Professional bookkeeping services for small businesses are all about turning a pile of raw financial data into clear, actionable insights. They take on the crucial jobs of recording your transactions, managing accounts, and keeping you on the right side of the taxman, which frees you up to focus on growth.

Running a small business often feels like you're captaining a ship in uncharted waters. You have a destination in mind—profitability, success—but how do you actually get there without a map and compass? That’s exactly where professional bookkeeping comes in. It’s so much more than just an admin chore; it’s your business’s financial navigator.

Think of your bookkeeper as the expert cartographer on your crew. They don't just log where you've been. They chart your exact financial position, spot potential storms on the horizon (like a looming cash flow shortage), and help you plot the most efficient course forward. Without that guidance, you're essentially sailing blind, making big decisions based on guesswork rather than solid data.

Accurate financial records are the bedrock of any smart business strategy. When your books are meticulously kept, you get the clarity needed to answer critical questions with real confidence:

This level of insight transforms bookkeeping from a reactive, backward-looking task into a proactive, forward-looking asset. It’s the difference between just about surviving and actively steering your company toward sustainable growth.

The demand for these services is huge. In the UK, small businesses are the backbone of the economy, and more and more are realising the value of expert financial management. With nearly 99% of the UK's 5.5 million private-sector businesses being classed as small, the need for reliable support is immense. In fact, around 37% of UK small businesses have already outsourced their accounting tasks to gain a competitive edge.

Beyond just strategy, professional bookkeeping ensures you stay compliant with UK regulations, like those set by HMRC. This includes handling VAT returns and getting everything ready for tax deadlines—especially important with ongoing shifts like Making Tax Digital. You can learn more about the move to Making Tax Digital for Self Assessment and how it affects your reporting duties.

By entrusting your financial records to an expert, you not only dodge costly penalties but also reclaim your most valuable resource: time. This lets you redirect your energy away from spreadsheets and receipts and back to what you do best—innovating, serving customers, and growing your business.

So, what do bookkeeping services for small businesses really involve? Forget the dry, textbook definitions for a moment. It’s far more useful to think of them as a complete financial health toolkit, with each tool serving a specific, vital purpose in keeping your business strong, compliant, and profitable.

Each component works with the others to paint a crystal-clear picture of where your company stands financially. Let's open this toolkit and have a proper look at the essential tools you'll be putting to work.

Cash flow is the lifeblood of your business; it's what keeps the lights on day-to-day. Two key services act as the engine that keeps your cash moving in the right direction.

First up is Accounts Receivable, which is just a formal way of saying "getting paid". It's the process of managing all the money your customers owe you. A bookkeeper makes sure invoices are sent out on time, tracks who has paid, and chases up any overdue accounts. This isn’t just admin; it's about shortening the time it takes to get cash in the bank.

On the other side of the coin is Accounts Payable. This is all about managing and paying the bills you owe to suppliers. Good management here means paying on time to keep your suppliers happy and avoid late fees, all while making sure you don't pay out too much cash at once and leave yourself short.

Once your cash flow is under control, the next set of tools focuses on dotting the i's and crossing the t's. This is where meticulous attention to detail saves you from headaches and costly mistakes later on.

Bank Reconciliation is a perfect example. Think of it as a financial fact-check. Your bookkeeper will sit down and compare your business records against your bank statements, line by line, making sure every single transaction matches up perfectly.

This seemingly simple process is incredibly powerful. It catches bank errors, spots fraudulent activity, and confirms your financial records are a true reflection of reality. Without it, you're flying blind.

Another non-negotiable tool is handling VAT Returns. If your business is registered for VAT, correctly calculating and submitting these returns to HMRC is a legal must. A bookkeeper manages this whole process, ensuring you claim back every penny you’re entitled to and pay the correct amount, on time, every time.

A professional bookkeeper doesn't just record history; they organise your financial data in a way that provides a clear, reliable foundation for every strategic decision you make.

Finally, managing Payroll is a fundamental service that ensures your team is paid correctly and on schedule – which is absolutely crucial for morale. It’s not just about transferring wages; it involves handling PAYE tax, National Insurance, pensions, and issuing payslips. For a closer look, our guide on payroll services for small businesses in the UK breaks this essential function down even further.

