Navigating the High-Income Child Benefit Charge (HICBC) often requires an annual Self Assessment tax return. However, a significant change now allows many to handle this charge directly through their monthly salary via PAYE, eliminating the need for a lump-sum payment and the stress of the January deadline. Our August 2025 update provides a detailed, step-by-step roadmap for making the switch. This guide covers everything from assessing your eligibility to finalising the process with HMRC. We will walk you through the specifics of switching from Self Assessment to PAYE for the High-Income Child Benefit Charge, making your tax affairs simpler. Let's begin the process of streamlining your finances.

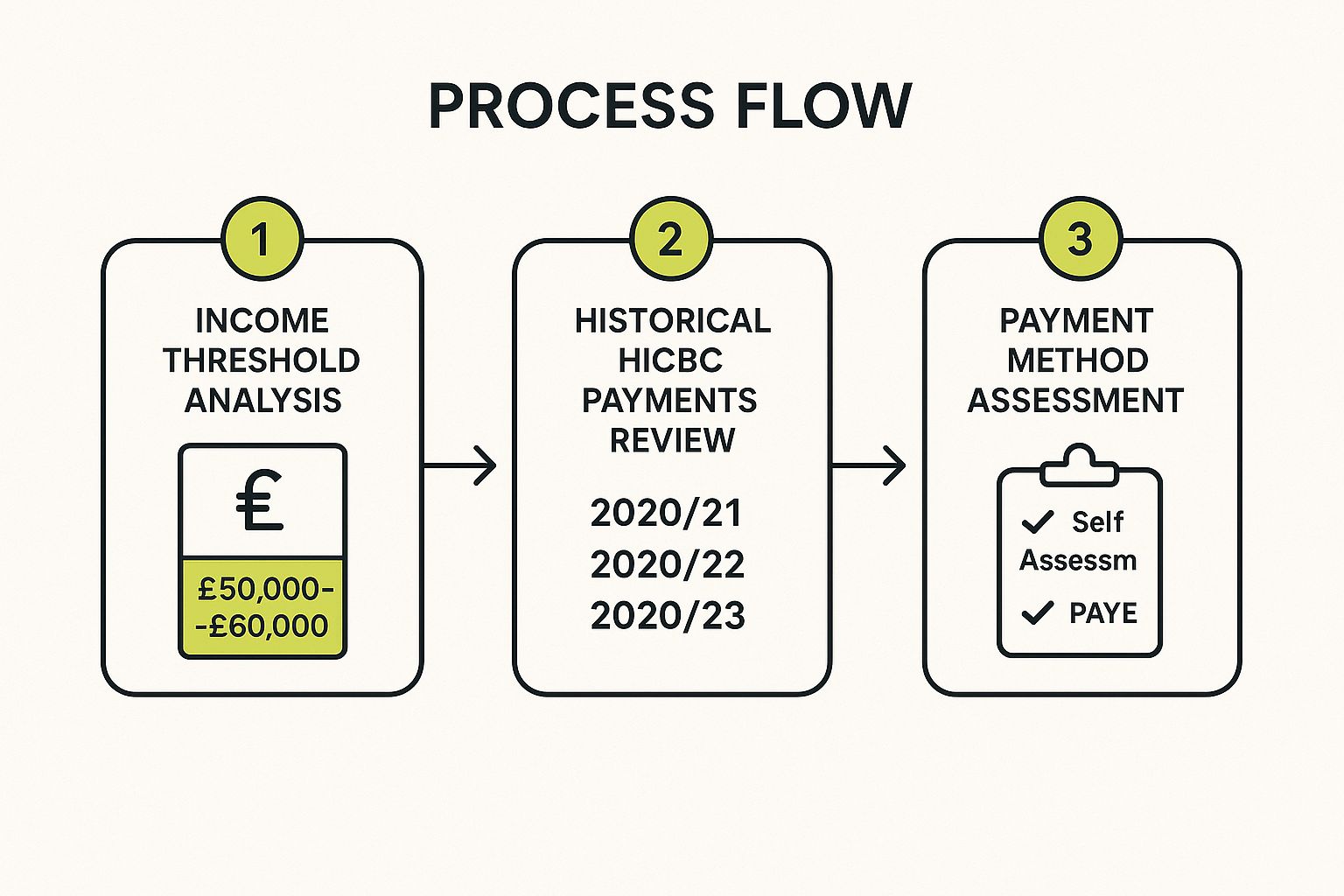

Before making any changes, the first essential step is to conduct a thorough review of your current financial position regarding the High-Income Child Benefit Charge (HICBC). This foundational assessment ensures you understand your historical obligations and can accurately project future liability, confirming that switching from Self Assessment to PAYE for the High-Income Child Benefit Charge is the right move for you. You need to calculate the precise charge you currently owe based on your adjusted net income and review your past Self Assessment tax returns where HICBC was declared.

