Setting yourself up as a sole trader is the simplest way to get a business off the ground in the UK. The process is surprisingly direct: once your earnings from trading top £1,000 in a tax year, you just need to let HMRC know you're self-employed. This no-fuss setup is why it’s the go-to structure for countless freelancers, contractors, and first-time entrepreneurs.

When you start out as a sole trader, you are the business. There’s no legal distinction between you and the enterprise you run, which is a massive advantage. It cuts out the complex paperwork and fees that come with forming a limited company.

For many, it's the perfect entry point into the world of self-employment. The low barrier to entry and having complete control over your own decisions make it a really attractive option. You set your own prices, decide which services to offer, and keep all the profits after tax.

Pretty much anyone can register as a sole trader in the UK, as long as you have the legal right to work here. If you've started a side hustle, picked up some freelance work, or even turned a hobby into a bit of cash, you're probably already operating as one without realising it.

The official trigger for registering with HMRC is your income. As soon as you earn more than the £1,000 tax-free trading allowance in a single tax year (that runs from 6th April to 5th April), you are legally required to register for Self Assessment.

This structure is overwhelmingly popular, and for good reason. As of 2025, there are a staggering 3.2 million sole proprietorships, making up 57% of the entire UK private sector business population. That figure grew by 5% between 2024 and 2025 alone, showing just how appealing it continues to be for new ventures.

While the setup is simple, there are a few crucial things to get your head around from day one. The biggest is unlimited liability. Because you and your business are the same legal entity, you are personally on the hook for any business debts. This means your personal assets could be at risk if the business runs into financial trouble.

Key Takeaway: As a sole trader, your personal finances and business finances are legally intertwined. This means you are personally liable for all business debts, a critical distinction compared to the limited liability protection offered by a limited company.

This is a fundamental concept that every new sole trader needs to grasp. It sounds intimidating, but for most small businesses—especially those in low-risk sectors like freelance writing or consulting—it’s a manageable risk.

Before diving into the registration process, it’s always a good idea to have a clear business plan. If you're looking for a wider view on launching a new venture, our comprehensive guide on https://www.gentax.uk/blog/how-to-start-a-business-uk-guide covers everything from planning to launch. For a broader look at different business structures, this guide on how to register a business in the UK provides further details on various registration types.