The final tools in your kit are the ones that turn raw numbers into business intelligence. This is where you move beyond simple record-keeping and start using your financial data to make smart moves for the future.

Financial Reporting is the process of summarising all that data into easy-to-digest reports. The two most important ones for any business owner are:

These reports aren't just for your accountant at year-end. They are your primary tools for tracking performance, spotting trends, and making informed decisions to steer your business towards growth.

So, beyond just getting the daily tasks done, what’s the real, measurable benefit of using professional bookkeeping services for small businesses? The answer comes down to your Return on Investment (ROI) – a simple way of figuring out what you get back for what you spend. It’s not just an expense; it’s an investment in your company’s future.

Imagine an artisan baker. She spends 10 hours every week buried in spreadsheets, chasing invoices, and wrestling with receipts. By outsourcing her bookkeeping, she gets those hours back. Now she can use that time to perfect new recipes, experiment with a new sourdough line, or improve her customer service—all activities that directly drive sales. That reclaimed time is a tangible return.

While getting your time back is a massive win, the benefits of professional bookkeeping run much deeper. The ROI you see is multi-layered, hitting everything from your bottom line to your long-term strategy.

It starts with financial accuracy. An expert bookkeeper helps you steer clear of costly errors, late filing penalties from HMRC, and missed tax deductions you might not even know existed. Over a year, these savings alone can easily cover the cost of the service.

But the real gains aren't just financial. Think about the mental load. Handing over the stress of financial compliance to a professional you trust means fewer sleepless nights worrying about tax deadlines or unexpected cash flow gaps. That peace of mind is invaluable, freeing you up to lead your business with a clearer, more focused mind.

Many business owners think they’re saving money by doing their own books, but they often ignore the hidden costs. These are the things that don't appear on a profit and loss statement but can seriously hold a business back.

Just think about these common DIY pitfalls:

Outsourcing isn't an expense; it's a strategic investment in efficiency, accuracy, and growth. It shifts your focus from working in your business to working on your business.

A recent study revealed a worrying gap in financial management among UK businesses. It found that almost two-thirds (62%) of small and medium-sized businesses don't work with a professional accountant or bookkeeper, even though half are worried about collapse due to financial pressures. You can discover more insights from the Dext study about the financial challenges facing SMBs.

Ultimately, the biggest return from outsourced bookkeeping is the ability to make better, data-driven decisions. With accurate, up-to-date financial reports, you get a crystal-clear view of how your business is performing. You can confidently answer questions like, "Which marketing campaign is actually delivering a return?" or "Can we really afford to invest in that new equipment this quarter?"

This kind of clarity is what separates businesses that thrive from those that just survive. Armed with precise data, you can create detailed management accounts for improved business performance, allowing you to set realistic goals and track your progress. To really grasp the impact, it helps to know how to calculate return on investment, a process your bookkeeping partner can help you nail down with accurate figures.

