Getting to grips with corporation tax isn't just about paying what you owe; it's about smart, proactive planning. Think of it as a strategic game where understanding the rules allows you to legally minimise your bill. It’s not about finding loopholes, but about using HMRC’s own frameworks—from R&D tax credits to pension contributions—to your advantage.

Before you can get clever with tax-saving strategies, you need to have the fundamentals locked down. Don't see corporation tax as a fixed, unavoidable cost. Instead, view it as a figure you can influence through careful financial management throughout the year.

This mindset shift is everything. It turns tax from a reactive chore into a powerful tool for improving your company's bottom line. For a more detailed breakdown of the basics, our guide on what is corporation tax is a great place to start.

Put simply, if you run a UK limited company that turns a profit, you're on the hook for corporation tax. The same goes for many other organisations, like clubs and societies. It’s a non-negotiable part of operating as a limited company.

But here’s the crucial bit: the tax is calculated on your profits, not your total income or turnover. This distinction is the bedrock of tax planning. Every pound you spend on a legitimate, allowable business expense directly reduces your taxable profit, which in turn cuts your corporation tax bill.

Since the financial year beginning 1 April 2023, the main rate for corporation tax sits at 25%. This is the rate for companies with profits exceeding £250,000.

However, it's not a one-size-fits-all situation, especially for smaller businesses.

A "small profits rate" of 19% applies to companies with profits of £50,000 or less. If your profits fall between £50,001 and £250,000, a system called Marginal Relief comes into play, creating a sliding scale where your effective tax rate gradually climbs from 19% towards 25%.

Getting your dates wrong with HMRC is an easy way to pick up penalties, so it's vital to have these two deadlines etched into your calendar for every accounting period.

Here’s a common trip-up: you must pay the tax before you file the return. It feels counterintuitive, but overlooking this detail can lead to fines you really don't need.

One of the most straightforward ways to bring down your taxable profit is to get forensic about claiming every single allowable expense. So many business owners I see stop at the big, obvious costs like office rent and utility bills. But if that’s all you’re doing, you're almost certainly leaving money on the table.

Real tax efficiency lives in the details—all those smaller costs you might not immediately flag as 'business' spending.

This is where you need a bit of a mindset shift. Any legitimate cost you incur that is "wholly and exclusively" for your business can be knocked off your profit figure. If you're running a growing digital agency, for example, this could be anything from your monthly project management software subscription to tickets for an industry conference. They aren't just running costs; they're strategic levers for pulling down your corporation tax bill.

