your first official year-end would be 31st May 2025.

The good news is you're not stuck with this date. You can change it if another time of year works better for your business cycle. Many directors line it up with the personal tax year (31st March) or the calendar year (31st December) just to keep things simple, but the choice is entirely yours.

Once that year-end date is set, it triggers a chain of crucial deadlines you absolutely cannot afford to miss. Getting these right is fundamental to running a compliant company and avoiding painful penalties from both Companies House and HMRC.

First up is your duty to Companies House. You need to file your company's annual accounts, which provide a public snapshot of your company's financial performance and health over the previous year.

The deadline here is strict: nine months after your company’s financial year-end. If your year-end is 31st March, your accounts must be filed by 31st December. Fail to meet this, and you're hit with automatic penalties that start at £150 for being just one day late and only get worse from there.

Remember, Companies House and HMRC are two completely separate government bodies. Filing your accounts with one does not mean you've filed your tax return with the other. They are distinct obligations with their own deadlines.

Next, you have your responsibilities to HMRC, which cover your Company Tax Return and paying the actual Corporation Tax bill. The return, officially known as a CT600, is where you detail your company's income, expenses, and calculate the profit or loss that your tax is based on. If you're looking for a deeper dive, our guide explains what is Corporation Tax in much more detail.

Now, this is where things get a little tricky, because there are two different deadlines to juggle.

Yes, you read that correctly. Your tax payment is due before the filing deadline for the return that calculates it. This little quirk means you can't leave things until the last minute. You need solid, proactive bookkeeping throughout the year to estimate your liability and pay it on time, otherwise you'll be stung with interest charges from HMRC.

Just as crucial as tax deadlines, effectively managing all financial timelines is vital for business health, which includes optimising your accounts payable workflow.

Finally, it’s vital to connect your company's finances back to your personal tax situation. Any director's salary you take or shareholder dividends you receive must be declared on your personal Self-Assessment tax return. This income is taxed according to the standard 6th April to 5th April tax year, no matter when your company's financial year ends.

This is a classic tripwire for new directors. You have to keep one eye on your company's year-end for all your corporate filings, and the other on the UK personal tax year for your Self-Assessment. Getting this balance right keeps you fully compliant and allows you to plan your finances effectively—both for your business and for yourself.

For any business that’s VAT-registered or has employees, tax compliance isn't just a once-a-year headache. It’s a constant operational pulse, a steady beat of deadlines that keeps your company healthy and on the right side of HMRC. If you start thinking of these dates as the vital signs of your business, they stop being chores and become manageable, predictable parts of your routine.

Unlike the annual dash for Self Assessment, both VAT and PAYE (Pay As You Earn) work on much shorter cycles. Getting the hang of this regular beat is absolutely essential for smooth cash flow and avoiding the sting of late penalties. Let’s break down the tempo for each.

Once your business turnover hits the VAT registration threshold, you’re put onto a standard quarterly cycle. This simply means that every three months, you need to tally up the VAT you've charged on sales and subtract the VAT you've paid on your own business purchases.

HMRC will usually assign your VAT periods when you register, and they often line up with calendar quarters. The critical deadline to burn into your memory for both filing your return and paying the bill is one month and seven days after your accounting period ends.

Here’s a classic example to make it clear:

This deadline is fixed, regardless of whether you owe HMRC, are due a refund, or just have a 'nil' return to file. Missing it can land you in a points-based penalty system, so consistency is your best friend here.

If you have staff on the payroll – even if it’s just yourself as the director of your limited company – you’ve got PAYE responsibilities. This is HMRC’s system for collecting Income Tax and National Insurance contributions straight from earnings. The rhythm here is much faster; it’s a monthly commitment.

Every time you run your payroll, you have to report your employees' payment details and deductions to HMRC. This is done through a Full Payment Submission (FPS).

The golden rule for PAYE is simple: your FPS must be sent to HMRC on or before your employees' payday. This gives HMRC a real-time picture of who is being paid what, and how much tax is being collected.

After you've sent the FPS, the clock starts ticking on your payment deadline. Any tax and National Insurance you owe for a tax month (which, don't forget, runs from the 6th of one month to the 5th of the next) must land in HMRC's account by the 22nd of the following month. If you’re paying by post, that date is the 19th.

For instance, for the tax month ending 5th May, your payment to HMRC is due by 22nd May. This is a non-negotiable monthly cycle for every employer. Getting this process right is vital, and exploring your options for payroll services for small businesses in the UK can be a game-changer.