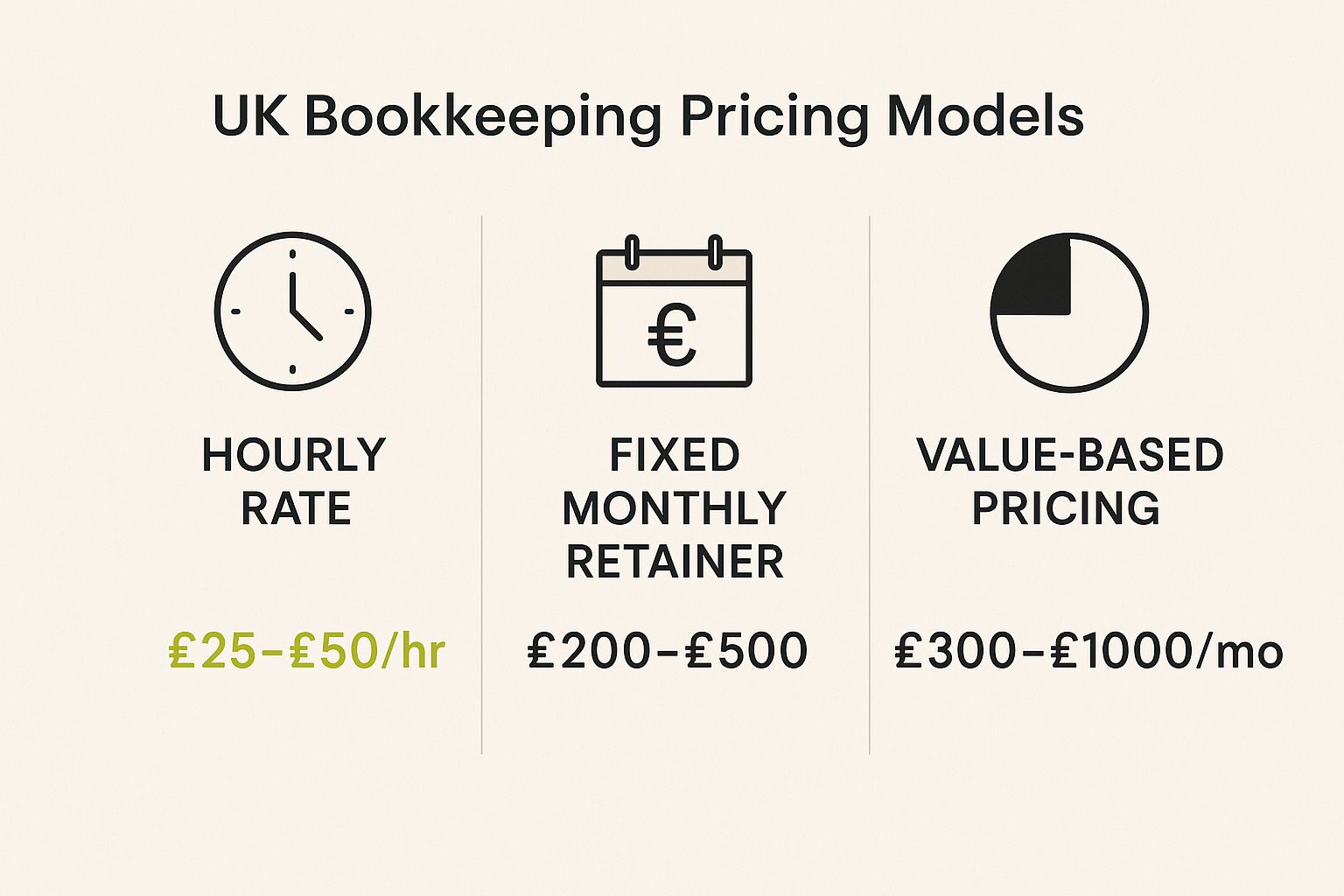

One of the first questions any business owner asks is, "So, how much is this going to cost?" Budgeting for professional bookkeeping isn't just about finding the cheapest quote; it's about understanding the real value you get for your money. Navigating the different pricing models can feel a bit confusing at first, but they generally fall into a few clear categories designed to fit different business needs.

Getting to grips with these structures is the key to finding a service that not only fits your finances but actually helps you grow. Let's break down the most common ways bookkeeping services for small businesses are priced in the UK so you can assess your options with confidence.

The most straightforward model is the simple hourly rate. You just pay for the actual time your bookkeeper spends working on your accounts. This approach is incredibly flexible and often a great starting point for businesses with fairly simple finances.

Think of a new sole trader who just needs a few hours of help each month to get their bank accounts reconciled and prep for a quarterly VAT return. It’s also perfect for one-off projects, like sorting out a year's worth of messy books or getting an extra pair of hands during a particularly busy spell. In the UK, you can expect hourly rates to range from £25 to £50, depending on the bookkeeper's experience and where they're based. The main downside? Costs can become unpredictable if your workload suddenly spikes.

For businesses that need consistency and predictable costs, a fixed monthly retainer is usually the way to go. With this model, you pay a set fee each month for a clearly defined scope of services. This package might cover bank reconciliation, VAT returns, payroll for a small team, and monthly financial reports.

This approach turns your bookkeeping from a variable cost into a predictable operating expense, just like your rent. It also helps build a stronger partnership with your bookkeeper, as they get to know the ins and outs of your business over time. Monthly retainers in the UK typically fall between £200 and £500, depending on your transaction volume and how complex your needs are.

