As a sole trader, there’s one number you really need to keep an eye on: your taxable turnover. Once it crosses a certain line in any 12-month period, you are legally required to register for VAT. This isn’t optional—it’s a fundamental rule designed to bring growing businesses into the VAT system.

Getting this right is your first major step in handling VAT correctly.

Let’s cut through the jargon. Value Added Tax, or VAT, is a tax added to most goods and services. Think of it like a tax relay race. The tax gets passed along at each stage of the supply chain—from manufacturer to wholesaler to you—but it's the final customer who ultimately foots the bill. Your job is simply to collect it and pass it on to HMRC.

The most critical part for you is the mandatory registration threshold. It’s the trigger point where the law says your business must register with HMRC and start charging VAT. If you're getting close, it's worth reading up on understanding the VAT registration threshold to prepare.

This is where a lot of sole traders get tripped up. Taxable turnover is not your profit. It’s not even your total income. It's the total value of everything you sell that isn't specifically exempt from VAT.

So, what counts towards it?

Pay close attention to that last one. Even sales with 0% VAT are included when you're calculating your turnover for registration purposes. To see how the numbers break down, check out our guide on the current VAT registration threshold.

Here’s another common pitfall. The VAT threshold isn't based on the tax year (April to April). It’s based on a rolling 12-month period. This catches so many people out and can lead to some uncomfortable letters and penalties from HMRC.

To stay on the right side of the rules, you need to check your turnover at the end of every single month. Simply look back over the last 12 months and add up your total taxable sales.

For instance, at the end of May, you’d tally up your total turnover from 1st June of last year right through to 31st May of this year. If that total goes over the threshold, it’s time to register.

This constant monitoring is key. In the UK, a sole trader must register for VAT as soon as their taxable turnover in a rolling 12-month period goes over £90,000. If you're expecting to cross this threshold in the next 30 days alone, you also need to register immediately.

Use this quick table to see if you're nearing the point of mandatory registration.

Staying on top of your turnover means you’ll know the exact moment you need to act, helping you avoid penalties and keep your business finances in good order.

