Working capital management is all about the strategic juggling act of balancing your company's short-term assets against its short-term debts. The goal? To make sure you always have enough cash on hand to cover your day-to-day operational costs. It’s about giving your business the financial breathing room it needs to pay suppliers, manage stock, and meet payroll without any stressful interruptions.

Think of your business as a living, breathing thing. If cash flow is its lifeblood, then working capital is its ability to take a steady, deep breath. Good management keeps that breathing regular and calm, supplying the oxygen needed not just for survival, but for healthy growth. This isn't just a box-ticking accounting task; it’s the active, strategic control of your company's immediate financial health.

The fundamental idea is to get the timing right between cash coming in and cash going out. You need enough money flowing in from customers to comfortably cover what's flowing out to suppliers, staff, and HMRC. Get this balance wrong, and even a profitable business can suddenly find itself in a serious cash crunch.

Working capital management isn’t about hoarding piles of cash. It’s about making sure your money is always working efficiently, moving through the business to fund operations and spark growth without creating friction or forcing you into costly borrowing.

At its very core, working capital is simply the difference between what you own in the short term (your current assets) and what you owe in the short term (your current liabilities). Getting a firm grip on these two sides is the first step to mastering your cash flow.

Current Assets: These are resources your business owns that you expect to convert into cash within the next year. This includes the obvious, like the cash in your bank account, but also money owed to you by customers (accounts receivable) and the value of the products sitting on your shelves (inventory).

Current Liabilities: These are your financial obligations that are due for payment within the next year. This covers everything from invoices you need to pay your suppliers (accounts payable) and short-term loans to upcoming tax bills and payroll.

Keeping a close eye on these figures is absolutely fundamental to your financial stability. For many businesses, getting professional help to prepare their accounts is the best way to get a clear and accurate picture. This balance sheet tug-of-war directly shapes your ability to operate day-to-day.

To make this crystal clear, let's break down the key components with some real-world examples you’d see in any UK business. This table shows the typical assets and liabilities that determine your working capital position.

Understanding these individual elements and how they interact is the foundation of effective working capital strategy. It allows you to see exactly where your cash is tied up and where your immediate financial pressures are coming from.

Knowing the moving parts of working capital is one thing, but actively managing them is where the real magic happens. This isn't just an accounting chore; it's the engine that keeps your business stable day-to-day and fuels its future growth. It’s the difference between just about keeping your head above water and confidently navigating the market.

Think of it as financial momentum. When your working capital is well-managed, your business has the agility to move forward. You can pay suppliers on time, strengthening those crucial relationships and maybe even bagging some early payment discounts. It also means you’re dodging costly late fees and building a solid credit reputation.

One of the biggest reasons this matters so much is resilience. UK businesses are no strangers to economic curveballs, from surprise interest rate hikes to supply chain chaos. A healthy working capital position acts as a vital financial cushion, giving you the liquidity to ride out these storms without having to scramble for expensive emergency loans.

This proactive approach turns financial management from a reactive headache into a strategic advantage. It’s not just about keeping the lights on; it’s about having the power to invest in new equipment, launch a product, or expand your team when the right opportunity comes along—all without being completely reliant on external finance.

In short, effectively managing your working capital puts you in control. You get to make strategic decisions from a position of strength, rather than being backed into a corner by a cash shortage. That control is fundamental to long-term, sustainable success.

Beyond just stability, optimised working capital is a direct line to funding your growth. Every pound you free up from being stuck in excess stock or tied up with slow-paying customers is a pound you can reinvest straight back into the business. This source of internal funding is often far cheaper and more accessible than a traditional bank loan.

This is a particularly sore point in the UK, which has a long-standing issue with low capital investment holding back productivity. A 2025 report from The Productivity Institute revealed that UK workers had about a third less productive capital per hour worked compared to their peers in the US, Germany, and France. That’s a staggering shortfall of around £2 trillion in 2019. This "capital gap" directly limits a business's ability to run its operations smoothly and, by extension, manage its working capital. You can read the full research on the UK’s capital gap and its economic impact.

By mastering what is working capital management, your business is better equipped to handle these bigger economic pressures and keep its cash flowing efficiently.

Strong working capital management also makes a direct impact on your bottom line. When you get a grip on your cash conversion cycle—the time it takes to turn your investment in inventory back into cash in the bank—you boost your profitability.

Just think about these direct benefits:

Ultimately, these efficiencies all feed into higher profit margins. By understanding your financial performance through clear management accounts and business performance analysis, you can pinpoint exactly where improvements will have the biggest effect. This data-driven approach turns working capital management from guesswork into a precise tool for sharpening your company’s financial health.