A less common but increasingly popular option is value-based pricing. Here, the fee isn't tied to hours worked but to the actual value and results the bookkeeper delivers. This model moves beyond just ticking off tasks and focuses on strategic input, like finding insights that lead to cost savings or better profitability.

Value-based pricing aligns your bookkeeper's goals directly with your business success. They are compensated for the outcomes they help you achieve, not just the time they spend on tasks.

This is best for established businesses that want a proactive financial partner, not just a record-keeper. Prices are bespoke and can range from £300 to over £1,000 per month, reflecting the direct impact on your bottom line. Getting the most out of this model often means using the right tools, and you can explore some of the best cloud accounting software for startups to see how technology powers this kind of advanced financial management.

The infographic below gives you a clear visual comparison of the pricing models you'll come across.

This visual helps show how pricing scales with the level of service, from simple hourly tasks right through to strategic, value-focused partnerships.

Choosing the right pricing structure is a big decision. This table breaks down the common models to help you figure out which one is the best fit for your business and budget.

Ultimately, the best model depends on where your business is today and where you want it to be tomorrow. Whether you need occasional help or a strategic partner, there's a pricing structure out there that makes sense for you.

Picking the right bookkeeping partner is one of the most important hires you’ll ever make. This isn’t just about finding someone to crunch the numbers; it’s about bringing a key player onto your team who will directly shape your financial health and strategic decisions. A great bookkeeper becomes a trusted advisor, helping you navigate your business journey with real clarity and confidence.

The whole process needs careful thought, and it goes way beyond a simple price comparison. You need a partner who gets your industry, understands your goals, and has the right skills to back your growth. This guide is a straightforward checklist to help you make a smart, informed decision.

Before you even start searching for bookkeeping services for small businesses, you need to look inward. What does your business actually need right now? Having a clear picture of your requirements acts as a filter, helping you instantly spot the right—and wrong—fits.

Are you a sole trader who mainly needs a hand with quarterly VAT returns and your annual Self Assessment? Or are you a growing limited company that needs detailed monthly management reports, payroll for five employees, and proactive cash flow forecasting?

Think about these key areas:

Knowing your specific needs is step one. For example, the support required by a freelance contractor is worlds apart from what a growing eCommerce business needs. Understanding who we help can give you a better idea of how services are matched to different types of businesses.

In the UK, anyone can call themselves a bookkeeper, so it's absolutely vital to check for professional qualifications. Look for credentials from recognised bodies, as they act as a stamp of approval, ensuring the person has met strict standards for competence and ethics.

Key qualifications to look for include:

Beyond qualifications, ask about their experience in your specific industry. A bookkeeper who understands the unique financial challenges of a construction firm or a digital agency will be far more valuable than a generalist. Don’t be afraid to ask for references from current clients with businesses similar to yours.

Modern bookkeeping is all about technology. It’s crucial that your potential partner is skilled with leading cloud accounting software like Xero, QuickBooks, or Sage. Ask them which software they specialise in and why they recommend it. Their answer will tell you a lot about their approach and whether they can help you work more efficiently.

Data security is just as important. After all, you’re trusting this person with your most sensitive financial information.

Ask direct questions about their security protocols: "How do you ensure my financial data is kept secure and confidential?" A professional bookkeeper will have clear, reassuring answers about data encryption, secure client portals, and their compliance with GDPR.

The stakes are high when it comes to financial paperwork. Research shows a staggering 66% of British businesses are at risk due to improper handling of their accounting documents. With nearly half of microbusiness owners worrying about tax return mistakes, finding a reliable, tech-savvy partner is more critical than ever. You can read more about the challenges UK businesses face and why professional support is so important.

Once you've shortlisted a few potential partners, get a list of questions ready for your initial consultation. This meeting is your chance to get a feel for their communication style, expertise, and whether you have a good rapport.

Here are some essential questions to ask:

Choosing the right bookkeeper is about finding a partner who not only has the right technical skills but also understands your vision and is committed to helping you achieve it. Taking the time to follow these steps will ensure you find someone who becomes a true asset to your business.

