Let’s get one thing straight: your break even point is the financial starting line for your business. It's that magic moment when your total sales finally cover your total costs. You're not losing money anymore, but you haven't quite started making a profit either. Every single pound you earn after hitting that point is pure, glorious profit.

Think of it like this. Imagine you run a small coffee van. You’ve got bills to pay every single month, whether you sell one latte or one hundred. Things like your pitch fee (rent), the loan on your coffee machine, and your insurance don't change. These are your fixed costs.

Then you have the costs that only pop up when you actually make a sale – the cup, the coffee beans, the milk. These are your variable costs. They go up and down with your sales volume.

Your break even point is the exact number of coffees you need to sell to cover both your fixed costs for the month and the variable costs of every coffee sold up to that point. Until you sell that many, you're technically in the red.

The second you sell that specific coffee—let's say it's the 500th of the month—you've officially broken even. That 501st coffee? That’s your first taste of actual profit.

Getting a handle on your break even point is essential for any UK business, whether you're a freelance contractor in London or running an eCommerce store from Manchester. It turns guesswork into a concrete, actionable target.

Knowing this number gives you the power to make genuinely informed decisions about where your business is heading. Specifically, it helps you:

At its heart, the break even point gives a clear, simple answer to the most fundamental question in business: "How much do I need to sell just to keep the lights on?" It's the foundation upon which all your profit is built.

Ultimately, this isn't just some boring accounting task; it’s a powerful strategic tool. Once you understand this core concept, you can face financial decisions with far more confidence and build your business on a solid footing for real, sustainable growth.