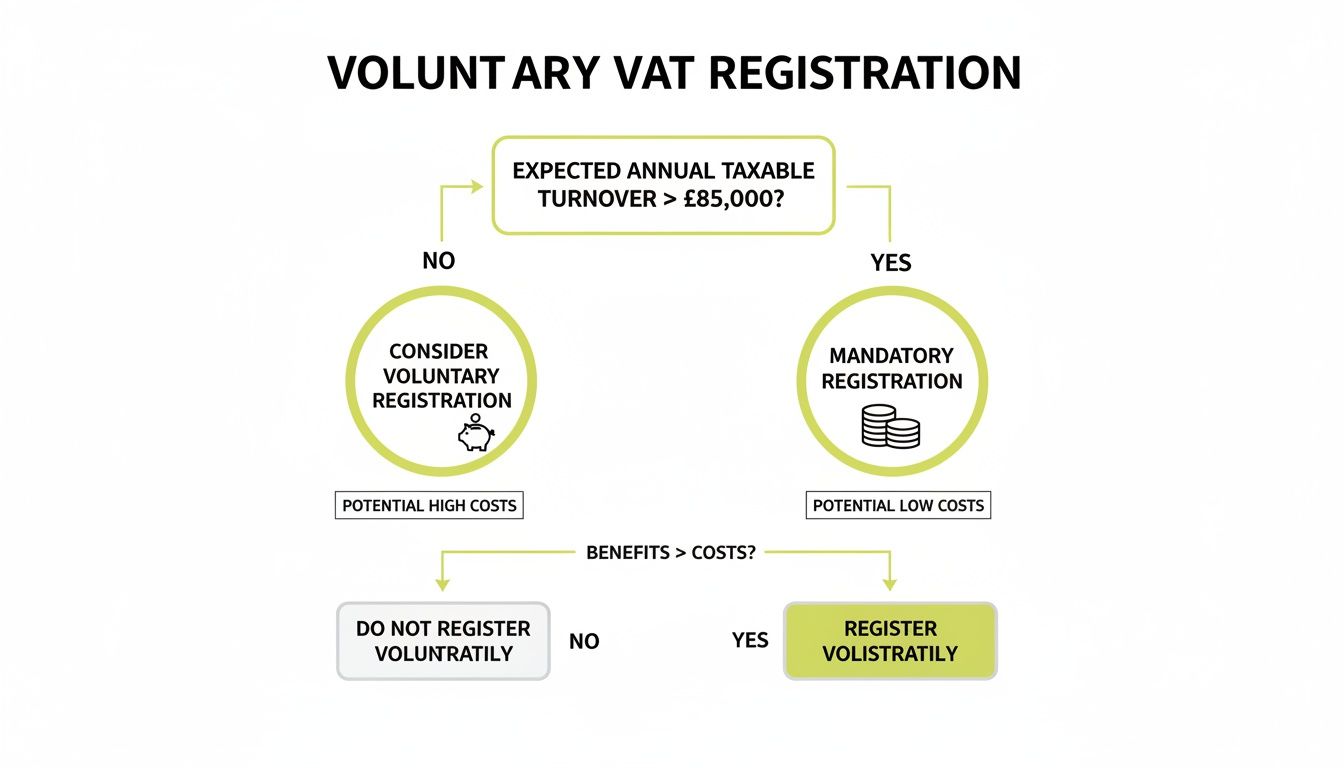

Just because your turnover is below the VAT threshold doesn't mean you can ignore it altogether. As a sole trader, you have the option to register voluntarily, and for some, it’s a seriously smart move. But it's not a decision to be taken lightly.

Before you jump in, you need to weigh up the benefits against the extra admin that comes with it. For certain types of sole traders, registering early can unlock some big financial advantages. For others, it just adds unnecessary complexity and cost. The right choice really boils down to your business model, your expenses, and, most importantly, who your customers are.

The single biggest reason to think about voluntary registration is the ability to reclaim input VAT. This is the VAT you pay on your business purchases – everything from stock and materials to software subscriptions and your accountant’s fees.

If your business has hefty running costs or you need to make big upfront investments, the savings can really stack up. Imagine you’re a freelance web developer buying a new high-spec laptop for £2,400. That price includes £400 in VAT. If you're registered, you can claim that £400 back from HMRC.

But it’s not just about direct savings. There are other perks too:

The crucial takeaway here is that voluntary registration makes the most sense for sole traders who sell to other VAT-registered businesses and have significant VAT-rated expenses themselves.

Of course, it’s not all good news. The most immediate challenge is what registration does to your pricing, particularly if you sell directly to the public. Once you’re registered, you must add VAT to your sales.

If your customers aren't VAT registered (think B2C), they can't reclaim this tax. This means your service effectively becomes 20% more expensive for them overnight. You’re then stuck with a tough choice: do you absorb the VAT cost and take a hit on your profit margins, or pass it on and risk pricing yourself out of the market?

Here are the main drawbacks to think about:

Let's look at two very different scenarios. A self-employed builder who buys thousands of pounds of materials each month stands to reclaim a lot of input VAT, and their clients (who are often other businesses) can reclaim the VAT they charge. It's a win-win.

Now, consider a freelance writer with very few expenses who mainly works for small, non-VAT registered businesses. For them, the administrative headache would almost certainly outweigh any tiny benefit. It just wouldn't make sense.

Once you’re VAT registered, HMRC automatically puts you on the standard scheme. This means totting up the VAT on every single sale and purchase, which can quickly become a headache for a busy sole trader.

Thankfully, there are a few other schemes designed to make life easier for small businesses. Picking the right one can seriously cut down your admin time and even give your cash flow a welcome boost. The trick is understanding how each one works and which fits your business like a glove.

Let's break down the main options.

Imagine boiling down all your VAT calculations to one simple percentage. That’s the big idea behind the Flat Rate Scheme. Instead of tracking the VAT on every single expense, you pay HMRC a fixed, lower percentage of your total VAT-inclusive turnover.

This percentage depends on your industry, and it's always lower than the standard 20% rate. Why? Because it’s designed to account for the fact that you can't reclaim VAT on most of your day-to-day purchases.

This scheme is a fantastic fit for sole traders who don't spend a lot on business expenses—think consultants, writers, or IT contractors. If your outgoings are pretty minimal, the simplified maths often means you end up paying less to HMRC over the year.

Cash flow is the lifeblood of any sole trader. The Cash Accounting Scheme is built from the ground up to help you protect it. On the standard scheme, you owe HMRC the VAT the moment you raise an invoice—whether your client has paid you or not.

This can create a massive cash flow problem, leaving you to foot a tax bill with money that’s not even in your bank account yet. The Cash Accounting Scheme flips that on its head.

You only account for VAT when money actually moves. You pay VAT on your sales once you've been paid by your customers, and you reclaim VAT on purchases once you've paid your suppliers.

