So, when is the right time to jump from being a sole trader to a limited company? It's a question I hear all the time, and while there's no single magic number, there are definitely key milestones that signal it's time for a serious look.

That moment when 'my little side-hustle' starts feeling like 'the business' is a real turning point. Most of us start out as sole traders – it's simple, quick, and gets the job done. But clinging to that structure for too long can hold you back. Recognising the triggers to incorporate is crucial for protecting yourself and setting up for real growth.

Often, it's not just about the tax savings. You might land a huge corporate client who has a strict policy of only working with limited companies. It’s a risk thing for them. Or maybe your own business is taking on bigger projects or even a bit of debt, and the thought of your house being on the line if things go south is keeping you up at night. That's when limited liability becomes a non-negotiable.

While the majority of small businesses in the UK are sole traders (around 3.2 million, making up 56% of the total), it’s telling that there are over 2 million limited companies. That's a huge number of founders who decided the switch was worth it, often for the credibility and scalability it brings. You can find more insights on UK business structures over at GoSimpleTax.com.

The real signal is when your mindset shifts from running a personal project to building a proper business entity. Incorporating aligns your legal setup with your long-term ambitions, especially if you ever plan to look for investment or sell the business down the line.

Right, let's cut through the jargon. The single biggest change when you move from being a sole trader to running a limited company is that you're creating a separate legal entity. All this means is that your business legally becomes its own ‘person’, entirely distinct from you. This separation is what gives you the crucial benefit of limited liability.

Think of it this way. Imagine your new company takes out a hefty business loan to expand. If things went south and the business couldn't repay it, your personal assets—like your house and savings—are safe. The debt belongs to the company, not to you. For many business owners, that firewall is the main reason to incorporate.

To make this clearer, let's look at the key differences side-by-side.

Here’s a simple table breaking down the core operational, financial, and legal aspects of each structure. It’s a good way to see exactly what changes when you make the switch.

FeatureSole TraderLimited CompanyLegal StatusYou and the business are one and the same.The company is a separate legal entity.LiabilityUnlimited personal liability for business debts.Liability is limited to your investment/shares.TaxationPay Income Tax and National Insurance on profits.Pays Corporation Tax on profits. Directors pay tax on salary/dividends.AdminSimpler accounts, file a Self Assessment tax return.More complex: annual accounts, confirmation statement, Corporation Tax return.OwnershipYou own 100% of the business.Owned by shareholders, managed by directors.CredibilityCan be perceived as smaller or less established.Often seen as more professional and credible.

As you can see, a limited company introduces more formal responsibilities, but it also provides significant protection and potential tax advantages.

Your finances will operate in a completely different way. As a sole trader, you're used to paying Income Tax on all your profits. A limited company, on the other hand, pays Corporation Tax on its profits first. Getting your head around what Corporation Tax is and its current rates is a must-do before you make any decisions.

After the company has paid its tax, you then pay yourself. This is usually done through a tax-efficient blend of:

For many, this two-pronged approach works out to be much more tax-efficient once profits hit a certain level.

The move towards incorporation isn't just anecdotal. Between 2010 and 2023, the number of registered limited companies in the UK shot up by 62%. In contrast, sole proprietorships only grew by 14%. You can dig into the full stats on the GOV.UK business population estimates page.