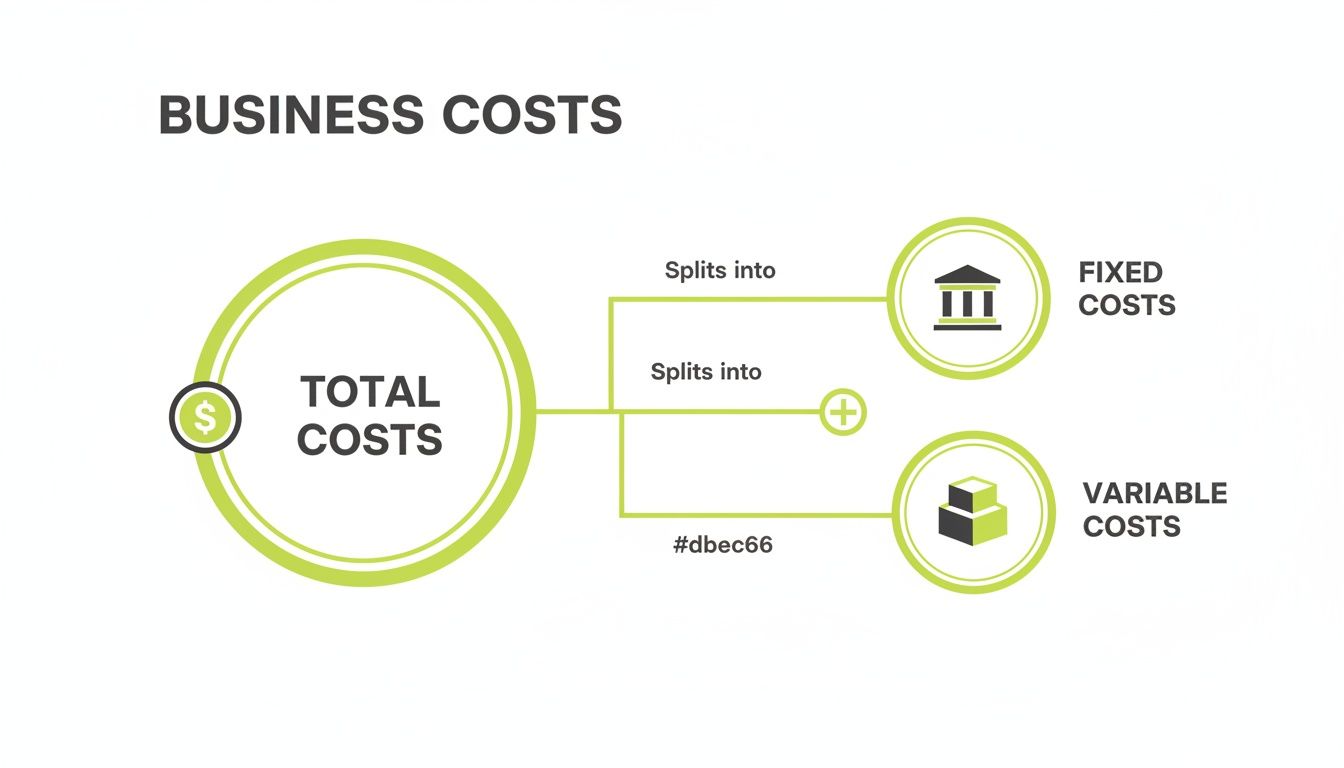

Before you can work out your break-even point, you need to get under the bonnet of your business and see what makes it tick. Financially, every business runs on two types of fuel: fixed costs and variable costs. Getting your head around the difference is the first, most crucial step.

Think of fixed costs as the constant, predictable hum in the background of your operations. These are the bills you have to pay every single month, whether you make one sale or one thousand. They're the financial bedrock of your business.

A freelance graphic designer, for example, has to pay for their software subscriptions and insurance whether they have five clients or none. These are the costs you have to cover just to open your doors, the mountain you climb each month before you even think about profit.

Fixed costs are your non-negotiables. They don't budge, no matter how many products you sell or services you deliver. A simple way to think about it is your monthly mobile phone contract – that base fee is due every month, regardless of how many calls you actually make.

Common examples for UK businesses include:

Getting these numbers down accurately is the first piece of the puzzle. To really get a grip on your finances, it helps to understand a few essential accounting principles.

Now for the other side of the coin. Variable costs are the expenses that rise and fall directly in line with your sales activity. The more you sell, the higher they climb. If sales dip, these costs should drop right alongside them.

Going back to the mobile phone analogy, these are like your extra data charges or international call fees. They only pop up when you use more of the service. For an eCommerce business, the classic example is the cost of goods sold – the more products you ship, the more you spend on the products themselves, packaging, and delivery.

Key Takeaway: Variable costs are directly tied to production or sales. If you have a quiet month with zero sales, your variable costs should ideally also be zero.

These costs are vital because they tell you how much it really costs to make each sale, which directly affects your profitability.

Once you’ve neatly separated your fixed and variable costs, you can uncover a powerful number called the contribution margin. This isn't just stuffy accounting jargon; it’s a concept that shows you exactly how much cash each sale generates to help your business stay afloat.

Put simply, the contribution margin is the revenue left over from a single sale after you’ve subtracted the variable costs tied to that specific sale.

Sale Price – Variable Costs = Contribution Margin

This leftover amount "contributes" towards two things:

Let’s say a contractor charges £500 for a day's work. Their variable costs for that day (materials, travel) come to £100. That means the contribution margin is £400. It's this £400 that helps pay for their fixed costs like insurance and van payments. Understanding this shows you exactly how each job pushes you closer to breaking even.

This is where having clear, organised financial data really pays off. Services like expert management accounts are designed to provide this level of detail. By breaking down your costs this way, you're no longer guessing – you're building a proper roadmap to profitability.

Right, you’ve got a handle on your fixed and variable costs. Now it’s time to put those numbers to work. Calculating your break-even point isn’t nearly as scary as it might sound. We’ve got two straightforward formulas that show you the magic number from two different angles: how many products you need to sell, and how much money you need to make.

This diagram shows how your total business costs are split between the steady, predictable fixed costs and the variable costs that change with your activity.

Getting this split right is the absolute key to using the break-even formulas correctly and making smart financial decisions for your business.

