When your business starts to grow, there are a few key milestones you’ll hit. One of the most significant from a tax perspective is crossing the VAT registration threshold. In simple terms, this is the turnover figure set by the government that dictates when you absolutely must register for, and start charging, Value Added Tax (VAT).

In the UK, if your business's taxable sales push past £90,000 in any rolling 12-month period, you’re legally required to sign up with HMRC. Think of it as a financial tripwire; once you hit it, your tax responsibilities change.

Picture a line in the sand. On one side, your business operates without the complexity of VAT. But the moment your turnover crosses that line, you’ve entered a new territory with different rules for pricing and paperwork. The VAT registration threshold is exactly that line for your business finances.

It’s crucial to realise this isn’t a figure you only check at your financial year-end. The £90,000 limit is based on a rolling 12-month period. This means at the end of every single month, you need to look back over the last 12 months of sales to see if you’ve crossed it. It’s a continuous monitoring process.

So, what exactly contributes to this £90,000 figure? We're talking about your taxable turnover, which is the total value of all goods and services you sell that aren't specifically exempt from VAT. This is a vital distinction to make.

It covers:

To give you some context, the current £90,000 threshold was increased from £85,000, where it had been since 2017. Before that, it was £79,000 back in 2013, showing how it adjusts over time with the economy.

The main takeaway here is that once your turnover goes over this limit, registering for VAT isn't a choice—it's the law. Getting this wrong can lead to some hefty penalties from HMRC, so it pays to stay on top of your numbers and understand what's involved with preparing and filing your VAT returns correctly.

When you look at the UK's VAT registration threshold, it's easy to think of it as just another number from HMRC. But once you zoom out and see it on a global stage, you realise just how unusual our approach is. This isn't an accident; it's a very deliberate government strategy that has a huge impact on small businesses and startups across the country.

Put simply, the UK's £90,000 VAT threshold is exceptionally high. In fact, it's the joint highest among all Organisation for Economic Co-operation and Development (OECD) countries. Many of our European neighbours have much lower limits, often somewhere between €10,000 and €35,000 (that’s roughly £8,500 to £30,000). For a deeper dive into these international differences, the ICAEW has a brilliant analysis.

This high threshold essentially acts as a protective bubble, shielding a massive number of small businesses from the headache and expense of VAT compliance. For many entrepreneurs just starting out, that means more time to focus on growing the business, not filling out tax forms.

So, why does the UK stick with such a high figure? It all comes down to creating a supportive environment where small businesses can get off the ground and thrive. By setting the VAT bar high, the government is aiming to:

This policy gives UK-based small businesses a clear head start compared to their international counterparts. It provides a much longer runway for growth before the business has to deal with the major operational shift that VAT registration brings. Of course, this approach also sparks a lot of economic debate, weighing up the benefits of small business support against the potential for a smaller national tax base.

Getting your head around how to calculate your turnover is the most important part of managing your VAT duties. It's also where things most often go wrong. A simple miscalculation can easily push you over the threshold without you realising, landing you with an unexpected tax bill and a penalty from HMRC. The key thing to remember is that this is all about your total sales, not your profit.

The biggest hurdle for most business owners is the rolling 12-month period. This isn't your financial year or the tax year. Instead, it’s a constant process. You need to check your total turnover at the end of every single month, looking back over the 12 months that just passed.

Think of it like a moving window that’s one year wide. At the end of May, you look at your sales from the previous June to May. At the end of June, you look at July to June. It’s a constant, active monitoring process.

To figure out where you stand against the VAT threshold, you must add up the total value of everything you sell that isn't VAT-exempt. This "taxable turnover" figure needs to include:

On the flip side, you should exclude any sales that are specifically exempt from VAT. Common examples include postage stamps, most property transactions, or financial and insurance services.

Let's walk through a real-world scenario. Imagine your business turnover from 1st April 2023 to 31st March 2024 was £84,000. You're comfortably under the limit.

But then, you have a fantastic month in April 2024, bringing in £12,000 in sales. At the end of April, you have to do the check. You'd take your previous 12-month total (£84,000), subtract the sales from April 2023 (let's say that was £5,000), and then add on your sales from April 2024 (£12,000).

Your new 12-month rolling total is now £91,000. You've crossed the threshold and need to register for VAT. This is why keeping your monthly records straight is so vital. Our guide to organising your business accounts can help you build a solid system to stay on top of this.