Putting simple systems in place to track these recurring dates is a must. Set reminders in your calendar, use accounting software with built-in alerts, or let an accountant handle the deadlines for you. By treating VAT and PAYE as the steady heartbeat of your company's finances, you'll never miss a beat and keep your business strong and compliant.

Knowing the calendar is one thing, but dealing with the real-world pressure of running a business means even the most organised person can slip up. Getting wise to the common pitfalls around UK tax dates is your best defence against needless stress and penalties from HMRC.

Think of these as early warning signals. They're not just simple admin errors; they carry real financial consequences and can trip up even experienced business owners.

This is one of the most common and easily dodged mistakes out there. The deadline to register is 5th October.

Picture this: you start a freelance side-hustle in May. You’re totally focused on finding clients and doing great work. Tax is the last thing on your mind. Before you know it, October has flown by, and you’ve completely missed the deadline to tell HMRC you need to file a tax return. This leads to a last-minute panic and can land you with penalties before you’ve even filed your first set of figures.

The next big tripwire is the shock of ‘Payments on Account’. So many sole traders breathe a huge sigh of relief after paying their tax bill on 31st January, only to get a nasty surprise: they also owe an advance payment towards the next tax year on the very same day.

Here’s a typical scenario:

This effectively makes their January payment a whopping 150% of their annual bill. Forgetting to budget for this is a massive cash flow shock that catches thousands of business owners off guard every single year.

For limited company directors, the biggest mistake is blurring the lines between the company's financial year and the personal tax year. Your company might have a year-end of 31st December, but any dividends you take are assessed based on the personal tax year dates: 6th April to 5th April.

This distinction is absolutely critical. Getting these two calendars mixed up can lead to incorrect Self Assessment filings, missed dividend tax, and a compliance headache that’s a real nightmare to unravel.

The UK tax year's rhythm provides a steady framework, even as specific tax rates and rules change over time. This consistency is vital for government revenue, with taxes recently averaging 33% of GDP. Income tax remains the biggest earner, but VAT has grown significantly, now accounting for about 15% of revenue after several rate hikes. Missing a VAT deadline, for instance, can have a major financial impact.

Of course, the foundation for avoiding all these errors is solid record-keeping. If your paperwork is a mess, meeting deadlines becomes a huge challenge. A great place to start is learning how to organize receipts for taxes. Keeping your financial documents in good order is the first, most important step to staying on top of every deadline.

Juggling the various tax deadlines can throw up a lot of questions, especially when you’re trying to keep track of different responsibilities. We’ve answered some of the most common queries business owners ask about UK tax dates to give you some quick, clear guidance.

This one trips a lot of people up, and the answer really depends on what part of your tax life you’re talking about.

When it comes to your personal tax return—your Self-Assessment—the answer is a simple no. The 6th April to 5th April tax year is set in stone by UK law for every individual. You can't shift it.

However, a limited company plays by different rules. You get to choose your company's 'financial year', which is its 12-month accounting period. This can start in any month you like, and that date is what drives your deadlines for Corporation Tax and filing your annual accounts with Companies House.

Honestly, not much good. Missing an HMRC deadline almost always triggers automatic penalties and interest charges that start racking up from day one.

For Self-Assessment, you’ll be hit with a £100 late filing penalty the day after the deadline passes. This applies even if you have no tax to pay or have already paid it. After that, further penalties are added at three, six, and twelve months, and interest is charged on any tax that’s late.

It's a similar story for late VAT, PAYE, and Corporation Tax. The penalties are designed to sting. The absolute best thing you can do is act fast. If you realise you've missed a deadline, get in touch with HMRC or your accountant immediately to figure out the damage and stop it from getting worse.

If you’re the director of a VAT-registered company that also employs staff, you're not just managing one tax calendar—you're juggling several at once. For example, you’ll have quarterly VAT deadlines, and it's crucial to get those right. Our guide on what is the VAT registration threshold can shed more light on that side of things.

You’re basically tracking two completely separate timelines: one for your personal tax and another for the company. Any salary or dividends you draw from the business go on your Self-Assessment return, which sticks to the standard tax year. At the same time, your company has its own set of deadlines based on its financial year.

The only sane way to stay on top of it all is to use accounting software, set up calendar alerts for everything, and—most effectively—work with an accountant. It’s the surest way to stay organised and keep everything compliant.

At GenTax Accountants, we help businesses of all sizes master their financial calendars, ensuring you never miss a critical deadline. Let us handle the dates so you can focus on your business.