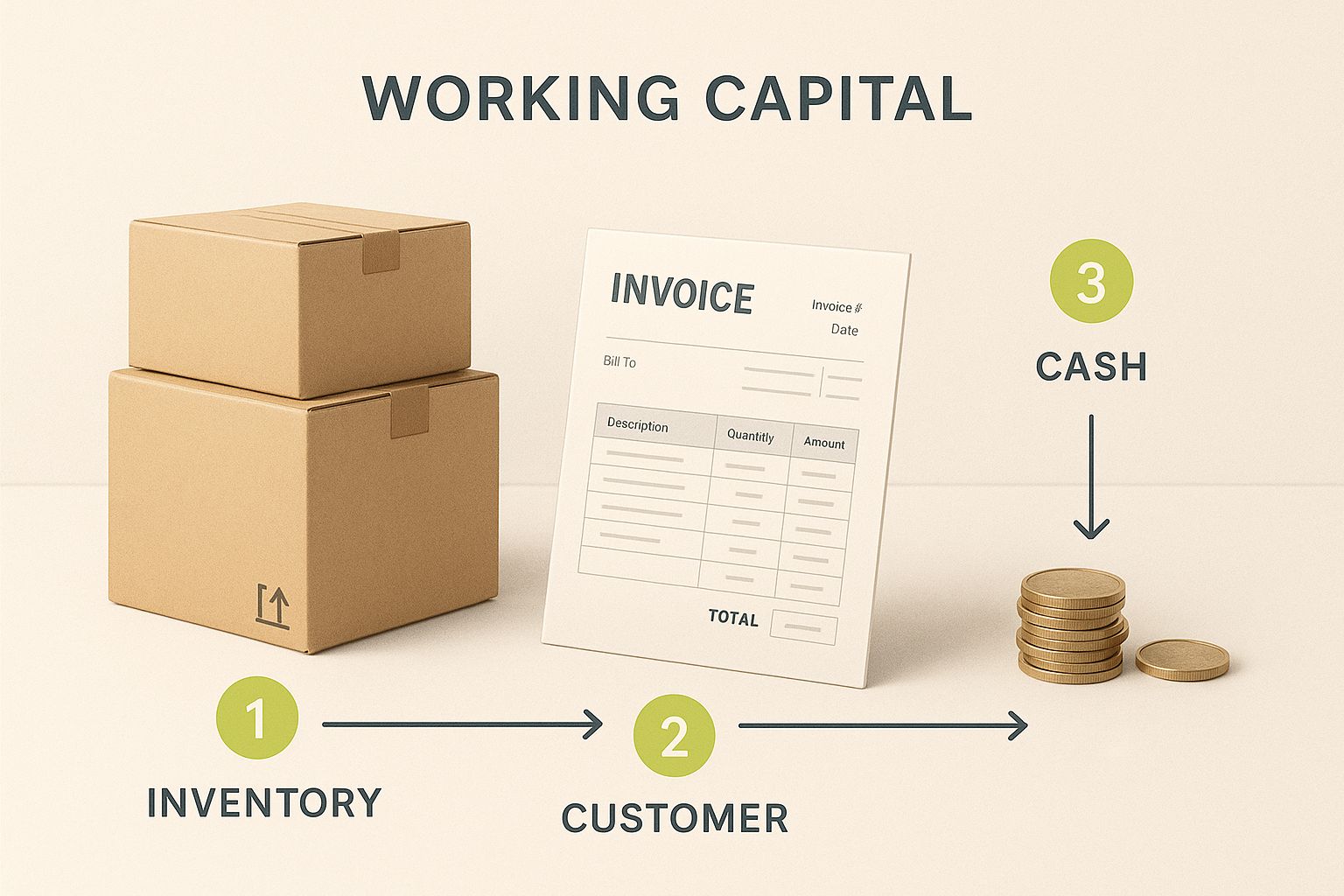

To really get to grips with working capital management, you need to see it as a continuous journey, not just a static calculation on a spreadsheet. This journey is called the working capital cycle, or sometimes the cash conversion cycle. It tracks the complete story of your cash, from the moment it leaves your bank to pay for goods, to the moment it comes flooding back from a customer's payment.

Think of it like a circular train route. Your cash is the train, and its journey has three main stops. The goal is to make this round trip as fast as possible. Why? Because while that train is out on the tracks, the cash is tied up and unavailable for anything else – like paying wages, covering rent, or investing in new equipment.

The entire process shows how your business transforms its operational assets and liabilities back into hard cash. This infographic breaks down the flow between buying stock, making a sale, and getting paid.

As you can see, cash is first locked up in inventory, then it becomes a receivable when you sell something, and finally, it's collected to start the whole cycle over again. A shorter, slicker cycle means your business's financial engine is running smoothly.

The journey begins the second you buy raw materials or finished goods from your suppliers. This creates an accounts payable – basically, a short-term IOU. The strategy here isn’t just about paying bills; it’s all about timing.