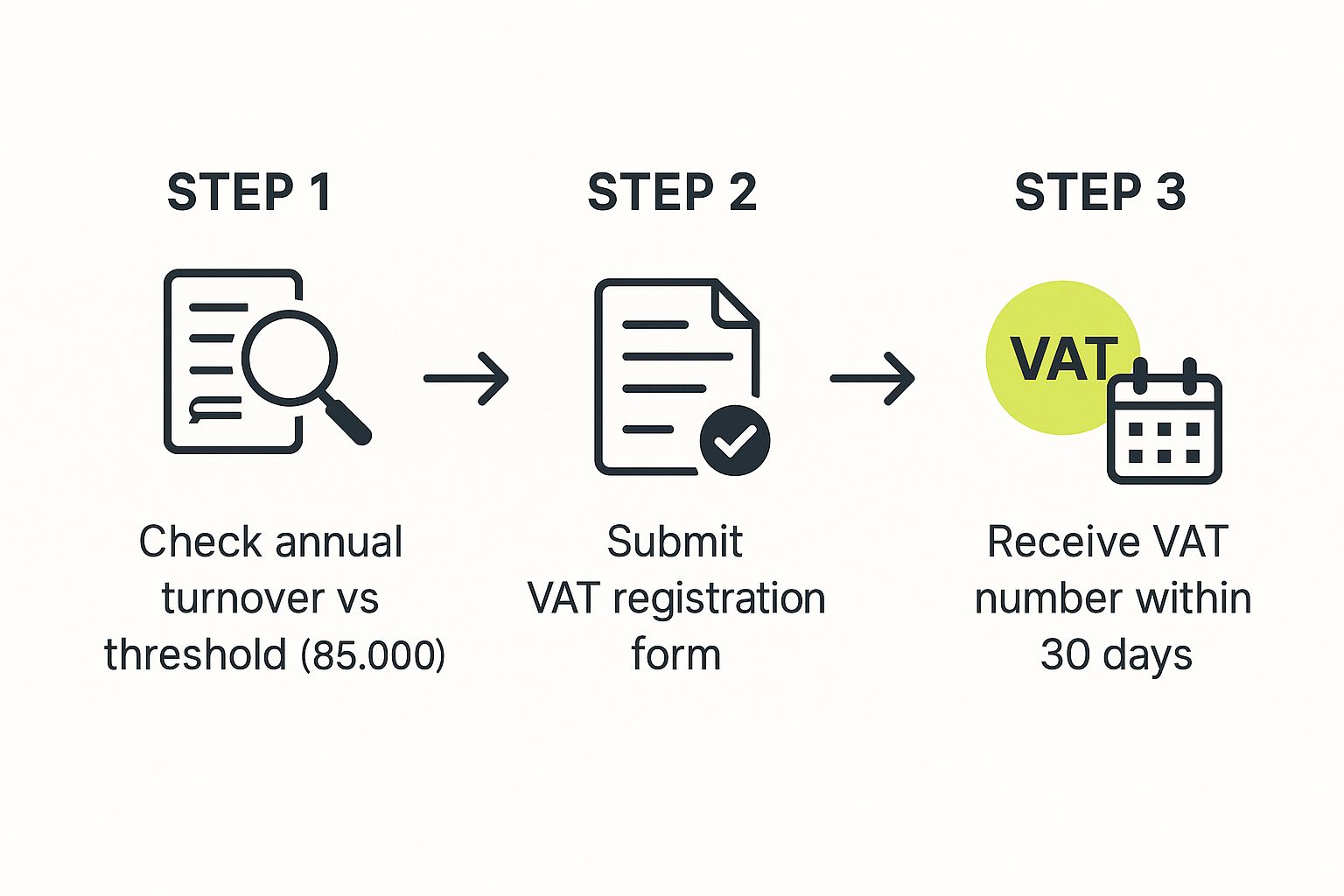

That moment you realise you’ve crossed the VAT registration threshold can feel a bit daunting, but the next steps are actually quite straightforward if you act quickly.

HMRC gives you a clear timeline: you have 30 days to register for VAT, and that clock starts ticking from the end of the month in which you went over the limit. So, if your rolling turnover tipped over £90,000 at any point in May, your 30-day registration window would kick off on 31st May.

This deadline isn't one to treat lightly. If you fail to register on time, you'll face penalties. Even more critically, you become liable for any VAT you should have charged from your effective date of registration. This is the date you were legally required to be registered, and HMRC will expect you to pay that VAT, even if you never actually collected it from your customers. It's a nasty surprise that can create a significant, unplanned financial hit.

The key takeaway here is that registration is a time-sensitive job. It requires you to keep a close eye on your turnover and act the moment you cross the line.

To make the whole process as painless as possible, it’s a good idea to get all your information together before you even start the application. A bit of prep work now can save you a lot of hassle and help you avoid missing that crucial deadline.

You’ll generally need to have these details to hand:

Your effective date of registration is a really important concept to grasp. It's typically the first day of the second month after you go over the threshold. For instance, if you cross the limit in May, your effective date is 1st July. From that day forward, you must start charging VAT on your sales.