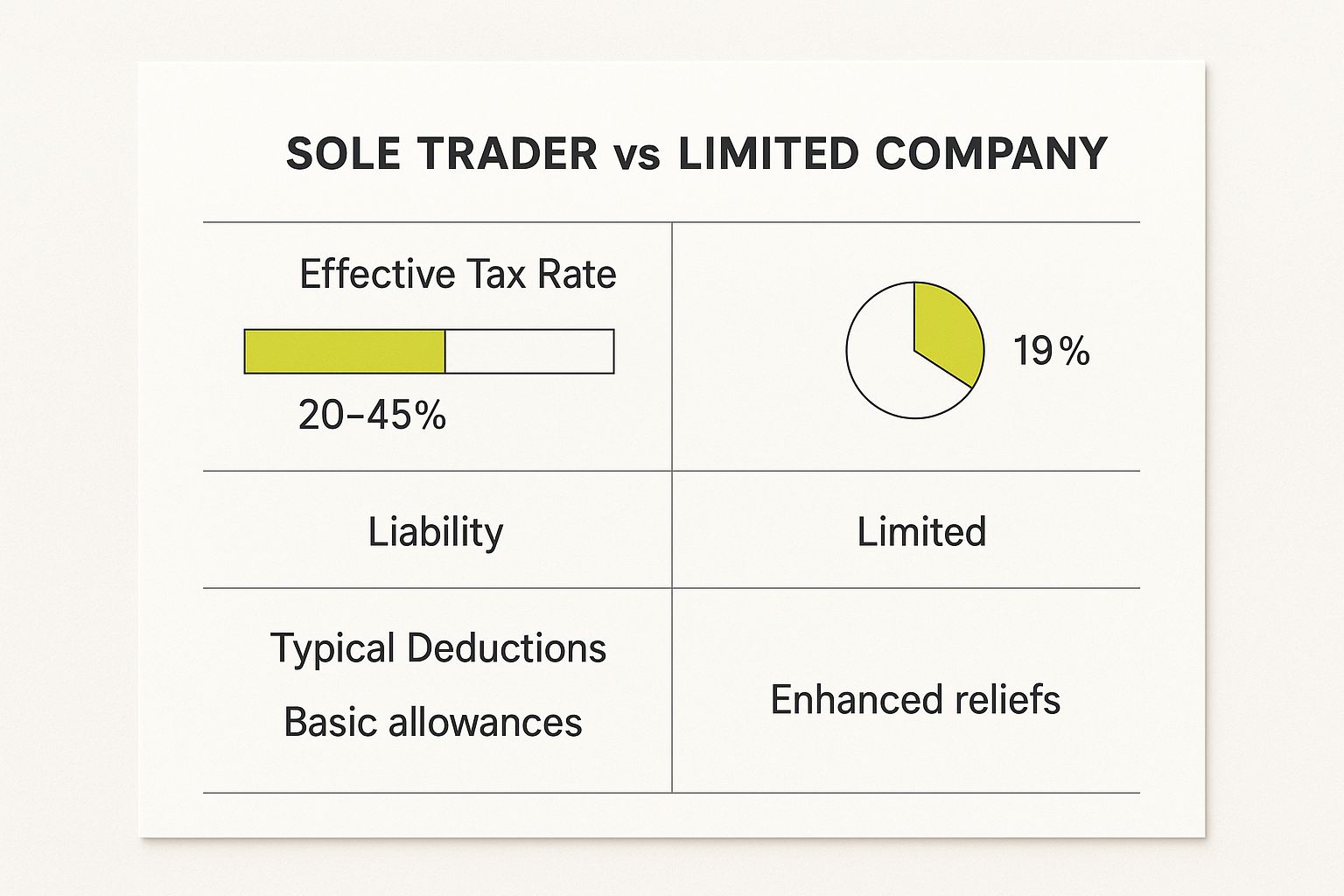

This infographic gives you a quick visual on how tax, liability, and deductions stack up differently between a sole trader and a limited company.

As you can see, the limited company structure often comes out ahead with a lower effective tax rate and access to a much broader range of reliefs.

Right, let’s get past the basics. Have you really thought about every cost linked to your operations? More often than not, the most valuable deductions are hiding in plain sight. This is especially true for businesses that have embraced remote or hybrid working.

For instance, directors working from home can absolutely claim a portion of their home utility bills. This isn't just a token gesture; it's a legitimate reflection of your business's operational footprint. It's simply about accurately assigning costs to where the work actually gets done.

Key Takeaway: The aim is to build a complete and honest picture of your company's outgoings. An incomplete expense report means an inflated profit figure, which directly leads to a higher tax bill than you need to pay.

To help you spot more of these opportunities, here's a quick comparison of the expenses people remember versus the ones they often forget.

This table is a practical comparison to help you identify more claim opportunities and reduce your taxable profit.

Spotting these less obvious expenses is the first step. The next is making sure you have the records to back them up.

Think about the day-to-day activities in your business. Every single one has the potential to generate an expense you can claim against your tax bill.

Here are a few that frequently slip through the net:

Getting into the habit of systematically identifying and tracking these costs is vital. By building a solid system for expense management, you ensure that final profit figure is as low—and as tax-efficient—as it can possibly be.

For more guidance specifically for smaller operations, you can find some valuable pointers in our article covering tax advice for small businesses. At the end of the day, diligent record-keeping is the bedrock of any successful tax reduction strategy.

Investing in your company’s future isn’t just about growth; it’s a brilliant way to manage your tax liability right now. Capital allowances are HMRC’s way of letting you write off the cost of certain assets against your taxable profits.