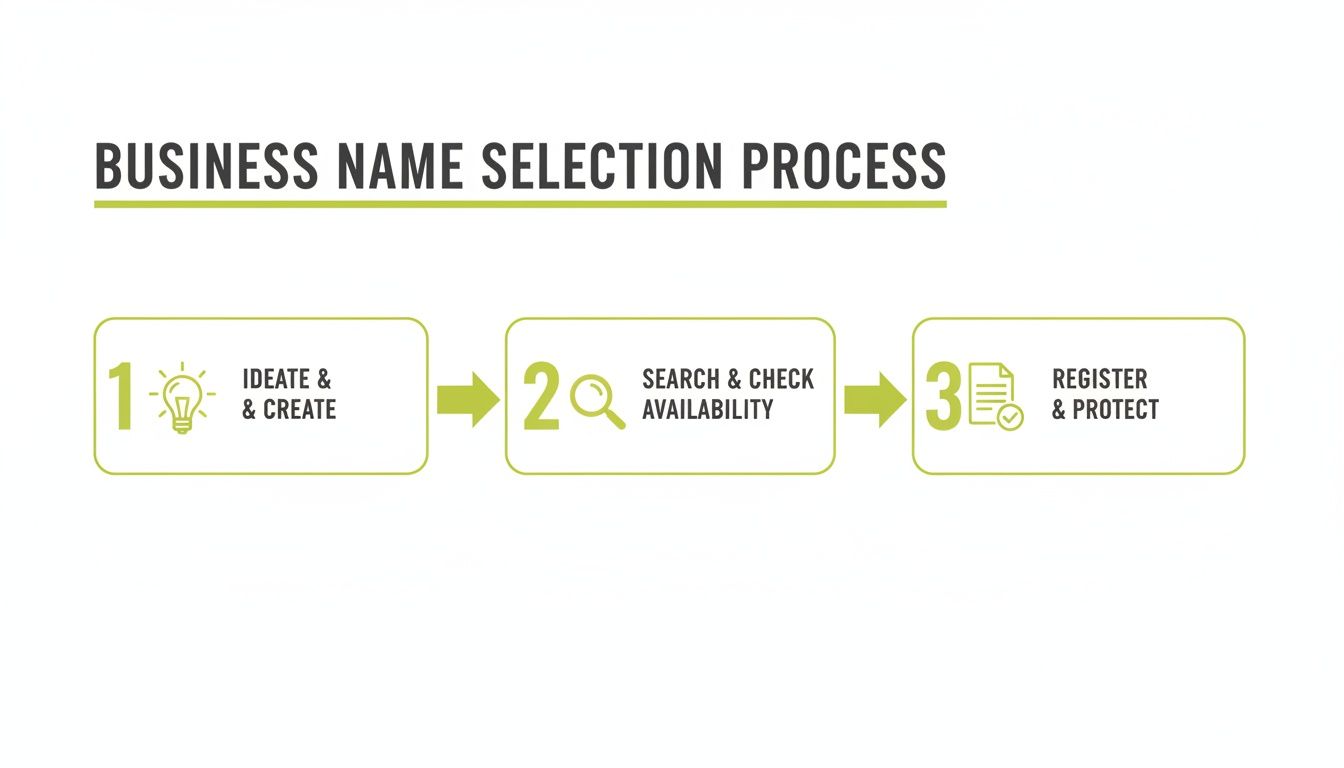

Alright, let's get to one of the more exciting first steps: picking a name for your business. This is your chance to stamp your identity on what you do, but it’s not just about finding something that sounds good. There are a few crucial rules you need to follow to stay on the right side of the law and build a brand that lasts.

First off, your name can’t be offensive, and you can't use certain 'sensitive' words or phrases without official permission. Think words like ‘Accredited’, ‘Royal’, or ‘Trust’ – they imply an official seal of approval, and HMRC is keen to stop businesses from misleading the public.

It also can’t be identical to an existing trademark. Let's say you're a freelance graphic designer named Alex Smith. Trading as 'Alex Smith Designs' is perfectly fine and makes total sense. But calling yourself 'Apple Designs'? You’d be inviting a very serious—and expensive—legal letter from a certain tech giant.

To save yourself a headache down the line, do a quick search on the Companies House register and the UK's trademark database. Even though as a sole trader you don’t register with Companies House, this search will tell you if a limited company is already using your name. That's a recipe for customer confusion you really want to avoid.

The government provides clear guidelines on the do's and don'ts for sole trader business names.

This official guidance is your go-to resource. It confirms a key rule: you must include both your own name and your business name on official paperwork like invoices. It’s all about transparency, making sure your clients know exactly who they're dealing with.

Beyond the legal checks, think practically. Is the domain name available? Are the social media handles free on platforms like Instagram, Facebook, and LinkedIn? Nailing these down early gives you a consistent online identity, making you much easier for customers to find and remember.

Next up, you’ll need a business address. For most people starting out, using your home address is the simplest and most common choice. It’s free, requires zero extra admin, and is perfectly fine as far as HMRC is concerned.

But there’s a big catch: privacy. This address will be plastered on your invoices and could end up in public directories. Not everyone is comfortable with that.

Privacy Tip: Using your home address is easy, but it puts your private information out there. If you’d rather keep your personal and professional lives separate, look into a virtual office address or a P.O. Box.

A virtual office is a brilliant alternative. For a monthly fee, you get a slick, professional-looking address in a city centre to use on all your documents. These services typically handle your mail and forward it on, giving your business a more established feel while keeping your home address private.

