Bookkeeping services for a small business are essentially the day-to-day work of managing and recording your company's financial transactions. Think of it as having a dedicated financial storyteller on your team—someone who translates every sale, purchase, and payment into a clear, organised narrative that helps you make smarter decisions.

At its core, professional bookkeeping is about the systematic recording of your financial activities. But it’s so much more than just crunching numbers; it’s about creating an accurate financial history you can actually rely on.

Imagine it like a health tracker for your business. It constantly monitors your financial pulse, logging every pound that comes in and every pound that goes out. Without this, you’re basically flying blind, making critical decisions based on guesswork rather than solid data.

A professional bookkeeper’s job is to be that storyteller. They gather all the raw data from your day-to-day operations—invoices, receipts, bank statements, payroll—and weave it into a meaningful story. This story reveals crucial plot points about your business, such as:

By keeping precise records, bookkeepers make sure this story is always accurate and up-to-date. They prepare key financial statements, like the Profit & Loss and Balance Sheet, which are the main chapters of your financial book. This readiness is a lifesaver come tax season, preventing that last-minute scramble and the risk of penalties.

Bookkeeping isn't just about compliance or looking backwards. It's the fundamental language of business, giving you the clarity needed to navigate challenges, jump on opportunities, and build a solid foundation for growth.

This need for financial clarity is especially urgent in the UK, where small businesses are the backbone of the economy. There are 5.5 million private-sector businesses, and around 99% of them are classed as small.

With that in mind, it’s not surprising that 37% of UK small businesses choose to outsource their bookkeeping. Much of this is driven by the headache of tax returns; HMRC data shows nearly half of microbusiness owners worry about making mistakes.

Ultimately, investing in expert bookkeeping services for small business isn’t just about managing the numbers—it's about gaining peace of mind. It’s the difference between hoping your business is healthy and knowing it is. This is often done using modern tools; you can explore our guide on the best cloud accounting software for startups to get a feel for the technology involved.

Let's be blunt: neglecting your business's finances is one of the biggest risks you can take. Picture the sudden panic of an unexpected HMRC inquiry or the sharp sting of a business loan rejection, all because of messy, unreliable financial records. These aren’t just abstract worries; they are the unfortunate reality for many small businesses that don't have a firm grip on their books.

But the rewards for getting it right are just as real. Proper bookkeeping isn't just another admin task to tick off a list. It’s the solid bedrock on which you build every strategic decision. Think of it as your best defence against financial surprises and your blueprint for sustainable growth.

When your books are in order, everything becomes clear. You can see exactly where every pound is going, identify which products or services are actually making you money, and plan for the future with genuine confidence. This financial insight transforms bookkeeping from a chore into one of your most powerful tools for building a resilient, competitive business.

Imagine your financial data is a map. Without accurate bookkeeping, you're navigating in the dark, relying purely on gut feeling. With it, you have a detailed, illuminated guide showing you the safest and fastest route to your goals. That clarity is absolutely crucial for making smart decisions.

For example, your records might reveal that a particular service, while popular, has incredibly low profit margins because of hidden costs you hadn't accounted for. Armed with that knowledge, you can adjust your pricing or tweak your operations to boost profitability. It also gives you a tight grip on cash flow, ensuring you always have the funds to pay suppliers, staff, and yourself on time. This is where tools like management accounts to assess business performance come in, helping turn raw numbers into an actionable strategy.