Essentially, you get tax relief for essential investments. It’s a core tactic for any business owner looking to minimise their corporation tax bill, as it often provides an immediate reduction in tax for the year you make the purchase.

The most common way businesses put capital allowances to work is when buying plant and machinery. This sounds industrial, but it’s a surprisingly broad category that covers everything from office furniture and computers to heavy equipment and commercial vehicles.

Let’s take a real-world example. A logistics firm decides to upgrade its fleet by purchasing three new delivery vans for £90,000. Under a scheme like Full Expensing, the company can potentially deduct the entire £90,000 from its profits in that same year. This directly shrinks the amount of profit subject to corporation tax, giving them a substantial and immediate cash flow boost.

This isn't just about delaying tax; it's a direct cut to your current tax bill. That frees up capital you can reinvest straight back into the business for more growth or to build a stronger financial cushion.

Before 2023, the Annual Investment Allowance (AIA) was the main tool for this, allowing a deduction up to a certain limit (currently £1 million). While Full Expensing has taken the lead for new main-rate assets, it's crucial to understand all the options, especially for more complex investments. Getting to grips with the specifics ensures you claim every penny you’re entitled to when preparing your annual tax returns.

Capital allowances aren't just for the tangible assets you can touch and see. HMRC also offers incredibly valuable tax reliefs designed to reward innovation through Research and Development (R&D) tax credits. These are often misunderstood and, frankly, tragically underclaimed by eligible businesses.

You don’t need to be a pharmaceutical giant in a high-tech lab to qualify. R&D happens in all sorts of sectors.

The key is that you have to be attempting to make an advance in science or technology. The best part? The project doesn't even need to be successful to qualify for the relief.

For a profitable small or medium-sized enterprise (SME), R&D tax relief works by allowing you to deduct an extra percentage of your qualifying costs from your yearly profit, on top of the standard 100% deduction. This creates a total deduction that is significantly larger than what you actually spent.

For instance, if your company spent £50,000 on qualifying R&D, you might be able to deduct as much as £86,000 from your taxable profits. This enhanced deduction takes a serious chunk out of your corporation tax bill.

For companies that are currently loss-making, the scheme is even more powerful. You can choose to claim a cash credit back from HMRC, providing a vital injection of funding right when you need it most.

For any UK company that’s genuinely innovating, the Patent Box regime is more than just a nice-to-have tax break. It’s a seriously powerful tool for slashing your corporation tax bill. The whole point of the scheme is to encourage businesses to develop, keep, and profit from their patented inventions right here in the UK.

If your company has qualifying patents and is making money from them, you can apply a much, much lower 10% corporation tax rate to those profits. This isn't a small tweak; it's a fundamental change to your tax position. When you compare this to the main corporation tax rate of 25% (for companies with profits over £250,000), you can see just how significant the saving is. You can get a better sense of the numbers by looking at the standard UK corporate tax rates.

A lot of people think the Patent Box is only for royalty payments you get from licensing out your patent. While that’s certainly part of it, the scheme is actually much broader, which is where the real value lies for most businesses.

You can also apply the lower rate to profits from:

This wider definition is fantastic. It means a company with just one unique, patented component in its main product can apply the 10% rate to the relevant part of its sales profit, not just a small side-stream of licensing income.

My Take: The trick here is to be proactive with your intellectual property. Stop seeing patents as just a legal shield. Start treating them like active financial assets that can directly and substantially cut your corporation tax bill for years.

Let’s imagine a UK med-tech startup. They've developed and patented a new type of sensor that goes into a medical monitoring device they build and sell.

In one year, they make a profit of £500,000 from selling the device. Normally, this would land them with a corporation tax bill of £125,000 (25% of £500k).

But they’re smart. They elect to use the Patent Box. After doing the calculations, they determine that £300,000 of their total profit can be directly attributed to their patented sensor.

Here’s how the tax breaks down:

Their new total tax bill is £80,000. That’s a straight-up saving of £45,000 compared to the £125,000 they would have paid. That’s a huge amount of cash they can now pump back into R&D, hiring new people, or expanding into new markets.