This first formula is perfect if you sell physical products or standardised services. It nails down the exact quantity you have to sell to cover every single one of your costs.

Here’s the formula:

Break-Even Point (Units) = Total Fixed Costs / (Price per Unit – Variable Cost per Unit)

That bit in the brackets, (Price per Unit – Variable Cost per Unit), is what we call your contribution margin per unit. Think of it as the slice of cash from each sale that goes directly towards paying off your fixed costs.

Of course, to get an accurate result, you first need to know how to calculate your cost per unit.

Let’s bring this to life. Imagine a sole trader in Bristol who makes and sells beautiful handcrafted leather wallets.

First up, let's find the contribution margin for each wallet: £50 (Sale Price) - £10 (Variable Costs) = £40.

Now, we just pop that into the main formula:

£1,000 (Fixed Costs) / £40 (Contribution Margin) = 25 units

Our artisan needs to sell exactly 25 wallets every month just to cover their outgoings. Any wallet sold after that 25th one is pure profit. This kind of clarity is invaluable, especially when you’re using tools from our guide on the best cloud accounting software for startups to keep an eye on your sales and costs.

But what if you don't sell "units"? What if you're a digital marketing agency, a consultant, or a contractor with a mix of services at different prices? A unit-based calculation just doesn't work.

In this case, you need to figure out the total sales revenue required to break even. For that, we use something called the contribution margin ratio. This little number tells you what percentage of every pound you earn is actually available to cover your fixed costs.

The formula looks like this:

Break-Even Point (Sales in £) = Total Fixed Costs / Contribution Margin Ratio

And you calculate the contribution margin ratio like this: (Total Sales – Total Variable Costs) / Total Sales.

Let's take a freelance contractor who offers various day-rate services.

First, let’s work out their contribution margin ratio:

(£8,000 - £1,600) / £8,000 = £6,400 / £8,000 = 0.8 or 80%

This tells us that for every single pound this contractor earns, 80p goes directly towards paying off those fixed costs.

Now for the final step:

£2,000 (Fixed Costs) / 0.80 (Contribution Margin Ratio) = £2,500

There it is. The contractor must generate £2,500 in revenue this month to break even. Every pound earned after that is profit. It’s that simple.

The theory is one thing, but seeing your break-even point in action is where it really clicks. It’s time to take those formulas off the page and apply them to four everyday UK business scenarios.

These examples are designed to show you exactly how the calculation works, step by step. We'll use realistic figures to walk through identifying costs, finding the contribution margin, and figuring out what that final break-even number actually means for making smarter business decisions.

Let’s start with Sophie, a freelance graphic designer based in Manchester. Her goal is simple: find out how many design projects she has to land each month just to cover her costs. This is a classic "break-even in units" calculation, where one project is one "unit".

First, Sophie tots up her monthly fixed costs:

Sophie's Total Fixed Costs come to £250 per month. This is the figure she has to cover, no matter how many projects she works on.

Next, she works out her variable costs. These are the expenses tied directly to a single job, like stock images or a specific font licence. She estimates these average out at £20 per project.

Sophie charges a flat fee of £320 per project.

With these figures, we can find her contribution margin for each project:

£320 (Sale Price) - £20 (Variable Cost) = £300 (Contribution Margin)

And now, the final step:

£250 (Fixed Costs) / £300 (Contribution Margin) = 0.83 Projects

Of course, she can't complete 0.83 of a project. This means Sophie needs to win at least one full project every month to break even. Everything after that first project is pure profit.

Now for David, a self-employed IT contractor in Birmingham who works on a day rate. He needs to know the minimum number of days he has to work each month to keep his business afloat.

David’s fixed costs are a bit higher, reflecting his business needs:

His Total Fixed Costs are £650 per month.

David’s variable costs, like fuel and minor materials for a job, average out to about £50 per day. He charges clients a day rate of £450.