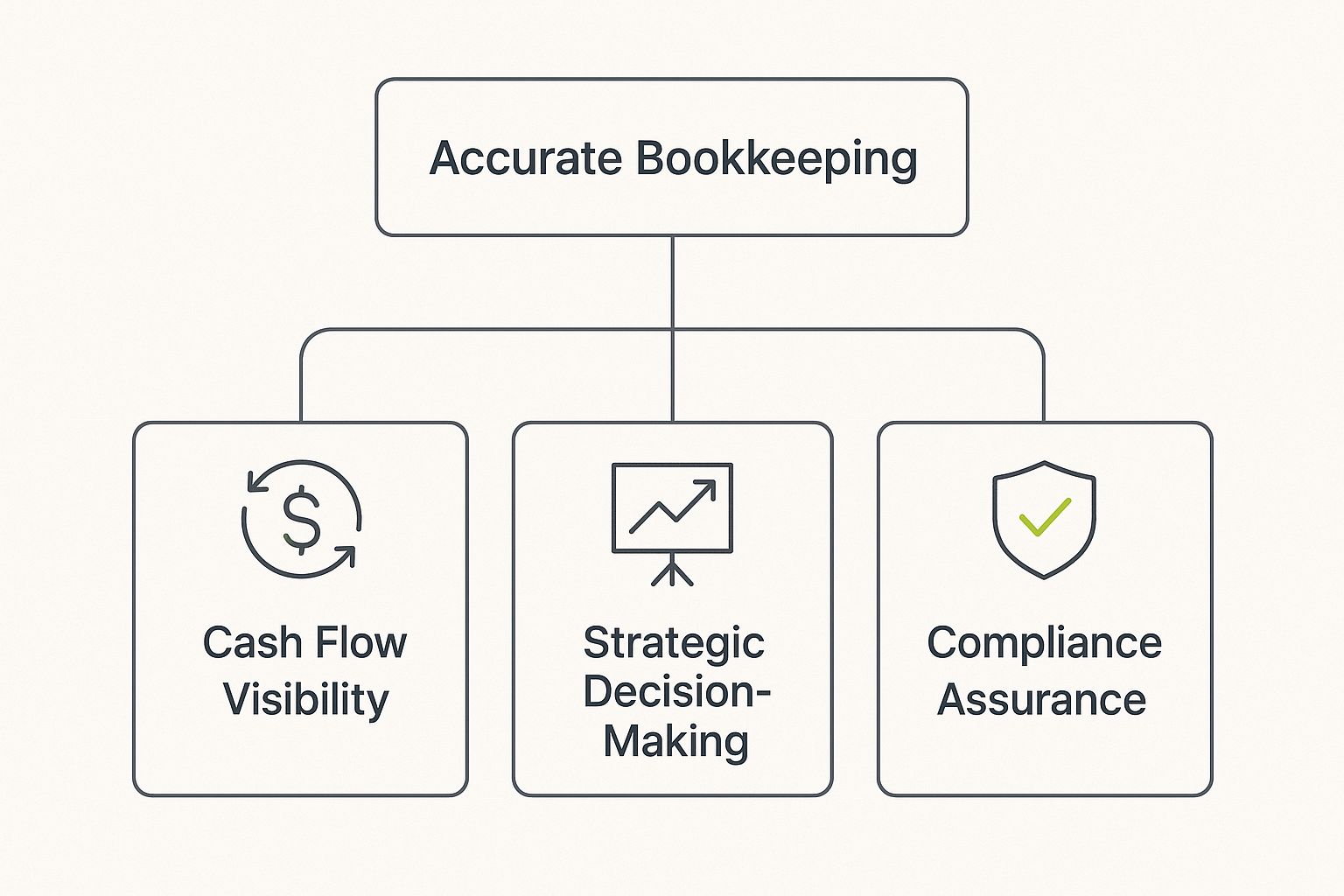

This infographic breaks down the core benefits of maintaining precise financial records.

As the diagram shows, solid bookkeeping directly supports essential business functions, creating a stable foundation for any small business to build upon.

Today's economic climate leaves very little room for error. Recent research paints a stark picture: a staggering 54% of UK small and medium-sized businesses (SMBs) are just one significant cost increase away from potential failure. That statistic really highlights the precarious financial tightrope many businesses are walking.

Despite this vulnerability, a surprising 62% of these SMBs do not work with a professional accountant or bookkeeper to help them navigate these risks. This reveals a critical gap between need and action. You can discover more insights from this small business financial research on dext.com.

This is where professional bookkeeping services for small business become a crucial line of defence. An expert bookkeeper does more than just record transactions; they act as your financial guardian.

They help you:

Having meticulously organised financials is like having a financial safety net. It provides the stability to weather unexpected storms and the credibility to seize growth opportunities when they arise. It’s a genuine investment in your business’s long-term health and survival.

It’s one thing to know the term "bookkeeping services," but it's another thing entirely to know which specific tasks will actually make a difference for your business. This isn't about buying a generic, off-the-shelf package; it’s about picking the precise support that solves your unique financial headaches and helps you grow. Think of it less like a set menu and more like building a custom toolkit for your company's financial health.