How you take money out of your business is one of the most powerful levers you have for managing your corporation tax bill. Structuring director pay isn’t just some admin task you tick off a list; it’s a core part of your tax planning strategy.

Getting the mix of salary, dividends, and pension contributions right can make a huge difference to what you owe HMRC at the year-end.

The first thing to get your head around is how the taxman treats each of these. Director salaries and employer pension contributions are both considered allowable business expenses. This is key. It means they’re deducted from your company’s revenue before profit is calculated, which directly shrinks the pot of money that’s subject to corporation tax.

Dividends are a different story. They're paid out of post-tax profits, so they don’t help you reduce your corporation tax at all—the company has already paid tax on that money.

For most directors running a small limited company, the smartest move isn't to take a massive salary. The common strategy is to pay yourself a relatively small, tax-efficient salary that keeps you under certain National Insurance (NI) thresholds.

By taking a salary up to the NI Secondary Threshold, the company pays 0% employer's NI. The brilliant part is that you, the director, still get a qualifying year towards your State Pension. It's a classic win-win: a personal benefit without adding an extra tax cost to the business. Any more cash you need can then be drawn down as dividends, which have the handy benefit of not attracting any NI.

Expert Tip: The optimal salary level changes every single tax year as the government moves the goalposts. It's absolutely vital to review your director payroll annually. A quick check ensures you haven’t accidentally drifted into a higher tax band or are missing out on valuable NI benefits.

While an efficient salary is a great foundation, making employer pension contributions is hands down the most effective way to slash your corporation tax while building your personal wealth.

When your company pays into your pension, that entire contribution is almost always an allowable business expense.

This creates a fantastic double benefit:

Let's look at a quick example. Imagine a company with £60,000 in profit. At a 19% corporation tax rate, that's a £11,400 tax bill.

But what if the director decides to make a £20,000 employer pension contribution instead? The taxable profit immediately drops to £40,000. The corporation tax bill falls to just £7,600. That’s an instant tax saving of £3,800 for the company, and the director now has an extra £20,000 in their pension.

This is worlds more efficient than taking that £20,000 as a dividend, which would have been paid from profits after the original £11,400 tax bill was settled. If you're looking to get the numbers right, you can learn more about how to calculate employer pension contributions in our detailed guide. It's a fundamental part of the toolkit for any director serious about tax efficiency.

When you're running a business, the world of corporation tax can throw up some very specific, practical questions. Getting the right answers is vital for staying compliant and making sure you’re not overpaying HMRC.

Let's dive into some of the most common queries we hear from UK limited company directors.

Yes, you certainly can. If you or your staff regularly work from home, a slice of your household running costs can be put through the business. After all, your home is pulling double duty as an office.

HMRC gives you two ways to handle this:

This is a classic point of confusion, and the short answer is usually no. Costs for entertaining clients, suppliers, or potential customers are not allowable expenses for corporation tax. That business lunch to woo a new client? Unfortunately, you can't use it to lower your taxable profit.

There is, however, one very important exception: entertaining your own employees. Money spent on annual events, like a Christmas party or summer social, is generally an allowable expense. The key rule is that the total cost must not exceed £150 per head for the year. It's a fantastic way to boost team morale that also happens to be tax-efficient.

This is the one that catches so many business owners out. Your deadline to pay your corporation tax is 9 months and 1 day after your company's accounting period ends.

Be careful not to mix this up with your filing deadline. You have a full 12 months from your year-end to file your Company Tax Return (the CT600 form), but HMRC wants the money three months sooner.

Miss that payment date and HMRC will start charging interest, so it's a date for the diary you really can't ignore. Getting these fundamental deadlines right is half the battle, and it's a topic we cover in more detail in our simple guide on UK tax advice for small businesses.

Understanding these details is the key to keeping your tax affairs tidy and your finances healthy. If you're looking for an expert to make sure you're claiming every allowance and taking advantage of every relief, GenTax Accountants can help. We provide clear, proactive advice designed to help your business grow. Visit us at https://www.gentax.uk to see how we can support you.