Deciding between a limited company and an LLP really boils down to how you want to structure your business and handle your tax. Think of a Limited Company (Ltd) as its own legal person, owned by shareholders and perfect for businesses that want to reinvest profits back into growth. On the other hand, a Limited Liability Partnership (LLP) is designed for partnerships where the members are taxed individually, making it a classic choice for professional service firms who distribute all profits.

When you're mapping out your new venture, the limited company vs LLP debate is one of the first big hurdles. Both structures give you that crucial layer of protection known as limited liability, meaning your personal assets are shielded if the business runs into trouble. But that’s where the similarities end.

The way they operate, how they’re taxed, and who’s in charge are worlds apart. Getting this right from day one can save a lot of headaches down the line. If you're still in the early stages, our guide on how to start a business in the UK is a great place to get your bearings.

The biggest difference is all about ownership. A limited company is owned by its shareholders and run by directors (who can absolutely be the same people). This clean separation of roles creates a formal, flexible structure that's ideal for businesses looking to bring in investors or build a clear management hierarchy.

An LLP, however, is a different beast entirely. It must have at least two ‘members’. These members are the partners who own and run the business together, sharing the profits and the responsibilities. It’s this collaborative, partner-led model that makes LLPs the go-to for professional practices like law firms, architects, and accountancy practices.

The core operational difference is simple: a limited company is run by its directors for its shareholders, while an LLP is run by its members, for its members. This distinction influences everything from decision-making to profit distribution.

Before we get into the nitty-gritty of tax and liability later in this guide, it helps to see the fundamental differences side-by-side. Think of this as the high-level cheat sheet to see which structure might align with your vision.

The table below breaks down the most important attributes at a glance.

This overview should give you a clear starting point. As you can see, while both offer protection, their internal wiring is completely different, suiting very different types of businesses and goals.

When you’re weighing up a limited company vs an LLP, one of the biggest draws for both is that they create a separate legal entity. This is a game-changer. It means your business is legally recognised as its own "person," entirely distinct from you, the owner.

This separation is what allows the business to sign contracts, buy property, and even take someone to court (or be taken to court) in its own name. For you, this creates a vital protective barrier—often called the "corporate veil"—that shields your personal finances if the business runs into trouble.

With a private limited company, liability is all about the shares. As a shareholder, your personal financial risk is usually limited to whatever amount is unpaid on your shares. For most small businesses, shares are fully paid up when the company is formed, often for a token amount like £1 per share.

So, what does this mean in practice? If the company racks up debts it can’t pay, creditors can go after the company’s assets, but they can't touch your house, your car, or your personal savings. It’s a solid, clearly defined layer of protection.

The corporate veil is a powerful legal shield. For a limited company director or shareholder, this means that unless fraud is involved, the financial fallout of a business failure stops with the company itself.

An LLP offers a similar safety net for its members, but it works a little differently. Here, your liability is generally limited to the amount of capital you've personally invested in the partnership. This is all laid out in the LLP agreement.

This setup is especially valuable in professional services—think law or accountancy firms—where one partner’s mistake could lead to a massive financial claim. If one member is found to be negligent, the personal assets of the other members are protected. It ring-fences the risk. It’s important to remember, though, that each member is still fully liable for their own professional negligence.

While limited liability is a huge advantage, it's not a magical forcefield. There are a few specific situations where the courts can "pierce the veil," making directors or members personally responsible for the business's debts.

It’s crucial to know where the lines are drawn.

Key Exceptions to Limited Liability:

Understanding these exceptions gives you a much more realistic picture of the protection you're getting. Setting up a corporate body is a fantastic way to manage risk, but it’s no substitute for sharp financial management and sound professional advice. For a deeper look at the duties involved, check out our accounting services for limited companies. Getting this right from the start is essential when deciding between a limited company vs an LLP.

When it comes to the Limited Company vs LLP debate, tax is often where the decision really clicks into place. The two structures are treated in fundamentally different ways by HMRC, and getting your head around this is vital for choosing the path that fits your financial goals.

One approach is built for reinvesting profits and scaling up, while the other offers a much simpler route for getting earnings directly into the hands of the partners.

For a limited company, tax is a two-step process. First, the company itself is treated as a separate legal entity and pays Corporation Tax on all its taxable profits. Only after HMRC has taken its slice can the remaining profits be passed on to the company’s owners (the shareholders).

This is an incredibly powerful setup for any business focused on growth. Because profits can be kept within the company having only paid Corporation Tax, it creates a tax-efficient pot of cash to fund expansion, buy new equipment, or just build up a rainy-day fund. You can get the full rundown in our guide on what is Corporation Tax.