This analysis helps determine if PAYE collection offers a more streamlined and manageable solution. For instance, if your income fluctuates due to bonuses, assessing past trends will help your employer set an accurate tax code. Gather your P60s, payslips, and tax returns from the last four years. Use HMRC's online calculator to verify past and present HICBC amounts, and document any periods where you opted out of receiving Child Benefit to avoid the charge. For complex situations, you can find expert help with your Self Assessment tax returns.

The infographic below outlines the key stages of this initial assessment process.

Following this process flow ensures you have a clear, data-driven basis for deciding whether to switch from a lump-sum Self Assessment payment to automated PAYE deductions.

Before initiating the switch, it's crucial to confirm that your employment status and primary income source are suitable for collecting the High-Income Child Benefit Charge (HICBC) through PAYE. This step involves ensuring your main income is taxed at source by an employer, which is a prerequisite for HMRC to adjust your tax code. Verifying your eligibility prevents complications and ensures a smooth transition when switching from Self Assessment to PAYE for the High-Income Child Benefit Charge.

This process is most straightforward for individuals with a single employer and a stable salary, such as a manager earning £80,000 annually. It is also suitable for those whose income is consistently above the HICBC threshold through their PAYE earnings alone. Before proceeding, confirm your employer's payroll system can handle tax code adjustments for this specific charge. If you plan to change jobs or your income structure is complex (e.g., significant non-PAYE income), you must carefully consider if this route remains the most appropriate, as PAYE collection is designed for employment-based income.

Verifying your eligibility upfront ensures that the automated PAYE deduction system will work effectively for your specific circumstances.

Once you've confirmed your eligibility, the next critical step is to formally contact HMRC and request the change. This action officially initiates the process of switching from Self Assessment to PAYE for the High-Income Child Benefit Charge, moving the liability from a one-off tax return payment to manageable monthly deductions. You must follow HMRC's designated channels to ensure your request is processed correctly and your tax code is adjusted in a timely manner.

This involves providing HMRC with your National Insurance (NI) number, Unique Taxpayer Reference (UTR), and an estimate of your HICBC liability for the tax year. The most direct method is often to call the HMRC helpline, though using your online personal tax account can provide a digital trail. For example, calling 0300 200 3300 early in the morning can reduce wait times. When you speak to an adviser, clearly state your request, have all reference numbers ready, and ask for confirmation of the change and the effective date.

Taking detailed notes of the conversation, including the adviser's name and any reference numbers given, is crucial. This provides a record should any issues arise later, ensuring a smooth transition and preventing potential communication errors with HMRC.

Once HMRC has processed your request and agreed to collect the HICBC through your tax code, the next critical step is to liaise with your employer's payroll department. This ensures the correct tax code is applied promptly and your deductions begin as planned, solidifying your move away from a large annual Self Assessment bill. You must ensure your employer acts on the new tax code notice issued by HMRC to make switching from Self Assessment to PAYE for the High-Income Child Benefit Charge a seamless reality.

This action bridges the gap between HMRC’s decision and the practical implementation of deductions. For example, if your annual charge is £1,200, you should expect to see a monthly deduction of £100 on your payslip. It is vital to monitor your first payslip after the change to confirm the correct amount is being withheld. Proactively provide your payroll team with a copy of your confirmation from HMRC and ask them to acknowledge receipt of the updated tax code. Keeping clear communication and records is essential for effective payroll management.

Once PAYE is successfully collecting the High-Income Child Benefit Charge, the final step is to formally stop filing Self Assessment tax returns, provided you have no other reason to be in the system. This crucial stage involves notifying HMRC that you no longer meet the criteria for Self Assessment, effectively concluding the process of switching from Self Assessment to PAYE for the High-Income Child Benefit Charge. This action removes the annual legal obligation to file a tax return solely for HICBC purposes, saving you significant time and administrative effort.