Let’s calculate his contribution margin per day:

£450 (Day Rate) - £50 (Variable Cost) = £400 (Contribution Margin)

Plugging this into the formula gives us:

£650 (Fixed Costs) / £400 (Contribution Margin) = 1.625 Days

To be safe, David needs to work at least two full days every single month just to cover his core expenses. Knowing this helps him plan his diary and see the real financial cost of taking a day off.

Here we have a small digital marketing agency in London. They work on monthly retainers and need to know how many clients they need to cover their hefty fixed costs, which include staff salaries.

The agency's monthly fixed costs are significant:

This brings their Total Fixed Costs to a chunky £7,750 per month.

The agency charges an average monthly retainer of £1,500. Their variable costs per client, for things like reporting tools and ad platform fees, come to £250 per month.

So, their contribution margin per client is:

£1,500 (Retainer) - £250 (Variable Costs) = £1,250 (Contribution Margin)

Let’s find their break-even point:

£7,750 (Fixed Costs) / £1,250 (Contribution Margin) = 6.2 Clients

The agency has to sign and keep at least seven clients on its books each month. That one number becomes a powerful Key Performance Indicator (KPI) for the sales team, giving them a clear, non-negotiable target to aim for.

Finally, let's look at an eCommerce business selling handmade candles from a workshop in Scotland. The owner needs to know how many candles they have to sell monthly to make the business viable.

First, the fixed costs:

The Total Fixed Costs add up to £520 per month.

Each candle sells for £18. The variable costs to produce and ship one candle (the wax, wick, jar, packaging, and postage) total £6. Getting these costs right is vital for any online seller, and our specialists can help you get to grips with the financial side of running a successful eCommerce business.

The contribution margin per candle is:

£18 (Sale Price) - £6 (Variable Costs) = £12 (Contribution Margin)

Now for the final calculation:

£520 (Fixed Costs) / £12 (Contribution Margin) = 43.33 Candles

To cover all costs, the store needs to sell 44 candles a month. This insight helps the owner set achievable sales targets and make smarter calls on how much to spend on advertising. Ignoring this simple maths is a huge risk for any small business.

Knowing your break-even number is just the first step. The real magic happens when you turn this static figure into a dynamic tool to steer your business—transforming it from a simple calculation into your strategic co-pilot for growth.

Once you get your head around the break-even point, you can move beyond just reacting to your finances. Instead, you can start asking proactive, forward-looking questions, testing ideas and understanding their financial impact before you commit. This analysis is a crucial part of smart business planning.

Break-even analysis truly shines when you start playing with the numbers. It lets you model different scenarios and see how small changes can have a huge impact on your journey to profitability. This isn't just theory; it’s a practical way to pressure-test your business strategy.

Think about these common business dilemmas:

Running these 'what-if' scenarios replaces guesswork with data-driven confidence. It's an essential discipline for making sound financial decisions, and it's a core part of what our fractional finance director services help business owners master.

One of the most powerful ways to use break-even analysis is for setting realistic and meaningful sales goals. Instead of plucking an arbitrary revenue figure out of the air, you can tie your targets directly to actual profit.

Imagine your break-even point is 50 sales a month. That's great, but what if you actually want to make a £2,000 profit? Simple. You just add your desired profit to your fixed costs in the formula. This revised calculation will tell you exactly how many sales you need not only to cover your costs but also to hit your specific profit goal.

Break-Even Point + Profit Target = New Sales Goal

This simple adjustment turns a survival metric into a growth metric. It gives your sales team a clear purpose: every single unit sold beyond the break-even point is pure profit.

For limited companies, this kind of financial clarity is vital. In the UK, average fixed costs for SMEs can hit £50,000 annually. With a typical contribution margin of around 40%, a business would need £125,000 in sales just to keep the lights on. A small agency with £8,000 in monthly fixed costs needs to know its break-even point inside out for strategic planning. You can dig into UK business productivity and costs by reviewing the latest insights from the Office for National Statistics.