This gives you a much healthier, real-time view of your finances and means you’ll never pay VAT on a bad debt. To join, your estimated VAT-taxable turnover needs to be £1.35 million or less.

This flowchart gives you a simple way to visualise if voluntary VAT registration—the first step before choosing a scheme—is a smart move for you.

As you can see, if you have high business costs, registration becomes much more attractive because you can start reclaiming significant amounts of VAT.

If your number one priority is to slash your admin time, the Annual Accounting Scheme could be your perfect match. Instead of filing four quarterly VAT returns a year, you only have to submit one.

You make regular advance payments towards your final VAT bill throughout the year (monthly or quarterly), which are based on an estimate from your last return. At the end of the year, you file your single return and either make a final top-up payment or get a refund if you’ve paid too much.

This scheme smooths out your payments and dramatically reduces your paperwork. Just like the Cash Accounting Scheme, you’ll need an estimated VAT-taxable turnover of £1.35 million or less to be eligible.

Juggling VAT can be tricky, and getting professional help often provides much-needed peace of mind. You can find out more about how we support sole traders with their VAT returns.

To help you decide, here’s a quick comparison of how the different schemes stack up against each other.

This table breaks down the main features of each scheme to help you see at a glance which one might be the best fit for your sole trader business.

Ultimately, choosing the right scheme is a critical decision. By matching your VAT admin to the way your business actually works, you can save yourself a huge amount of time, improve your cash flow, and get back to focusing on what you do best.

Making Tax Digital, or MTD, has been a pretty big shift for all VAT-registered businesses, and that includes sole traders. If the name sounds a bit daunting, don't worry – it's much simpler in practice. The best way to think of it is swapping an old-school paper filing system for a smart, digital one that does most of the heavy lifting for you.

At its heart, MTD is HMRC’s way of making tax admin more accurate, efficient, and straightforward for everyone. For you as a sole trader, it boils down to two key things: you now have to keep your VAT records digitally, and you must file your VAT returns using special MTD-compatible software. The days of scribbling numbers on a paper form and popping it in the post are officially over.

To get on board with MTD, you need to use software that can talk directly to HMRC's systems. This isn’t just about using a standard spreadsheet; it has to be a program that's been specifically approved to submit your VAT information.

Some of the most popular choices for sole traders include:

Once you pick your software, you’ll need to grant it permission to connect to your HMRC account. This creates a secure digital link, allowing your VAT return to be sent straight from your records to HMRC with just a couple of clicks. It's not just easier; it also slashes the risk of making typos or other manual errors.

MTD isn’t just another bit of admin to tick off. When you keep digital records, you get a live, accurate view of your business's financial health. This puts you in a much better position to make smart, informed decisions day-to-day.

Under the MTD rules, your software needs to capture a few specific details for every single transaction. We're not just talking about saving a PDF of an invoice; it's about logging the core data in a digital format.

For every sale you make, you must digitally record:

And for every business purchase you make, you need to log:

By keeping these details up-to-date in your software, you can be confident that your VAT returns are calculated correctly right from the source. This system doesn't just keep HMRC happy; it gives you a crystal-clear picture of your cash flow and profitability throughout the year. As your business expands, these digital habits will become invaluable, especially as Making Tax Digital for Self Assessment will also be coming your way in the future.

Once you're VAT registered, your paperwork suddenly becomes one of your most important tools. Getting your invoicing and record-keeping sorted from day one is the secret to a stress-free relationship with HMRC. This isn't just about ticking boxes; it’s about creating a crystal-clear financial story for your business.

Think of it this way: your VAT records are the evidence that backs up every single figure you submit on your returns. Without solid proof, you can’t reclaim the VAT on your purchases, and you could find yourself facing some very awkward questions during an inspection.

Once you’re registered, a standard invoice just won’t cut it anymore. You are legally required to issue a proper VAT invoice that contains specific information. If you miss even one detail, your business client might not be able to reclaim the VAT, which can lead to payment delays and a lot of unnecessary frustration.

Your VAT invoice must clearly show:

Beyond these basics, the financial breakdown is absolutely crucial. You have to itemise the net cost of each item, the VAT rate you’ve applied, and the total VAT amount. For sole traders, this level of transparency is non-negotiable.

A valid VAT invoice is more than just a request for payment; it's a legal document. It provides the official evidence needed for you to account for the VAT you've charged and for your business customers to reclaim the VAT they've paid.