To do this, you must complete your final Self Assessment return for the last tax year you were liable (e.g., the 2024-25 return by 31 January 2026). Afterwards, contact HMRC directly by phone or through your online account to request removal from the Self Assessment system. It is vital to confirm with them that no other factors, such as self-employment or rental income, necessitate continued filing. For those navigating complex tax changes, understanding upcoming digital requirements is also beneficial; you can read more about the future of Making Tax Digital for Self Assessment.

The infographic below outlines the key stages of this finalisation process.

Following this process flow ensures a clean break from the Self Assessment system, preventing future penalties for non-filing and completing your transition to a simplified tax-collection method.

Once your employer starts collecting the HICBC through your salary, the process isn't complete. Regular monitoring is crucial to ensure the correct amount is being deducted and to avoid any surprises at the end of the tax year. This ongoing step involves diligently checking your monthly payslips to verify the deductions align with HMRC's calculations and reconciling the annual totals to confirm your liability has been fully met. This proactive approach is a key part of switching from Self Assessment to PAYE for the High-Income Child Benefit Charge.

This continuous oversight helps you identify discrepancies early, such as an over-deduction due to an outdated tax code or a payroll error where the charge was accidentally doubled for a month. To stay organised, it's wise to maintain a simple spreadsheet tracking each month's HICBC deduction against your expected liability. This is particularly important for those whose income fluctuates, as it provides a clear record if adjustments are needed. Efficient record-keeping and regular checks are central to successful payroll management, whether for an individual or a business. You can explore a deeper dive into effective payroll services for small businesses to understand best practices.

The infographic below illustrates the best practices for monitoring your PAYE deductions.

Adopting this monitoring cycle ensures your transition to PAYE is smooth and accurate, preventing future complications with HMRC and giving you peace of mind that your tax affairs are in order.

Once you have successfully transitioned, the final step is to establish a system for an annual review of your PAYE arrangement. This proactive approach ensures your tax code remains accurate and helps you plan for future changes, confirming that switching from Self Assessment to PAYE for the High-Income Child Benefit Charge continues to be the right choice. Life events like a promotion, job change, or having another child can alter your adjusted net income and HICBC liability, requiring adjustments.

This review process helps you stay ahead of potential underpayments or overpayments. For instance, if you anticipate a significant bonus, you can inform HMRC in advance to adjust your tax code, avoiding a surprise bill. Set a yearly calendar reminder, perhaps in April at the start of the new tax year, to assess your income against the HICBC thresholds. For those with fluctuating self-employed income alongside PAYE, you can explore more about managing your tax obligations with expert tax advice for small businesses.

The infographic below illustrates the key considerations for your annual HICBC review.

Following this annual cycle ensures your tax affairs remain compliant and prevents any financial shocks, keeping the PAYE collection method effective for your circumstances.

Transitioning your High-Income Child Benefit Charge from the annual Self Assessment system to monthly PAYE deductions is a proactive step towards simplifying your financial life. This move replaces a single, often substantial, year-end tax bill with smaller, predictable payments, significantly improving your cash flow management and reducing administrative burdens. By meticulously following the steps outlined, from assessing your eligibility and contacting HMRC to updating your employer and ceasing your Self Assessment obligations, you can take firm control of this specific tax liability.

The core benefit lies in automation. Once set up, the process largely manages itself through your employer's payroll, freeing you from the annual cycle of calculations and filing deadlines associated with the HICBC. This strategic shift not only ensures timely payments but also minimises the risk of penalties for late filing or underpayment. Mastering this process is crucial for any high earner seeking greater financial clarity and efficiency. The key is careful planning, clear communication, and diligent monitoring to ensure your tax code is correct and deductions are accurate. Embracing this change allows you to focus less on tax admin and more on what truly matters.

If you're navigating the complexities of switching from self assessment to paye for high-income child benefit charge (august 2025 update), professional guidance can ensure a seamless transition. The expert team at GenTax Accountants specialises in personal tax optimisation and can manage the entire process for you. Contact GenTax Accountants today for a consultation and simplify your tax affairs with confidence.