Modern bookkeeping has moved far beyond dusty paper ledgers and clunky spreadsheets. Today, professional bookkeeping services for small businesses are powered by smart, cloud-based platforms that completely change how you see and manage your finances.

Think of it like swapping an old paper road map for a live GPS. The map shows you where you’ve been, but the GPS gives you a real-time view of your position, upcoming traffic, and the fastest route to your destination. That’s exactly what cloud accounting software like Xero, QuickBooks, and Sage does for your business's financial journey.

The single biggest game-changer with modern bookkeeping tech is access to real-time financial data. Because everything is in the cloud, your financial information is always up-to-date and accessible from anywhere with an internet connection. This means you, your bookkeeper, and your accountant can all look at the same accurate numbers at the same time.

This instant access has a huge impact on your ability to make proactive decisions. No more waiting weeks for month-end reports. You can see your cash flow position today, check which invoices are overdue right now, and plan for upcoming expenses with confidence.

A professional bookkeeper uses these tools not just to record your history, but to give you a live dashboard of your business’s financial performance. This allows you to make faster, better-informed decisions.

This collaborative setup means your financial partner can spot a potential problem and alert you immediately, helping you steer clear of trouble before it escalates. It’s a fundamental shift from reactive record-keeping to proactive financial management.

One of the most practical benefits of this technology is automation. Manual data entry is not only a drain on your time but also a major source of costly human errors. Modern platforms get rid of most of this tedious work.

Here’s a glimpse of how automation can simplify your day-to-day operations:

A big part of getting your financial operations running smoothly is automating data entry processes wherever possible. By letting technology handle these repetitive tasks, your bookkeeper can focus on higher-value work, like analysing your financial performance and providing strategic advice that genuinely helps your business grow. This smart use of tech is what truly defines modern, effective bookkeeping.

When you're looking into professional bookkeeping services for small businesses, a few questions are bound to pop up. That's perfectly normal. Getting straight answers is the only way to feel confident you're making the right move.

Think of this section as a quick-fire Q&A, tackling the most common queries we hear from business owners. We’ll clear up the practical stuff so you know exactly what to expect.

This is easily the most common question we get, and for good reason. While the roles definitely overlap, the main difference comes down to timing. A bookkeeper's job is to capture and organise your day-to-day financial transactions as they happen. They are focused on the present.

An accountant, on the other hand, takes that clean, organised data and puts it to work. They handle the bigger picture stuff like high-level analysis, tax planning, and strategic financial advice. Their focus is on the future.

A simple way to put it: your bookkeeper builds a solid financial foundation brick by brick. Your accountant then uses that foundation to design the rest of the house—your long-term financial strategy and goals.

Most small businesses need a bookkeeper for ongoing accuracy throughout the year and an accountant for year-end reporting and tax strategy. Many modern firms, like ours, bundle these services together for a seamless experience.

Trying to handle the books yourself can seem like a great way to save money, especially when you're just starting out. And honestly, for a very simple business with only a handful of monthly transactions, it might be manageable for a little while.

But as your business grows, so does the financial complexity. The risk of making a mistake that costs you money goes up, and every hour you spend wrestling with spreadsheets is an hour you’re not spending on what you do best—running your business. The tipping point usually arrives sooner than you think. If you find yourself spending more than a few hours a month on it, or feeling that knot of uncertainty around VAT rules, it’s a clear sign you’re ready for professional help.

The right communication rhythm is all about what works for you, but it should always be consistent. As a bare minimum, you should expect a monthly check-in where your bookkeeper runs you through your financial reports and discusses how things are going.

Many business owners actually prefer more frequent contact, like a quick weekly email to clear up any queries. A great provider will be proactive, reaching out whenever they spot something that needs your attention. The key is to agree on a communication plan right from the start, so you always feel connected and in control of your numbers.

Getting set up with a new bookkeeper is usually a pretty painless process. To get the ball rolling, you’ll just need to pull together a few key bits of information.

Don't worry, your new bookkeeper will walk you through exactly what they need, making the whole handover smooth and straightforward.

At GenTax Accountants, we make managing your finances simple and stress-free. Our expert team combines technology and personalised support to handle all your bookkeeping needs, giving you the clarity to focus on what you do best. Ready to get your books in order? Visit GenTax Accountants to learn more.