An LLP, on the other hand, is what’s known as 'tax transparent'. This is a key bit of jargon that simply means the LLP itself doesn’t pay a penny in tax. Instead, the profits are seen to 'pass through' straight to the individual members, who then become personally responsible for settling the bill with HMRC.

Each member is effectively treated as self-employed. This means they need to register for Self Assessment and pay Income Tax and National Insurance Contributions (NICs) on their share of the LLP's profits—and this is crucial—whether they’ve actually taken the money out or not. It’s a very direct system, often favoured by professional services firms where the plan is simply to distribute all the profits each year.

The core tax difference is this: a limited company is taxed as a separate entity on its profits before owners are paid, whereas an LLP is not taxed at all—the tax burden falls entirely on the individual members.

The way you actually take money out of the business is where you’ll really feel the difference. This choice directly shapes your personal tax bill and how efficiently you can access your earnings.

For a Limited Company:

This blend of a small, tax-efficient salary topped up with dividends is a classic, tried-and-tested strategy for owner-directors looking to optimise their take-home pay.

For an LLP:

The crucial tax differences between UK limited companies and LLPs create significant incentives depending on your business size and profit levels. Limited companies pay corporation tax at rates from 19% to 25%, which supports tax-efficient profit retention for growing businesses. Conversely, LLPs avoid corporation tax entirely, with profits passing through to members who are taxed at personal income tax rates. This is often more appealing for high earners in professional services like law or accountancy. A key advantage for LLPs is that members are treated as self-employed, avoiding employer NICs on profit shares—a potential saving of up to 15.5% compared to salaries in a limited company.

When you choose a business structure, you’re not just thinking about tax – you’re also signing up for a certain level of admin. The initial setup and the year-on-year compliance for a limited company and an LLP are quite different, affecting everything from your workload to how much of your business is public knowledge.

Both journeys start at Companies House, but they don't start the same way. A limited company can be launched by just one person, acting as both the sole shareholder and director. This makes it a brilliant, go-to option for solo contractors and entrepreneurs. An LLP, on the other hand, must be set up by at least two members, which speaks to its roots as a formal partnership.

Registering either structure is a fairly painless online process these days, but the paperwork you need to prepare really highlights their fundamental differences.

To form a limited company, you’ll need:

For an LLP, the list is slightly different:

This last point is a major fork in the road. A company’s articles are public, offering total transparency. The privacy of an LLP agreement, however, lets partners keep their internal arrangements, like profit splits, completely confidential. If you're weighing up the costs, our guide on UK company registration fees breaks down the initial outlay.

Once your business is up and running, the admin requirements begin to diverge even more. Both structures have to file annually with Companies House and HMRC, but what they file is not the same.

Limited companies face a more structured set of duties. Every year, they must file a Confirmation Statement to confirm the details held at Companies House are correct. They also submit a set of annual statutory accounts, which gives the public a window into the company's financial performance. On top of that, a separate company tax return has to be sent to HMRC.

While both structures require you to be organised, the compliance framework for a limited company is generally more rigid and public. An LLP offers more internal flexibility and privacy, but this freedom depends entirely on having a robust, well-drafted members' agreement in place from day one.

An LLP’s filing obligations look a little different. It also files a Confirmation Statement and annual accounts. But because it doesn't pay Corporation Tax, it files a partnership tax return (the SA800) instead. From there, each member is responsible for filing their own personal Self Assessment tax return (SA100) and paying tax on their share of the profits. This really puts the onus on individual members to get their personal tax affairs right.

If you look at the official numbers, there's a clear winner in terms of popularity. Private limited companies vastly outnumber LLPs on the Companies House register. As of March 2025, there were 5,229,368 private limited companies, making up an incredible 92.6% of all corporate bodies. In contrast, there were only 52,109 LLPs, representing just 0.9%. This really shows the broad appeal of the limited company model for almost every type of business. You can dig into these corporate registration statistics on GOV.UK.

Your choice of business structure does more than just sort out your tax liabilities; it sends a powerful signal to the outside world. When it comes to raising capital, especially from venture capitalists and angel investors, the debate between a limited company and an LLP isn't much of a debate at all. The limited company wins, hands down.

This isn't just a matter of preference; it's rooted in the simple, universally understood mechanics of share capital. Investors get it. They can buy a tangible slice of your company, and their ownership is clearly defined. This straightforward process is the bedrock of equity investment in the UK.

For any ambitious startup with external funding on its roadmap, the limited company structure is the only realistic path forward. It's built from the ground up to accommodate investment by issuing new shares—a process that is both legally sound and commercially proven.