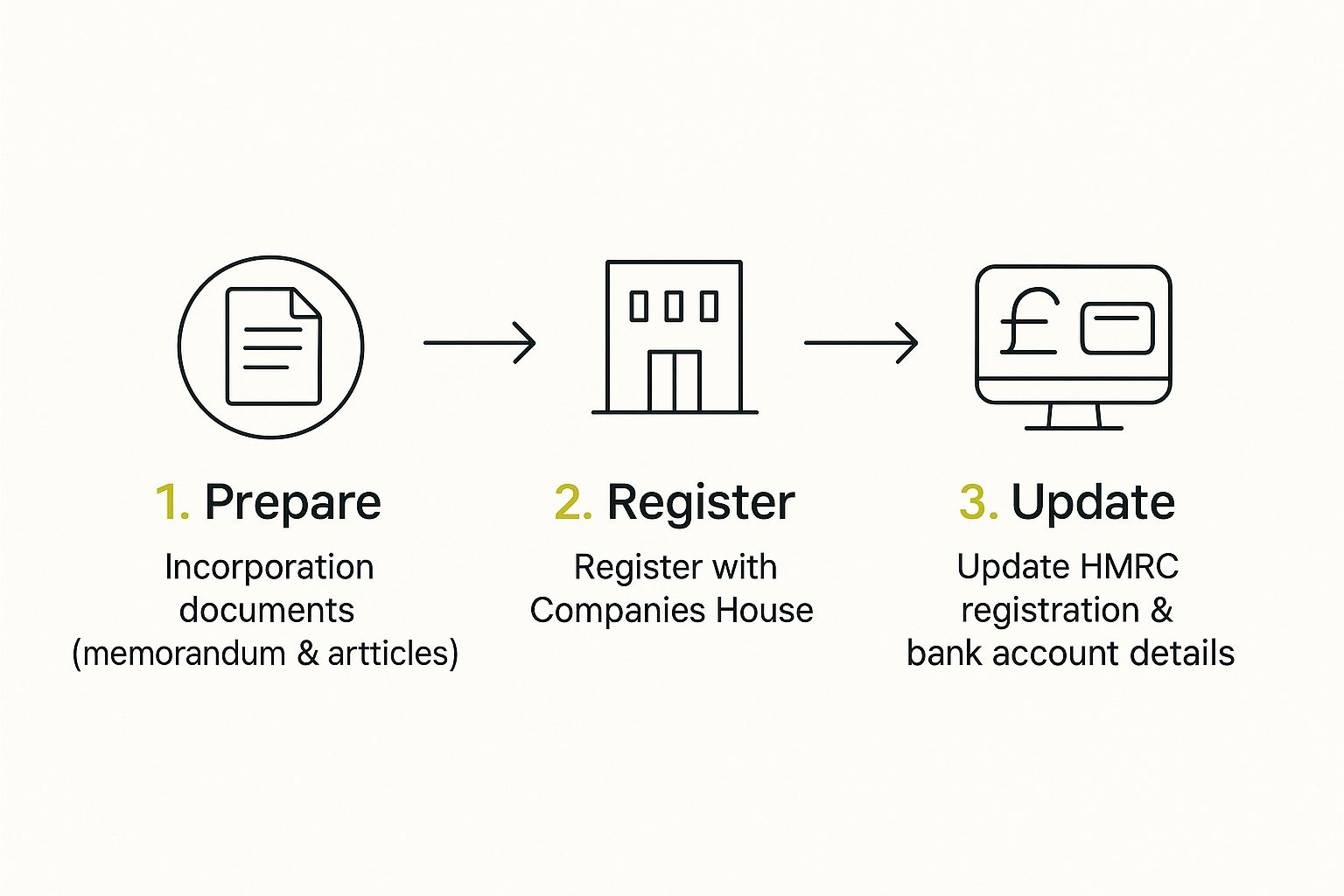

Right, so you’re ready to make the switch? Going from a sole trader to a limited company involves a bit of official paperwork, but honestly, it’s more straightforward than you might think. Let's walk through what you actually need to do, without the usual headache.

First things first, you need a unique company name. It absolutely must be different from any other name already on the Companies House register, and you can't use certain sensitive words without getting permission first. A quick search on the GOV.UK website will tell you if your brilliant idea for a name is free to take.

Once you've bagged a name, you need to appoint your company officers. This just means officially naming at least one director (the person who manages the company) and at least one shareholder (the person who owns it). For most people making this change, you will be both the sole director and the sole shareholder, which keeps things simple.

You'll also need to identify any 'persons with significant control' (PSCs). Again, if you own more than 25% of the shares or voting rights, this is going to be you.

Finally, you’ll need to put your governing documents in place. The main one is the articles of association, which basically sets out the rulebook for running your company. Don't panic – for most small businesses, the default template provided during registration is perfectly fine.