Your break-even point is your financial sanity check before you make any significant investment. Thinking about moving to a bigger office or buying expensive new equipment? Both decisions will push up your fixed costs, which in turn raises your break-even point.

Before you sign that lease or loan agreement, use the formula to answer the most important question: "How many more sales do we need to make this decision financially viable?" If the answer seems unrealistic or requires a huge leap in sales, it might be a sign to reconsider or look for less costly alternatives. This strategic foresight stops you from taking on financial burdens that your current sales can't support, protecting the long-term health of your business.

Right, so you’ve got the formulas down and you understand what your break-even point means. What now? The next step is to take this number off the page and use it to make real, decisive moves in your business. Think of it less as a calculation and more as a vital health check – one that gives you the clarity to build a genuinely profitable future.

But here’s the catch. The entire analysis, and any decision you base on it, hangs on one critical thing: the quality of your data. The formulas themselves are simple, but their accuracy is only as good as the numbers you plug into them. This is exactly where so many businesses stumble.

The real challenge isn’t the maths; it’s correctly separating your fixed and variable costs from the daily mess of your accounts. One small mistake here can make your break-even point completely meaningless, leading you to make bad calls based on flawed information.

To get any real value out of a break-even analysis, you need clean, organised financial data. It sounds obvious, but this is where precise bookkeeping becomes absolutely essential. Without it, you’re just guessing.

The accuracy of your break-even point is a direct reflection of the quality of your financial records. Clean data leads to clear insights; messy data leads to costly mistakes.

Getting professional support can make all the difference. When you have accurate, up-to-date accounts, every cost is correctly categorised. This gives you the solid foundation you need for this analysis and any other financial planning you do. Our dedicated bookkeeping for UK businesses is designed to give you exactly that level of clarity and control.

To help you put all this into practice, we’ve created a simple tool to get you started. The best way to see the value in these concepts is to apply them to your own figures.

We're offering a simple, downloadable spreadsheet template that walks you through the calculation. It’s a straightforward way to apply the formulas using your own business data, taking that first crucial step towards greater financial awareness. It's your chance to move from theory to practical application and start making smarter decisions today.

Even after you've got the formula down, a few practical questions always pop up when you start applying this to your own business. Let's tackle some of the most common ones to clear up any lingering confusion.

Your break-even point isn't a "set it and forget it" number. Think of it as a living part of your business finances.

You absolutely need to recalculate it whenever a significant financial change happens. This could be a price hike from a supplier that squeezes your margins, the cost of hiring a new team member, or a strategic change to your own pricing.

A good rule of thumb is to review it at least quarterly. This simple habit ensures your sales targets and financial plans are always based on what's happening right now, preventing you from operating on outdated and potentially dangerous assumptions.

This is a classic snag for businesses with a diverse inventory, like an eCommerce store or a retail shop. A simple unit-based calculation just won't cut it if you're selling a mix of items with wildly different prices and profit margins.

In this situation, the break-even point in sales revenue formula is your best friend. By working out your overall contribution margin ratio across all your sales, you can figure out the total revenue you need to hit each month to cover all your costs. It shifts the focus from an impossible mix of individual units to a single, clear revenue target.

It's a common mistake to apply a simple unit-based formula to a multi-product business. This almost always leads to inaccurate targets because it completely ignores the different profit margins of each item you sell.

Yes, absolutely. This tricky situation almost always comes down to one thing: cash flow.

Your break-even analysis tells you the moment you've covered your costs on paper, but it doesn't track the actual cash moving in and out of your bank account. You could be technically profitable but have all your money locked up in unpaid client invoices or sitting on shelves as unsold stock.

A business will fail if it runs out of cash to pay its immediate bills—like rent, supplier invoices, or payroll—even if its break-even chart looks perfectly healthy. Profit is an opinion, but cash is a fact.

Understanding your numbers is the first step to taking full control of your finances. At GenTax Accountants, we help you turn complex data into clear, actionable insights, giving you the confidence to drive your business forward. Find out how we can support your growth at https://www.gentax.uk.