Under the Making Tax Digital (MTD) rules, all VAT-registered businesses must keep digital records. This means managing your accounts using compatible software that connects directly to HMRC's system. It’s not a suggestion; it’s the law.

Your digital records need to be a complete log of every sale and every purchase. Keeping these financial documents in good order is essential, especially when thinking about MTD rules or a potential audit. You can learn how to organize business receipts effectively to stay audit-ready and build good digital habits from the start.

HMRC requires you to keep all your VAT records for at least six years. This includes your VAT account, all invoices and receipts, and any paperwork related to imports or exports.

One of the big perks of being VAT registered is the ability to reclaim the VAT on your business expenses. This is known as input VAT. The key rule here is that you can only reclaim VAT on purchases that are genuinely and exclusively for your business.

Common examples of reclaimable expenses for a sole trader include:

There are some strict exceptions, though. For example, you generally can't reclaim VAT on client entertainment costs. And if a purchase is for both business and personal use, you can usually only reclaim the business portion of the VAT.

Using one of the best cloud accounting software for startups makes managing all of this so much easier. These platforms help you tag expenses, store digital receipts, and automatically calculate the VAT you can reclaim, which makes filing your quarterly returns far simpler and more accurate.

Even once you've got your head around the basics, VAT can still throw a few curveballs. Let's tackle some of the most common questions that crop up for sole traders, giving you clear, practical answers to navigate those tricky grey areas.

This is a classic scenario. You land one big project, and suddenly your turnover for the month pushes you over the £90,000 threshold. What now? The standard rule is pretty clear-cut: you must register for VAT within 30 days of the end of the month you went over the limit.

But what if you know for a fact it was a one-off? If you have a solid reason to believe your turnover will drop back below the deregistration threshold (£88,000) in the next 12 months, you don't have to just accept it. You can actually apply for a registration ‘exception’ from HMRC.

To do this, you need to write to HMRC and lay out your case with clear evidence. This could be proof that a large, non-recurring contract has now ended. The key is to be proactive. Just ignoring the registration requirement is a surefire way to attract penalties. If HMRC turns down your application, you’ll have to register for VAT backdated to the original required date.

Yes, and this is a fantastic perk that often gets overlooked! It can seriously soften the financial blow of becoming VAT registered. HMRC lets you reclaim VAT on certain goods and services you bought before your registration date, as long as they were for your business.

The rules are a little different for goods versus services:

You'll need to have kept the valid VAT invoices for all these purchases, of course. This potential reclaim is a massive factor to weigh up if you're thinking about registering voluntarily.

This is probably the single most important strategic question you'll face when you first register. The moment you're registered, you are legally required to add VAT (currently 20% on most things) to your prices. How this lands depends entirely on who your customers are.

If your clients are other VAT-registered businesses (B2B), it’s not a huge deal. They can simply reclaim the VAT you charge them, so from their perspective, your service doesn't actually get more expensive. But if your customers are the general public or non-VAT-registered businesses (B2C), your price just jumped by 20%.

This leaves you with a tough decision. Do you swallow that 20% yourself, which eats directly into your profit margin? Or do you pass it on to your customers, potentially making you less competitive than your non-registered rivals? It is absolutely essential to analyse your customer base before you commit. Getting this wrong can sting, and it's an area where getting proper advice for sole traders is worth its weight in gold.

This is a common point of confusion, but the distinction is absolutely vital for keeping your VAT accounting straight. While neither involves charging your customer VAT, HMRC treats them very differently, and it impacts your turnover calculations.

Zero-Rated Supplies: Think of these as items that are technically in the VAT system, but the rate is simply set at 0%. Classic examples include most food, books, and children's clothing. Sales of zero-rated items do count towards your VAT registration threshold. Crucially, you can still reclaim the input VAT on costs related to making these sales.

VAT-Exempt Supplies: These are goods and services that are completely outside the scope of VAT. Think insurance, postage stamps, and certain financial services. Sales of exempt items do not count towards your VAT registration threshold, and you cannot reclaim any input VAT on costs associated with them.

If your business provides a mix of standard, zero-rated, and exempt supplies, your VAT returns will get more complicated and you may need to do partial exemption calculations.

Navigating the world of VAT, from figuring out registration to staying compliant, can feel like a full-time job in itself. At GenTax Accountants, we specialise in taking the stress out of tax so you can get back to what you do best: running your business. Discover how our dedicated accounting services can support your sole trader journey.