The foundation of it all is keeping your transaction records straight, which makes up the largest chunk of the UK's £6.6 billion bookkeeping industry. There's a good reason this sector is growing – solid record-keeping is the fundamental building block for everything else. From this base, a few key services emerge that every small business owner should have on their radar.

To give you a clearer picture, here's a breakdown of the essential bookkeeping services and how they directly impact your business.

These services work together to build a complete and reliable picture of your business's financial health, giving you the control and clarity you need to succeed.

At its core, good bookkeeping is about recording every single transaction—every sale, every purchase, every expense. A professional bookkeeper doesn't just list these; they meticulously organise the data, assigning each item to the correct category.

This simple act transforms a chaotic shoebox of receipts and invoices into a clear, usable financial database. It's the difference between a messy, disorganised storeroom and a perfectly catalogued library where you can find any piece of information in seconds. One huge advantage here is the ability to efficiently track jobs and costs, which gives you a crystal-clear view of what's making you money and what isn't.

Think of this as your financial safety check. Bank reconciliation involves comparing your internal business records against your bank statements, line by line, to make sure they match up perfectly. It might sound a bit tedious, but its value is enormous.

This regular check-up helps you:

Without reconciliation, you're flying blind, relying on a financial picture that could be dangerously out of date.

Put simply, this is about keeping track of who you owe (accounts payable) and who owes you (accounts receivable). Getting a firm grip on these two areas is the absolute lifeblood of your cash flow.

A bookkeeper will track all outstanding invoices, making sure your suppliers are paid on time to keep those relationships strong. Even more critically, they'll chase up customer payments and follow up on overdue invoices so that cash actually lands in your business promptly. This proactive management stops the cash flow gaps that can cripple even a profitable company.

If you have employees, getting payroll right is completely non-negotiable. It’s so much more than just paying salaries; it involves calculating taxes, National Insurance contributions, and pension deductions, then issuing accurate payslips.

An expert bookkeeper makes sure your team is paid correctly and on time, every single time, while keeping you fully compliant with all HMRC regulations. This lifts a huge administrative weight off your shoulders and removes the risk of making costly payroll errors.

For any VAT-registered business, managing Value Added Tax is a critical and often bewildering task. A bookkeeper will track the VAT you've charged on sales and the VAT you've paid on purchases. They then prepare and submit your VAT returns to HMRC accurately and on schedule.

This not only keeps you compliant but also ensures you're reclaiming all the VAT you're entitled to, which can make a real difference to your bottom line. If this is a particular headache, it's worth seeing how specialised VAT return services can take this entire process off your plate.

Finally, all this diligent record-keeping comes together in the form of vital financial reports. These aren't just dry documents for your accountant; they are powerful tools for you, the business owner, to understand what’s going on. The two most important reports are:

These reports translate all that raw data into actionable intelligence, helping you see exactly where your business stands so you can make confident, informed decisions for the future.

Picking the right bookkeeping services for your small business goes way beyond just handing off a task. It's about finding a financial partner who will genuinely get invested in your company’s growth. Think of it like bringing a key player onto your team—you need the right skills, the right experience, and a communication style that just clicks with how you work.

The aim is to find someone proactive, an expert who brings you insights, not just a data entry clerk who quietly logs your transactions. A great bookkeeper becomes a real extension of your business, helping you steer through financial rough patches and spot opportunities you might have missed on your own.

Here in the UK, not all bookkeepers are on the same level. You’ll want to look for professionals with recognised qualifications from bodies like the Association of Accounting Technicians (AAT) or the Institute of Certified Bookkeepers (ICB). These certifications are a solid stamp of approval, showing they meet high technical and professional standards.

But qualifications are just the start. Industry-specific experience can be a game-changer. A bookkeeper who knows the ins and outs of your sector—whether that’s construction, retail, or tech—is going to be far more valuable. They'll already be familiar with the common financial hurdles, typical spending patterns, and the specific VAT rules that apply to you.

That kind of specialised knowledge means they can give you much sharper advice and make sure your books are not only accurate but truly optimised for your business model.