For anyone just setting out on their business journey, getting to grips with these compliance steps is fundamental to building a solid venture. Our detailed guide on how to start a business in the UK covers the wider legal and financial duties you'll encounter. Acting decisively when you cross the VAT threshold is one of the first major tests of your business's financial management.

While you must register for VAT once your turnover hits the £90,000 limit, you don't actually have to wait. Choosing to register voluntarily, even when your sales are well below that magic number, is a strategic business move you might want to consider.

At first, this might sound a bit mad. Why would you sign yourself up for extra paperwork and tax filings if the law doesn't require it? The answer, for many businesses, comes down to one key benefit: reclaiming the VAT you spend on your own business expenses.

Think about it. If you're launching a new venture with hefty start-up costs—say, a design agency that needs powerful new computers, expensive software subscriptions, and office furniture—those costs add up. By registering for VAT, you can claim back the 20% you paid on all those eligible purchases, which can give your cash flow a serious boost right when you need it most.

Voluntary registration is a great tool, but it's not a one-size-fits-all solution. You really need to weigh up both sides of the coin, and the decision often boils down to who your customers are and what your costs look like.

Key Benefits of Voluntary Registration:

Potential Downsides to Consider:

Deciding whether to register voluntarily is a classic business dilemma. If your clients are mostly other VAT-registered businesses, they won't bat an eyelid at the extra VAT because they’ll just claim it back themselves. But if you sell directly to consumers, it could put you at a significant price disadvantage against your non-registered competitors.

Making smart choices like this means understanding the whole tax picture. For more on this, our guide on tax advice for small businesses is a great place to start, as it covers far more than just VAT. Ultimately, the best decision for you will depend entirely on your unique business model and where you plan to take it.

Getting your head around VAT doesn't have to mean drowning in paperwork, especially for smaller businesses. HMRC has actually created several simplified schemes to cut down the admin and make staying compliant a whole lot easier. Think of them as alternatives to the standard, sometimes clunky, way of doing VAT.

Each scheme is built with different types of businesses in mind, so you can find a better fit. For example, the Cash Accounting Scheme is a lifesaver for managing cash flow. It lets you account for VAT when money actually hits your bank account, not just when you send an invoice. Then there’s the Annual Accounting Scheme, which lets you file just one VAT return a year instead of four.

These schemes are designed to ease you into the world of VAT. HMRC recognises that a one-size-fits-all approach just doesn't work, so they provide this crucial middle ground between not being registered at all and tackling the full weight of standard VAT accounting.

To give smaller businesses even more support, there are options like the Flat Rate Scheme, which comes with its own specific turnover limits for joining and staying on it. Other schemes, like the Cash and Annual Accounting options, are open to businesses with much higher turnovers, creating a sort of tiered system for compliance. You can dig into the specifics of VAT thresholds for these schemes over at Ross Martin.

Picking the right scheme can make a massive difference to your admin time, but remember that eligibility is tied to your business type and turnover.

Just as there are rules for getting into the VAT system, there are also clear guidelines for getting out. If your taxable turnover has dropped and you’re confident it will stay below the £88,000 deregistration threshold for the next 12 months, you can apply to cancel your VAT registration.

This often happens if you decide to scale back your business or change your services. Once you deregister, you’ll stop charging VAT on your sales and you won't be able to reclaim it on your expenses. It's a great way to simplify your finances if your turnover is consistently below that mark.

Getting to grips with the VAT registration rules always throws up a few tricky “what if” scenarios. Nailing these edge cases is absolutely crucial if you want to stay on the right side of HMRC and dodge any expensive mistakes.

A classic point of confusion is the "forward look" test. What happens if you land a massive new contract and you know, without a doubt, your turnover is going to blow past the threshold in the next 30 days alone?

The rule here is crystal clear: you must register for VAT the moment you realise this is going to happen. You don’t get to wait until the money is actually in the bank. Your registration date is the day you became aware that your turnover was about to jump significantly.

Another frequent question is about international sales. Do sales to customers outside the UK count towards your turnover? It’s a bit complicated.

Generally, sales of goods (exports) are zero-rated for VAT, but you must still include them when you calculate your total turnover for the threshold. The rules for services can be different and often depend on the specific service and where your customer is based, which is where getting professional advice becomes really important.

What if your turnover shoots up, you register for VAT, and then it dips back down again? You can apply to deregister, but only if you can prove to HMRC that your turnover will stay below the £88,000 deregistration threshold for the next 12 months.

Be careful, though. If you think the dip is just a temporary blip, the admin headache of deregistering and then having to re-register a few months later often isn't worth the hassle.

The best way to navigate all of these situations is to keep meticulous records. If you need a hand staying on top of your financial data, professional bookkeeping services can bring clarity and make sure you're always prepared for whatever comes your way.