Pay your suppliers too early, and your cash leaves the business sooner than it needs to, shortening your own financial runway. But pay them too late, and you risk damaging crucial supplier relationships, causing supply chain nightmares, and getting hit with penalty fees. The real art is in finding that sweet spot.

This is where a key metric comes into play: Days Payable Outstanding (DPO).

DPO measures the average number of days it takes for your company to pay its suppliers. A higher DPO means you are effectively using your suppliers' credit to finance your operations, letting you hold onto your cash for longer. But push it too far, and your reputation could take a hit.

Once you've paid for your goods, they officially become inventory. This is the second stop on the cash journey. While that stock is sitting in your warehouse or on your shelves, it represents cash that is completely tied up and earning nothing.

Good inventory management is a delicate balancing act. Hold too little stock, and you risk missing out on sales and frustrating customers. But hold too much, and you're just locking up capital in products that could become obsolete, expire, or simply go out of fashion, leading to big financial losses.

To keep an eye on this, businesses use Days Inventory Outstanding (DIO). This metric tells you the average number of days your stock sits around before it’s sold. The goal is to keep this number as low as you can without sacrificing sales.

The final stop is turning a sale back into cash. When a customer buys from you on credit, you create an accounts receivable. You've made the sale, which is great, but you don't actually have the money yet. This is often the stage where the working capital cycle can slow to a crawl.

Efficiently managing your receivables is absolutely vital. It means setting clear credit terms, invoicing promptly and accurately, and having a systematic process for chasing up late payments. The faster you collect this cash, the sooner you can put it back to work in your business.

The crucial metric for this stage is Days Sales Outstanding (DSO).

A high DSO, on the other hand, is a red flag that your cash is trapped with your customers for far too long. For any business, maintaining accurate financial records is the first step towards getting these metrics under control. Expert bookkeeping services provide the clear, reliable data needed to calculate and improve your DSO, DPO, and DIO.

The length of this entire journey—your working capital days—has a massive impact on your financial health. Recent trends across Europe, including the UK, show just how much external pressures matter. Post-pandemic disruptions saw sales and payables days spike, while inventory days have remained stubbornly high due to ongoing supply chain issues. As regulations tighten and economic uncertainty grows, UK companies face increasing pressure to shorten their cycles by getting smarter with both collections and supplier negotiations. You can discover more insights about these working capital trends from PwC's European report.

By mastering each stage of this cycle, you can slash the amount of time your cash is tied up, freeing up vital resources to run and grow your business.

Knowing the theory is one thing, but putting it into practice is what really strengthens your business. Moving from theory to action means picking a strategic approach that lines up with your company’s goals, how much risk you’re comfortable with, and your position in the market. There's no one-size-fits-all solution here; the right strategy is entirely down to your specific circumstances.

Generally, businesses fall into one of three camps when it comes to managing their working capital. Each offers a different trade-off between risk and reward, so it’s vital to figure out which one fits your business best.

The first big decision is your overall game plan. Are you going to play it safe and prioritise liquidity, or are you willing to take on more risk for the chance of higher returns? This choice will shape your day-to-day decisions on everything from stock levels to chasing invoices.

There are three main paths you can take:

The Conservative Approach: This is the cautious route. A business using this strategy holds on to high levels of current assets—plenty of cash in the bank and stock on the shelves—and leans more on long-term financing than short-term debt. It's like keeping a well-stocked pantry and a healthy savings account; you’re always ready for a rainy day. This minimises the risk of not being able to pay your bills, but it can dampen profitability because all that extra cash and stock isn't out there earning a return. It's a solid choice for established, stable businesses in predictable industries.

The Aggressive Approach: Think of this as the high-risk, high-reward option. An aggressive strategy means keeping current assets to an absolute minimum and funding your operations with short-term, often cheaper, debt. It’s like running a lean operation with just enough fuel to get to the next petrol station. While this can squeeze every last drop of profit out of your assets, it leaves zero room for error. A minor delay in a customer payment or an unexpected expense could easily spark a serious cash flow crisis. This is often the path taken by fast-growing startups willing to roll the dice for rapid expansion.

The Moderate Approach: This strategy tries to find a happy medium between the two extremes. It’s also known as the ‘maturity matching’ approach because it aims to line up the lifespan of your assets with your financing. Short-term needs are funded with short-term loans, while long-term investments are covered by long-term capital. It’s a sensible, middle-of-the-road method that balances risk and return, making it a popular choice for many small and medium-sized UK businesses.

Once you’ve settled on a broad strategy, you can get down to the nitty-gritty. Implementing specific, practical tactics will directly improve your working capital position by targeting the key cogs in the machine: getting paid faster, managing stock smarter, and timing your payments effectively.

Here are a few proven tactics you can put into action today:

By actively managing these areas, you transform working capital from a passive number on a spreadsheet into a dynamic tool for building financial muscle. The goal is to shorten the cash conversion cycle so that every pound you invest in your operations gets back to you as quickly as possible.