With all your details gathered, the cheapest and most direct way to get registered is via the GOV.UK website. The government's online portal is designed to guide you through each stage, making a DIY registration completely achievable for most business owners.

If you want to dive deeper into what this will set you back, take a look at our complete guide on company registration fees in the UK.

A quick word of advice: you can use a formation agent or ask your accountant to handle this for you. Yes, it costs a bit more, but it also buys you peace of mind. They deal with all the admin, which is a massive plus if you’d rather just focus on running your business.

Right, so you’re officially registered with Companies House. What’s next? Your first port of call is to get the company’s finances set up on the right foot. This isn’t just about being organised; it's a legal must-have.

Your new limited company is its own legal entity, completely separate from you personally. That means its money has to be kept entirely separate from your own.

This is non-negotiable: you absolutely must open a dedicated business bank account in the company's name. You can't just carry on using your old sole trader account or, even worse, a personal one. This separation is the cornerstone of limited liability. If you start mixing funds, you blur those lines and could put your own assets at risk if the business runs into trouble.

For a full step-by-step, check out our guide on how to set up a business bank account.

With the bank account sorted, you’ll need to formally transfer any business assets from your sole trader setup over to the new company. This isn't as complicated as it sounds and could include things like:

Typically, you'll "sell" these assets to the company. This can be in exchange for shares or simply logged as a director's loan that the company owes you.

The final, crucial piece of the puzzle is tying up loose ends with HMRC. You have to tell them you’ve stopped trading as a sole trader, which you’ll do on your final Self Assessment tax return. At the same time, you need to register your new limited company for Corporation Tax within three months of starting to trade. Getting this right from day one is key to a smooth and compliant financial transition.

Welcome to life as a company director. Things are about to get a bit more formal, but don't let that put you off. Getting your head around your new duties from the very start is the key to avoiding penalties and keeping things running smoothly. The extra admin is just part of the deal when you move from sole trader to a limited company.

You're now on the hook for a few key annual filings with both Companies House and HMRC. These aren't optional extras; they're legal requirements you have to meet.

Paying yourself is different now, too. Gone are the days of just taking 'drawings' from the business bank account. You'll likely move to a much more tax-savvy blend of a small salary (run through a proper PAYE payroll) and taking dividends from your company's post-tax profits. For a deeper dive, check out our essential guide on tax advice for small businesses.

So, when does all this extra work actually start to pay off? From what we've seen, the switch really makes financial sense once your annual profits start hitting the £30,000 to £40,000 mark. At this point, the tax savings you can make as a limited company usually start to outweigh the new costs you'll have, like accountant fees. You can explore more on these financial tipping points at Quality Company Formations.

Making the jump from sole trader to a limited company can feel like wading through treacle. It’s perfectly normal to have a few questions buzzing around your head, so let’s clear up some of the most common ones.

First up: the bank account. Do you really need a new one? The answer is a hard yes. This isn't just good practice; it's a legal must-have. Your new company is a completely separate legal entity, and its finances have to be kept totally separate from your personal cash. This is what protects your limited liability, so don't skip it.

What about your beloved business name? You can almost certainly keep it, but you'll need to tack "Limited" or "Ltd" onto the end. The crucial first step is to check that another company hasn't already registered the exact same name at Companies House.

Then there are your existing client contracts. You can't just carry on as normal. You’ll need to let your clients know about the change and formally 'novate' the agreements, which is the legal process for transferring the contract from you (the sole trader) to your new limited company.

Finally, you have to tell HMRC you're closing up shop as a sole trader. You do this on your final Self Assessment tax return by simply stating that your self-employment has ceased. Once you're a director, your responsibilities change, particularly around pay. You can learn more about this with our guide to payroll services for small businesses in the UK.

Finding the financial admin a bit much? GenTax Accountants can take the whole process off your hands. We’ll handle the company formation, tax registrations, and all your ongoing accounting for a simple fixed monthly fee. Get in touch for expert support by visiting https://www.gentax.uk.