Finally, remember that your business name and address are foundational pieces of your financial identity. As soon as you can, getting a separate bank account is a non-negotiable step for keeping your books clean. Our guide on how to set up a business bank account walks you through why it’s so important and how to get it done right from the start.

Alright, you've chosen a business name and sorted your address. Now for the bit that often feels the most intimidating: making things official with HMRC. Don't worry, this isn't nearly as scary as it sounds. In reality, it's a logical, step-by-step process.

Think of it this way: you're simply letting the government know you've started earning your own money. Registering as a sole trader in the UK is designed to be straightforward. You don't need to stump up any capital, and you aren't creating a separate legal entity like a limited company. It's just you, trading under your own name.

There’s a reason it’s such a popular route. There are over 3 million sole proprietorships in the UK, which makes up a whopping 56% of all businesses. What's even more telling is that 93.57% of them are one-person bands with no employees, according to figures from money.co.uk. This just shows the incredible scale of individual enterprise in this country.

This simple graphic shows how choosing your name flows directly into the registration process.

As you can see, once the name is locked in, the next logical step is telling the authorities you're open for business.

Before you dive into the online forms, do yourself a favour and gather all your details first. Trust me, it makes the whole thing much smoother and quicker. You can get it all done in about 15 minutes if you're prepared.

Here’s a quick checklist of what to have on hand:

Having this little pile of info ready means you won't be scrambling to find documents halfway through.

If there’s one date to circle in your calendar right now, it’s this one: 5th October. You are legally required to register for Self Assessment by the 5th of October that follows the end of the tax year you started trading in. Remember, the UK tax year runs from 6th April to 5th April.

Let’s make that real. Imagine a new graphic designer, Ben, lands his first paid client project on 1st August 2024.

Missing this deadline isn't a great start. It can land you a £100 penalty, so it's a date to take seriously. My advice? Just register as soon as you know you’ll earn more than the £1,000 trading allowance. Don't leave it to the last minute.

To give you a clearer picture of the journey ahead, here’s a table outlining the key milestones in your first year.

These dates form the basic rhythm of your compliance duties as a sole trader. Getting them in your calendar early is one of the best habits you can form.

The easiest and most common way to get registered is online via the Government Gateway. If you've never filed personal taxes online before, you’ll need to set up an account first.

Once you’re logged in, you're looking for the 'Register for Self Assessment' service. The form itself is pretty intuitive; it simply asks for the information you've already gathered. It’s designed to be used by everyday people, not just accountants.

What to Expect After Registering: Once you've hit submit, HMRC gets to work. You'll receive a confirmation letter in the post, usually within a couple of weeks. This letter is really important because it contains your 10-digit Unique Taxpayer Reference (UTR) number.

Your UTR is your golden ticket for all things Self Assessment. You’ll need it to file your tax return, so keep that letter somewhere safe. It can take up to 15 working days to arrive, so don't panic if it's not there the next day.

And that’s it. Once you have your UTR, you are officially on HMRC’s books as a sole trader. Your next big job is to get into the habit of keeping meticulous records of your income and expenses, which will make your first tax return a breeze. This whole process is set to change slightly with the move to digital record-keeping, which you can read all about in our guide on Making Tax Digital for Self Assessment.

Once that Unique Taxpayer Reference (UTR) number lands on your doormat, you’re officially in business in HMRC’s eyes. It’s a huge milestone, but it also kicks off a whole new set of financial responsibilities. Getting your head around how tax and National Insurance work from day one is absolutely crucial for staying compliant and avoiding any nasty surprises down the line.

The first thing to get straight is that as a sole trader, you pay Income Tax on your business profits, not your total turnover. This is a vital distinction. Your profit is simply what's left after you deduct all your allowable business expenses from your total income. That final figure is what you'll be taxed on.

This is all managed through your Self Assessment tax return, which you'll need to complete and file each year. Think of it as a detailed summary of your business's financial performance that tells HMRC how much tax and National Insurance you owe.