A limited company can also get creative, offering different classes of shares (like ordinary and preference shares) that come with different rights attached to voting or dividends. This flexibility lets founders keep control while offering investors more attractive terms to sweeten the deal. On top of that, limited companies can roll out tax-efficient incentive schemes to bring top talent on board.

The Enterprise Management Incentive (EMI) scheme is a perfect example. It's a government-backed initiative that lets smaller, high-growth companies grant share options to key employees with massive tax advantages. Crucially, EMI is only available to limited companies, giving them a serious edge in building a skilled team ready to scale.

An LLP, by its very design, just doesn't have this machinery. There's no share capital. To bring in an investor, you’d have to make them a member of the partnership. This completely changes the dynamic and is rarely an appealing setup for someone who just wants to provide financial backing.

Beyond the mechanics of fundraising, there’s the simple matter of public perception. That little 'Ltd' at the end of a company name carries real weight. It’s widely understood by the public to mean a formal, stable, and properly registered business. It projects an image of permanence and commercial credibility.

This isn’t to say LLPs lack credibility—far from it. In certain professional circles, the 'LLP' suffix is a badge of honour.

Perception by Sector:

Choosing the right structure, then, is also about aligning your business with the expectations of your customers, industry, and potential partners. If securing equity funding is a core part of your strategy, the decision is pretty much made for you.

For help structuring your finances to be investor-ready, the insight of a fractional finance director can give you the strategic oversight needed to prepare your company for its next phase. Getting this financial planning right is crucial for attracting serious investment.

Figuring out whether to go for a limited company or an LLP isn't about ticking boxes on a generic pros-and-cons list. It’s about asking the right questions—questions that get to the heart of what you want your business to become. Think of it as a compass, not a calculator.

Forget the one-size-fits-all advice. Your long-term vision is what matters here. By being honest about where you're headed, the right path usually becomes surprisingly clear.

Your answers to these three questions will quickly reveal which structure is a natural fit for your ambitions. Don’t rush them; each one points you in a very specific direction.