Technology and specialised financial products can be powerful allies in your mission to optimise working capital. For example, the best cloud accounting software for startups gives you a real-time view of your cash flow, automates your invoicing, and makes it far easier to keep on top of who owes you money and who you owe.

On top of that, consider these financing options to unlock trapped cash:

Putting these strategies and tactics into place systematically will help you build a more resilient, agile, and profitable business—one that’s ready to navigate challenges and jump on growth opportunities.

Even with a solid strategy, managing working capital is rarely a smooth ride. Businesses all over the UK run into obstacles that can drain cash and stop growth in its tracks if they're not dealt with swiftly. Spotting these challenges early is the first step toward building a more resilient financial footing.

These hurdles can pop up from inside your business or be thrown at you from the outside world. Internal issues often grow out of everyday operational habits, while external pressures are usually tied to the wider economy. Getting to grips with both is essential.

The most common headaches often start right inside your own four walls. These are the slow leaks that, over time, can put your finances under serious strain. Without a watchful eye, they can easily just become "the way we do things."

Here are the key internal challenges to look out for:

A business can look fantastic on paper – profitable, with strong sales – but still fail if its cash is constantly trapped in unsold stock or unpaid invoices. This is the classic cash flow crunch that smart working capital management is designed to prevent.

Fixing these internal habits takes discipline. It means putting robust tracking systems in place, setting firm credit policies, and making decisions about inventory based on data, not feelings. Even fine-tuning internal processes like payroll can free up valuable time to focus on these core financial pressures.

Looking beyond your direct control, the economic landscape presents its own set of tough challenges. For UK businesses, these external factors have become more and more pronounced, demanding even greater agility in how you manage your money.

Common external pressures include:

Navigating these external storms requires a proactive approach, not a reactive one. A great example of a challenge that often gets missed is covered in this insight on The Quiet Crisis In Working Capital: Low Utilisation. By anticipating these pressures and building buffers into your financial plans, you can shield your business from the worst of the impact and keep your cash flowing.

As you get to grips with working capital, it’s completely normal for specific questions to pop up. This section gives you direct, jargon-free answers to the queries we hear most often from business owners, helping you link the big ideas to your day-to-day operations.

We’ll walk through the practical calculations, clear up some confusing terms, and give you the confidence to manage your working capital like a pro.

The working capital ratio, often called the current ratio, is a quick health check for your business. It answers one critical question: do you have enough short-term assets on hand to cover your short-term debts?

The calculation itself is nice and simple:

Working Capital Ratio = Current Assets / Current Liabilities

Imagine your business has £100,000 in current assets (cash in the bank, stock, and money owed by customers). At the same time, you have £50,000 in current liabilities (supplier bills, short-term loans). Your ratio would be 2:1. For every £1 of debt you owe in the near future, you have £2 of assets ready to cover it.

A healthy working capital ratio is generally seen as being between 1.5:1 and 2:1. This sweet spot shows you can comfortably pay your bills without having too much cash sitting idle in unproductive assets.

A ratio below 1:1 is a major red flag, suggesting you might struggle to meet your obligations. On the other hand, a very high ratio (say, above 3:1) could mean you're not putting your assets to work effectively to grow the business.

This is a really common point of confusion, but the distinction is vital. The easiest way to think about it is that working capital is a snapshot, while cash flow is a movie.

You can have positive working capital and still run into cash flow trouble. For instance, if you have a warehouse full of inventory (an asset) but your customers are taking ages to pay their invoices, your working capital might look healthy on paper. But without the actual cash coming in, you won't be able to pay your staff or suppliers.

Not always, but it almost always warrants a closer look. For most businesses, having negative working capital (where your current liabilities exceed your current assets) points to potential financial distress. It suggests you might not have the funds to cover your upcoming bills.

However, some business models are built to run this way and are incredibly successful.

Think of a big supermarket like Tesco. They sell products to customers and get the cash instantly. But they often pay their suppliers on 30- or 60-day terms. This means they collect cash long before they have to pay it out, allowing them to operate very efficiently with negative working capital. The secret is their super-fast inventory turnover and a constant, predictable stream of cash.

For the vast majority of small to medium-sized UK businesses, though, sustained negative working capital is a serious warning sign that needs immediate attention.

There isn't a one-size-fits-all answer here; it really depends on your industry and how fast things change in your business. But as a general rule, regular reviews are crucial to staying ahead of any problems.

Here’s a practical schedule to consider:

Consistent monitoring is what turns working capital management from a reactive chore into a proactive tool for building a more resilient and successful business.

Managing your working capital effectively is the bedrock of a stable and growing business. At GenTax Accountants, we turn complex financial data into clear, actionable insights, helping you optimise your cash flow and make informed decisions. Discover how our expert accounting services can support your financial success.