The amount of Income Tax you’ll pay boils down to how much profit you make. The UK has a progressive tax system with different bands, which just means you pay different rates on different portions of your income.

The good news is that everyone gets a Personal Allowance—an amount you can earn each year before you start paying any Income Tax at all. For the 2024/25 tax year, this is £12,570.

Here’s a quick breakdown of the Income Tax bands for England, Wales, and Northern Ireland (Scotland has its own system):

It might seem complicated, but it just means your first chunk of profit up to £12,570 is completely tax-free. You then pay 20% on the next portion, and so on. Getting familiar with these thresholds helps you anticipate your tax bill and, most importantly, put enough money aside.

If you want to dig deeper into planning your finances, our guide offering tax advice for small businesses is a great place to start.

Alongside Income Tax, most sole traders will also pay two types of National Insurance Contributions (NICs). These payments are what contribute towards your state benefits, like the State Pension, Maternity Allowance, and Bereavement Support Payment.

The two you need to know about are Class 2 and Class 4. They work in different ways and are triggered by different profit levels.

Key Insight: Think of Class 2 as your ticket to accessing state benefits and Class 4 as a tax on your profits. Both are a mandatory part of being self-employed, but they serve different functions in the UK's social security system.

Class 2 NICs used to be a flat weekly rate, but the rules changed significantly from 6 April 2024. Now, if your profits are over £12,570, you get the NI credits automatically without having to pay anything.

If your profits are below £6,725, you won't get those credits automatically, but you can choose to make voluntary Class 2 payments to protect your entitlement to state benefits.

Class 4 NICs are calculated as a percentage of your annual profits, much like Income Tax. You only start paying Class 4 once your profits exceed a certain threshold.

For the 2024/25 tax year, you'll pay 6% on profits between £12,570 and £50,270, and then just 2% on any profits above that.

Let’s imagine Sarah, a freelance web developer, makes a profit of £40,000 in her first year. How would her tax and NI bill be calculated for the 2024/25 tax year?

Income Tax Calculation:

National Insurance Calculation:

In this scenario, Sarah's total bill for the year would be £5,486 (Income Tax) + £1,645.80 (Class 4 NI) = £7,131.80. Budgeting for this amount throughout the year is absolutely essential to avoid a last-minute panic.

As your business grows, you might need to register for other schemes. The most common one is Value Added Tax (VAT). You are legally required to register for VAT if your VAT-taxable turnover exceeds £90,000 in a rolling 12-month period. It’s also possible to register voluntarily if it benefits your business.

Another big trigger is hiring your first employee. If you decide to take someone on, you must register as an employer with HMRC and operate a Pay As You Earn (PAYE) scheme. This means you’ll be responsible for deducting tax and NI from your employee's wages and paying it to HMRC.

These are significant steps that bring extra admin, so it’s always wise to plan for them well in advance.

Now that we’ve covered your tax obligations, let's talk about building the financial habits that make managing them straightforward. Believe me, great record-keeping isn't just about appeasing HMRC; it's the foundation of a healthy, stress-free business. Think of it as the control panel for your enterprise—it shows you what's coming in, what's going out, and where your money is really going.

Getting this right from day one will save you countless hours of panic when your first Self Assessment deadline looms. HMRC requires you to keep accurate records for at least five years after the 31st January submission deadline of the relevant tax year, so you need a reliable system for tracking every penny. It doesn't have to be complicated, but it does have to be consistent.

HMRC isn't trying to catch you out; they just need proof of the figures you report on your tax return. Your record-keeping system simply needs to capture all your business's financial activities.

At a minimum, you must keep a clear record of:

Keeping your business bank statements is also essential as they provide a clear trail of all transactions. For many service-based businesses, client bookings are a core part of their operational records. To keep things organised, you might want to look into an efficient booking system once you're up and running.