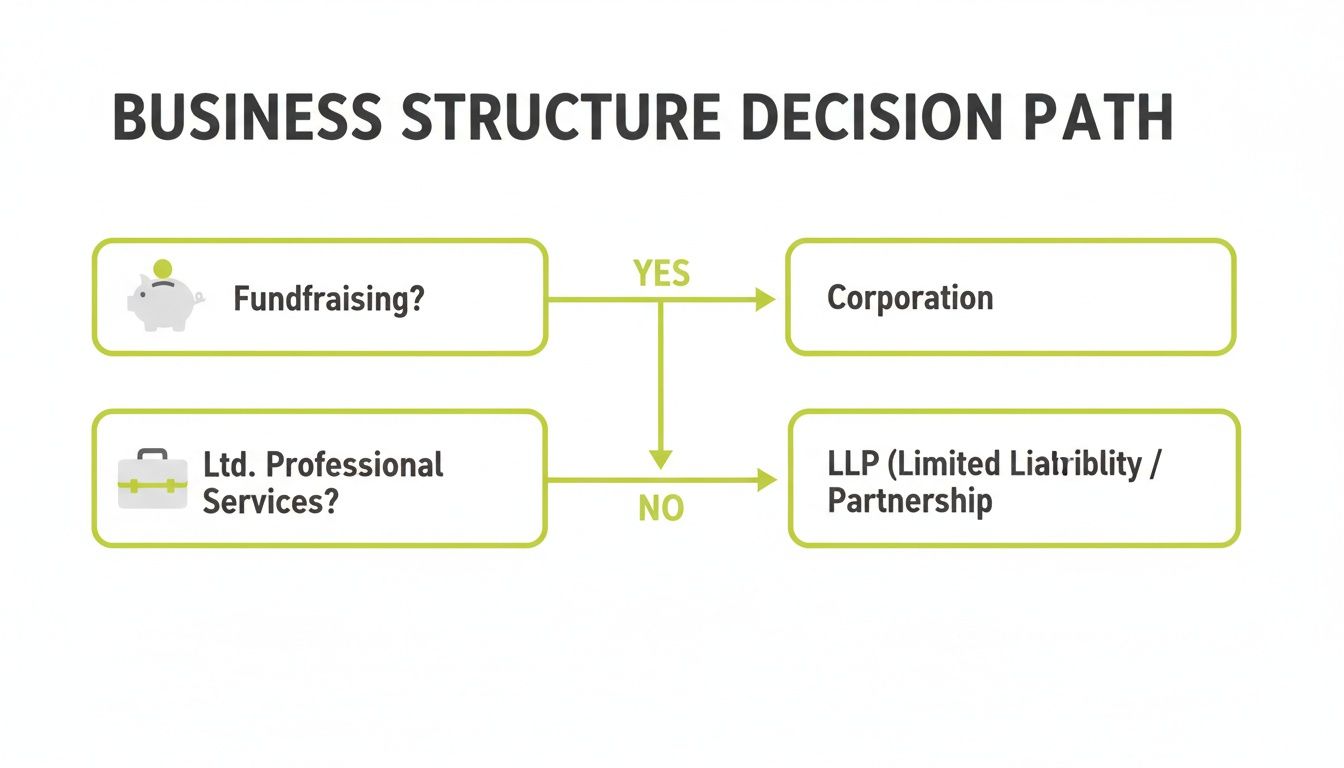

1. Is Raising External Equity Investment a Future Goal?

If there's even a slight chance you'll be seeking investment from venture capitalists or angel investors, your decision is pretty much made. It has to be a limited company. The entire investment world is built around share capital, something an LLP just doesn't have. Investors understand shares, share classes, and EMI schemes—they are the tools of the trade for bringing in outside capital.

2. Are You a Partnership of Qualified Professionals Distributing All Profits Annually?

This is the classic scenario for an LLP. Think accountants, solicitors, architects, or consultants working together. If your model is to share out the profits among the partners each year, the LLP structure is beautifully simple. Profits flow directly to the members, who then sort out their own tax through Self Assessment. This completely bypasses the two-step dance of Corporation Tax followed by dividend tax.

3. Will You Consistently Reinvest a Significant Portion of Profits Back into the Business?

For any business focused on scaling up, retaining profits is crucial for funding that growth. Here, the limited company is hands-down the more tax-efficient choice. Any profit you leave in the company is hit with Corporation Tax only, creating a pot of money you can use for expansion, hiring, or new equipment before any personal tax comes into play.

This decision-tree infographic helps visualise how these questions lead you down one path or the other.

As you can see, the need for future fundraising is a major fork in the road, almost always pointing towards a limited company. On the other hand, professional partnerships that share profits tend to find the LLP a much more comfortable home.

Let's boil this all down to the most common use cases. See if you can spot your own venture in one of these descriptions.

Choose a Limited Company if you are: A tech startup with big investment plans, a solo contractor or consultant, an e-commerce brand you want to grow, or really any business where you're building an asset that’s separate from its owners.

Choose an LLP if you are: A firm of accountants or lawyers, a medical practice with several partners, or any professional collaboration where members operate as a team and share the profits directly.

Ultimately, the choice between a limited company and an LLP really boils down to your strategic priorities. A limited company is built for growth, investment, and creating a separate corporate identity. An LLP is optimised for partnership, profit distribution, and professional collaboration.

Before you make a final call, it’s always a good idea to understand the full range of options available. Getting familiar with the different types of company structures in the UK will give you the confidence that your decision is the right one for your business's future.

Choosing between a limited company and an LLP isn't just a tick-box exercise. It brings up real-world questions about how your business will run day-to-day. Here are some of the most common queries we get from founders, with straight-talking answers.

Yes, you absolutely can, but be warned: it’s not just a simple paperwork shuffle. Moving from a limited company to an LLP, for instance, usually means you have to wind up the company and then transfer all its assets over to the new LLP.

This can trigger some hefty tax bills, like Capital Gains Tax on the assets being sold and even Stamp Duty if property is involved. The same headaches apply if you're going the other way.

Our Take: It's technically possible to convert, but it's a major legal and tax event. You're far better off spending the time now to pick the right structure from day one, rather than facing the cost and complexity of a switch later on.

In a word, no. An LLP is a partnership at its core, so you need a minimum of two designated members to keep it legal. The clue is in the name – Limited Liability Partnership.

If you're flying solo as a contractor, founder, or consultant, the limited company is the way to go. It’s designed to be run by just one person, who can be both the sole director and the only shareholder.

When it comes to keeping your affairs under wraps, the LLP has a distinct edge over a limited company.

No, they are quite different, and this is a key distinction. A limited company director has very specific legal duties laid out in the Companies Act 2006. These are strict obligations, like acting in the company's best interests and avoiding any conflicts of interest.

Designated members in an LLP have formal duties too, mostly around administrative compliance like filing accounts. But the wider duties that members owe to each other and to the LLP are defined in their private LLP Agreement. This gives them far more flexibility to decide their own rules of engagement compared to the rigid statutory duties of a director.

Making the right choice between a limited company and an LLP is one of the most important decisions you'll make when starting out. The team at GenTax Accountants can walk you through the tax and compliance implications for your unique situation, making sure you start on solid ground. For tailored advice on getting your business structure right, get in touch with GenTax today.