As your business scales, managing finances transitions from a simple task of balancing books to a complex, strategic necessity. The jump from a lean startup to an established enterprise is often where financial discipline makes or breaks a company. Strong initial sales and a great product are fantastic, but without a solid financial framework, even the most promising ventures can falter. Neglecting this crucial area can lead to cash flow crises, missed opportunities, and stalled growth.

This guide provides eight practical financial management tips for growing businesses in the UK, designed to help you build a resilient foundation for sustainable expansion. We will move beyond generic advice to offer actionable steps and clear examples that you can implement immediately. You will learn how to forecast cash flow accurately, separate your finances effectively, and create detailed budgets that guide your strategic decisions.

From establishing strong credit relationships and implementing professional accounting systems to diversifying revenue and planning for tax obligations, these insights will equip you to navigate the complexities of expansion with confidence. Mastering these principles is not just about avoiding failure; it's about proactively steering your business towards long-term success and stability. Let's dive into the strategies that will secure your financial future.

For a growing UK business, cash is king, queen, and the entire royal court. Simply looking at profit and loss statements isn't enough; you need to understand the timing of money moving in and out of your accounts. Cash flow forecasting is the practice of projecting these movements, giving you a clear picture of your liquidity over a specific period. This foresight is one of the most critical financial management tips for growing businesses, as it helps you anticipate shortfalls and seize opportunities.

During rapid growth, expenses often escalate before revenue fully catches up. A detailed forecast allows you to manage this gap, ensuring you can pay suppliers, staff, and HMRC on time, thus avoiding costly penalties and reputational damage. It transforms financial management from a reactive scramble to a proactive strategy.

Getting started doesn't require complex software. Begin with a simple spreadsheet, tracking expected income and outgoings on a weekly basis. As you grow, you can adopt cloud-based accounting tools like Xero or QuickBooks for more dynamic, real-time insights.

Actionable steps include:

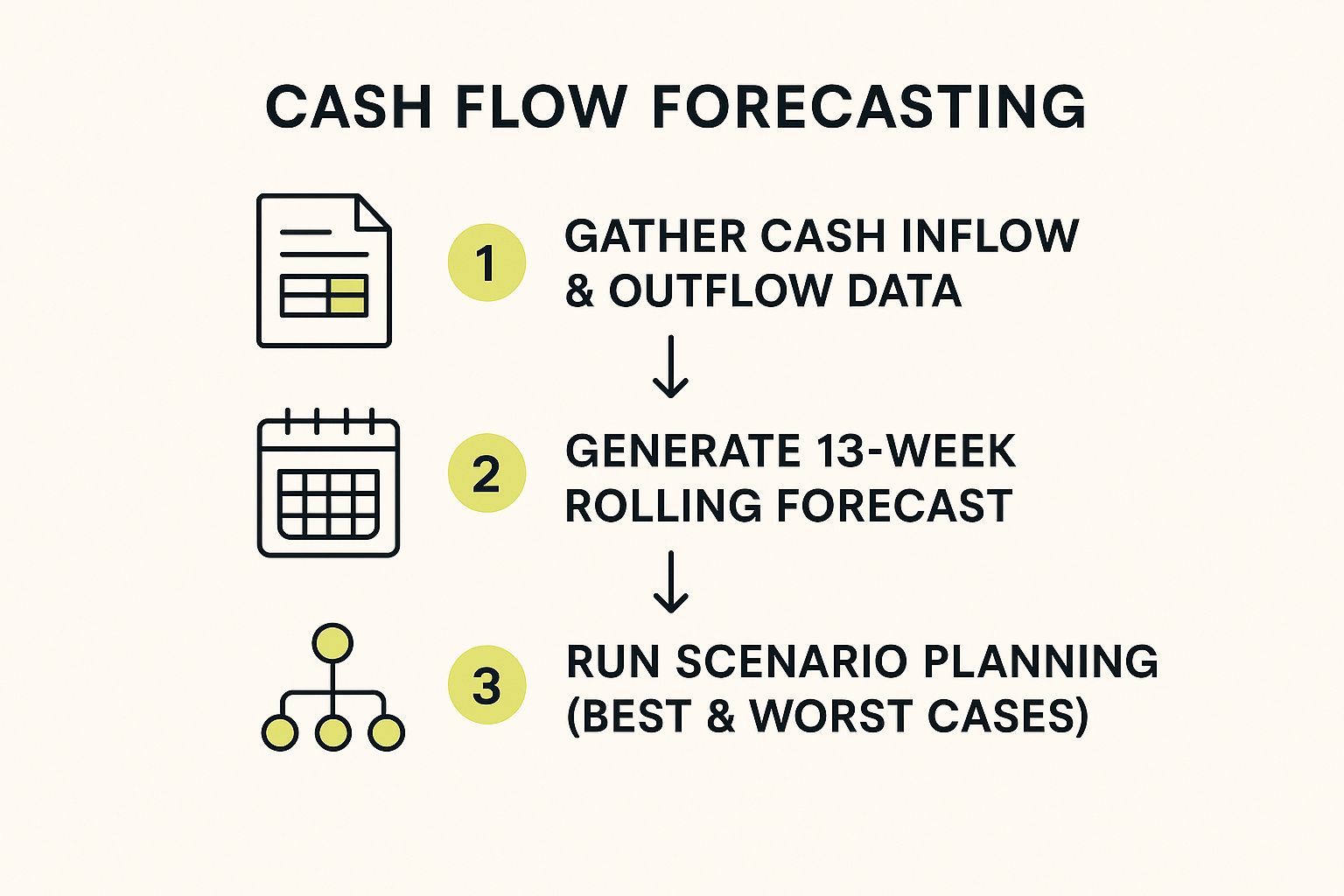

The following infographic illustrates a simple, three-step process for establishing a robust cash flow forecasting system.

This process flow highlights how forecasting moves beyond simple data collection to strategic planning, allowing you to prepare for various business outcomes.

For any growing UK business, from a sole trader to a limited company, commingling personal and business funds is a recipe for administrative chaos and potential legal trouble. The fundamental practice of separating your finances involves maintaining dedicated bank accounts, credit cards, and accounting records exclusively for your business operations. This clear division is non-negotiable for accurate financial reporting, simplified tax compliance with HMRC, and establishing professional credibility.

As your business scales, this separation becomes one of the most vital financial management tips for growing businesses. It provides a transparent view of your company's profitability and financial health, unclouded by personal spending. For limited companies, it's also a legal requirement that protects your personal assets by upholding the corporate veil. Without it, you risk piercing that veil, making you personally liable for business debts. This discipline transforms messy records into a clear, auditable financial system.

Setting up this structure is straightforward and should be one of the first steps you take. Start by opening a dedicated business bank account as soon as your company is formed or begins generating revenue. This initial step sets the foundation for clean bookkeeping and professional financial management from day one.

Actionable steps include:

While cash flow forecasting manages immediate liquidity, a detailed budget acts as your strategic roadmap for growth. For a growing UK business, a budget isn't a restrictive document; it's a powerful tool that translates your ambitions into a financial plan. It outlines expected revenues, costs, and capital expenditures over a set period, typically 12-36 months, providing clear benchmarks to measure your performance against. This structured approach is fundamental among financial management tips for growing businesses.

As your business scales, a comprehensive budget helps you allocate resources effectively, justify investment decisions, and identify potential funding gaps before they become critical. For instance, Peloton's meticulous budget planning was essential for scaling its manufacturing capacity rapidly to meet surging demand. It provides the financial discipline needed to turn rapid growth into sustainable profitability, ensuring every pound is working towards your strategic goals.

Effective budgeting moves beyond a simple annual exercise to become a dynamic part of your financial management. Start by building a detailed model that reflects your unique business drivers, using tools from spreadsheets to dedicated financial planning software. For specialised guidance, engaging a fractional finance director can provide the expert oversight needed to build and manage a robust budget.

Actionable steps include:

For a growing UK business, access to capital is the fuel for expansion. Establishing strong business credit and nurturing good relationships with lenders isn't just a defensive measure; it's a strategic asset. A solid credit profile allows you to secure financing on favourable terms, manage cash flow gaps, and invest in growth opportunities like new equipment or inventory without delay. This proactive approach to credit management is one of the most vital financial management tips for growing businesses, ensuring you have the resources to scale effectively.

When your business is rapidly expanding, unexpected costs and opportunities will arise. Whether it's financing a large order or bridging a seasonal revenue gap, having pre-established credit lines and a positive reputation with lenders means you can access funds quickly. It provides the financial agility needed to outmanoeuvre competitors and capitalise on market shifts, transforming your creditworthiness into a powerful growth engine.

Building excellent business credit is a marathon, not a sprint. It starts with demonstrating financial responsibility consistently over time. You can begin by formally registering your business with credit reference agencies like Experian or Equifax and then focusing on disciplined financial habits. As you grow, diversifying your credit sources builds resilience.

Actionable steps include:

For a growing UK business, relying on spreadsheets and manual bookkeeping is a recipe for error and missed opportunities. As your operations scale, you need a robust accounting infrastructure to provide accurate, timely financial information. Implementing a professional accounting system is about more than just logging transactions; it’s about creating a single source of truth that informs every strategic decision, from pricing and hiring to investment and expansion.

This transition from basic bookkeeping to a sophisticated system is one of the most vital financial management tips for growing businesses. It ensures regulatory compliance with entities like HMRC, builds credibility with investors and lenders, and provides the clarity needed to navigate the complexities of growth. A professional system automates routine tasks, reduces human error, and organises financial data into actionable insights, such as detailed management accounts.

Choosing the right software is the first step. Platforms like QuickBooks, Xero, or NetSuite are designed to scale with your business, offering features that go far beyond simple ledgers. The goal is to move from reactive record-keeping to proactive financial analysis, supported by regular, standardised reporting.