When it comes to how you keep these records, you really have two main options: a simple spreadsheet or dedicated accounting software.

A basic spreadsheet can work perfectly well when you're just starting out. You can create columns for the date, a description, income, and various expense categories. It’s free and gives you a decent overview.

However, as your business grows, a spreadsheet can quickly become unwieldy and prone to errors. This is where cloud accounting software comes in. These platforms are designed for business owners, not accountants, and they automate so much of the hard work. They can link directly to your business bank account, help categorise expenses, and generate professional invoices in seconds.

Our Take: While a spreadsheet is a good starting point, investing in user-friendly accounting software early on is one of the smartest moves you can make. It not only prepares you for Making Tax Digital but also gives you real-time insights into your business's financial health.

If you're considering this route, it's worth exploring your options. You can learn more about the best cloud accounting software for startups in our detailed guide.

One of the biggest financial wins for any sole trader is getting to grips with allowable expenses. These are the day-to-day running costs of your business that you can deduct from your income before calculating your tax bill. The more allowable expenses you claim, the lower your profit figure, and the less tax you pay. It really is as simple as that.

The golden rule from HMRC is that an expense must be "wholly and exclusively" for business purposes.

Common examples of allowable expenses include:

Keeping detailed receipts for every single one of these is non-negotiable. A blurry photo on your phone is better than nothing, but a clear digital copy saved in your accounting software is the gold standard. It ensures you have the evidence to back up your claims and maximises your tax savings, turning what feels like a tedious admin task into a profitable habit.

Once you’re officially registered, a whole new set of practical questions will inevitably pop up. These are the “what now?” queries that take you from the initial setup phase into the day-to-day reality of running your own show. We’ve pulled together the most common ones we hear from new sole traders to give you some clear, straightforward answers.

One of the first things people ask is, “Can I be a sole trader while I’m still employed?” The answer is a big, resounding yes. It’s incredibly common for people to launch a side hustle or start freelancing while holding down a full-time or part-time job.

HMRC is perfectly happy with this arrangement, but it does add an extra layer to your tax affairs. Your salary from your job is handled through PAYE, meaning your employer deducts tax for you. Your sole trader income, however, is a different story. You’ll need to report it separately on your annual Self Assessment tax return. HMRC will then look at your total income from all sources to figure out the correct tax you owe.

Another frequent question is getting to grips with the difference between being a sole trader and setting up a limited company. While they're both legitimate ways to structure a business, they are worlds apart in terms of liability, admin, and tax.

Think of it this way: as a sole trader, you are the business. There’s no legal separation, which means you have unlimited liability. If your business racks up debts, your personal assets—like your home or savings—could be on the line.

A limited company, on the other hand, is a completely separate legal entity. This creates a protective wall between your business and personal finances, giving you limited liability. Your personal assets are safe from business debts.

This core difference creates a knock-on effect on everything from your paperwork to your tax planning options.

Key Takeaway: The choice often boils down to risk and revenue. The sole trader route is simpler and cheaper to manage, but a limited company offers crucial financial protection and better tax planning opportunities for a growing business.

Finally, the one question on almost every new sole trader’s mind: "How much money do I actually need to save for my tax bill?" This is a critical habit to get into from your very first invoice. Getting this wrong can lead to a world of financial stress down the line.

There isn’t a single magic number, but a solid rule of thumb is to open a separate bank account just for your tax. I call it a "tax pot".

Every single time a client pays you, transfer 25-30% of that income straight into this dedicated account. For most people earning within the basic rate tax band, this buffer will comfortably cover both your Income Tax and your Class 4 National Insurance contributions.

This simple discipline means the money is ready and waiting when the 31st January payment deadline rolls around. It transforms your tax bill from a nasty surprise into a predictable, manageable business expense.

Navigating these questions is all part of the journey. At GenTax Accountants, we specialise in helping sole traders move forward with confidence, turning financial confusion into clarity. To see how we can support your business from day one, get in touch with our expert team today.