Actionable steps include:

By establishing a rigorous reporting schedule, you can transform raw data into a powerful tool for strategic planning. To learn more about how structured reporting can drive your business forward, you can find further information on management accounts and business performance.

Relying on a single product, service, or customer is a significant risk for a growing business. Diversifying your revenue streams means creating multiple sources of income to build resilience and stability. This strategy, combined with a close analysis of your unit economics, ensures that your growth is not just rapid, but also profitable and sustainable. This approach is one of the most powerful financial management tips for growing businesses as it protects you from market shifts and customer volatility.

Unit economics breaks down your profitability on a per-unit basis, whether that unit is a customer, a product sold, or a subscription. By understanding the revenue and costs associated with each individual unit, you can make informed decisions about pricing, marketing spend, and product development. This granular view ensures that each part of your business is contributing positively to your bottom line, preventing you from scaling an unprofitable model.

The key is to start with your existing strengths. Look for adjacent products or services that you can offer to your current customer base. For example, a web design agency could add SEO services or social media management. As you introduce new streams, meticulously track their performance.

Actionable steps include:

This dual focus on expanding your income sources while ensuring each one is profitable provides a robust framework for long-term financial health and growth.

For a growing UK business, overlooking tax planning is a costly mistake. As your revenue and complexity increase, so does your tax liability. Proactive tax planning involves strategically organising your finances and operations to legally minimise what you owe to HMRC while ensuring full compliance. This goes far beyond simply filing a return; it’s about making tax-efficient decisions throughout the year.

As your business scales, you'll encounter a more complex tax landscape, including Corporation Tax, VAT, PAYE for employees, and National Insurance contributions. Effective planning, supported by professional advice, is one of the most vital financial management tips for growing businesses. It ensures you don't face unexpected bills that could derail your growth, and it helps you leverage available reliefs, like R&D tax credits, which are particularly valuable for tech startups.

Start by treating tax as a regular, predictable expense rather than a year-end surprise. This requires meticulous record-keeping and a forward-looking approach. Working with a qualified accountant or tax advisor transforms this from a compliance headache into a strategic advantage, helping you structure your business for optimal efficiency.

Actionable steps include:

For a growing UK business, momentum can feel unstoppable, but unforeseen challenges can strike without warning. Building an emergency fund and actively managing financial risk is not about pessimism; it's about creating a financial safety net that allows your business to withstand shocks and maintain its growth trajectory. This involves setting aside liquid cash reserves to cover several months of operating expenses, providing a crucial buffer against unexpected downturns, supply chain disruptions, or market volatility.

This proactive stance on risk is one of the most vital financial management tips for growing businesses, transforming vulnerability into resilience. Without adequate reserves, a single unforeseen event, such as the loss of a major client or a sudden economic shift, could derail your progress. A well-managed emergency fund ensures you have the resources to navigate crises without taking on high-interest debt or making desperate, short-sighted decisions.

Building a robust financial cushion starts with disciplined saving and strategic planning. The goal is to create a fund that is both substantial enough to be meaningful and accessible enough for a genuine emergency. This should be coupled with a broader risk management strategy that identifies and mitigates potential threats before they escalate.

Actionable steps include:

Navigating the financial landscape of a growing business is a continuous journey, not a final destination. The tips we have explored, from implementing rigorous cash flow forecasting to strategically building an emergency fund, are the essential building blocks of a resilient and scalable enterprise. Each principle, whether it's the disciplined separation of personal and business finances or the strategic diversification of revenue streams, contributes to a stronger financial foundation.

Mastering these concepts is about more than just keeping the books tidy. It is about transforming financial management from a reactive chore into a proactive, strategic advantage. When you understand your numbers inside and out, you gain the clarity and confidence to make bolder decisions, seize opportunities, and navigate economic uncertainty with greater agility. These aren't just isolated tasks on a checklist; they are interconnected habits that create a virtuous cycle of financial health and sustainable growth.

The true value of these financial management tips for growing businesses lies in their consistent application. Your next steps are crucial for embedding these practices into your company's DNA. Start by selecting one or two areas that require immediate attention. Is your cash flow unpredictable? Make forecasting your priority. Are you unsure about your tax liabilities? It’s time to engage with a professional.

Here is a practical action plan to get you started:

Embracing these financial disciplines will not only protect your business from common pitfalls but will also empower it to thrive. Strong financial management is the engine that powers innovation, fuels expansion, and ultimately turns your entrepreneurial vision into a lasting triumph. It is the critical differentiator between a business that merely survives and one that is built to last.

Ready to elevate your financial strategy and accelerate your growth? The team at GenTax Accountants specialises in providing tech-driven accounting and tax solutions tailored for ambitious UK businesses. We help you implement the systems and strategies discussed here, giving you the financial clarity you need to focus on scaling. Visit GenTax Accountants to learn how we can become your dedicated financial partner.