Once you've got a shortlist, it's time to dig a bit deeper with some key questions. How they answer will tell you a lot about their process, their expertise, and how they’ll gel with you day-to-day.

Here are a few essential questions to get the conversation started:

The answers to these questions do more than just test their technical skills. They reveal their commitment to communication. You need a partner who's easy to reach and can break down complex financial stuff in a way that makes perfect sense to you.

Getting a clear picture of how you'll be charged is crucial for avoiding any nasty surprises down the line. Bookkeeping services in the UK generally use a few common pricing structures, and the best fit depends on your business's needs and how predictable your workflow is.

Fixed Monthly Fees

This is a popular one. You pay a set fee each month for a clearly defined list of services. It’s brilliant for budgeting because you know exactly what your outlay will be. This model is perfect for businesses with a fairly consistent volume of transactions.

Hourly Rates

With this approach, you pay for the exact time spent on your accounts. It can be a cost-effective option if your needs are minimal or fluctuate a lot, but be warned—it can also lead to unpredictable bills during busier months.

When you're comparing quotes, try not to get fixated on the price tag alone. Look at the value you're getting. A slightly pricier fixed-fee package that includes proactive advice and regular reporting could give you a much better return on your investment than the cheapest hourly rate. To understand more about the people behind the service, you can learn about our team's approach to client partnerships. This insight helps you see how a dedicated team can become a genuine asset to your business.

When looking into professional bookkeeping services for small business, one of the first questions on every owner's mind is: "So, what's this going to cost me?" The answer isn't a simple one-size-fits-all number. Instead, understanding the factors that shape the price will help you find a service that fits your budget while delivering genuine value.

Think of it like getting a quote for building work. The final price depends on the size of the job, the complexity of the plans, and the materials you choose. It's exactly the same with bookkeeping; the cost is tailored to your business's unique financial landscape.

Several core elements determine what you can expect to pay. A good bookkeeper won’t just pull a number out of thin air; they’ll take the time to assess your specific situation to give you a fair and accurate quote.

So, what are they looking at? It usually boils down to three things:

Essentially, the more moving parts your business has, the more you should budget for an expert to keep it all in order.

In the UK, bookkeepers generally use one of three main pricing models. Each has its pros and cons, and the right choice really depends on what your business needs in terms of predictability and flexibility.

Seeing bookkeeping as just another expense is a mistake. It’s far better to view it as an investment in your financial clarity—one that pays for itself by saving you time, preventing costly errors, and giving you the data to make smarter decisions for growth.

To help you get a clear picture, here's a look at the common pricing structures you’ll come across.

This table breaks down the common pricing models, helping you figure out which one might be the best fit for your company’s budget and needs.

For the majority of small businesses, a fixed monthly package strikes the best balance between value and predictability. It lets you budget effectively and build a proper partnership with your bookkeeper, all without the fear of surprise invoices. By understanding these options, you can confidently choose a plan that supports your financial goals and helps your business thrive.

Hiring an expert is a fantastic step forward, but the best results always come from a strong partnership. To really squeeze the most value out of your bookkeeping services for small business, it pays to get a few simple, organised habits in place first. Think of it like preparing a worksite before the builders arrive; a little groundwork makes the whole project run smoother, faster, and more efficiently.

When you create a clear and steady flow of information, you’re giving your bookkeeper the tools they need to do their best work. This approach minimises your own admin headaches and turns the relationship from a simple service into a powerful financial partnership. The goal here is simple: spend less time on paperwork and more time growing your business.

If there's one habit that will make the biggest difference, it's opening a dedicated business bank account. When business and personal spending get mixed up, it creates a tangled mess that your bookkeeper has to painstakingly unravel, transaction by transaction. That confusion doesn't just eat up their time (and your money); it also seriously increases the risk of errors and missed tax-deductible expenses.

Keeping your finances separate from day one brings instant clarity. It creates a clean, undeniable record of all your business income and spending.

A dedicated business account is the bedrock of clean bookkeeping. It draws a clear line in the sand, making your financial story easy to read and simple to manage for both you and your bookkeeper.

This simple act is the first move towards building a more professional and organised financial system.

The days of handing your bookkeeper a shoebox overflowing with faded receipts are, thankfully, long gone. Modern bookkeeping runs on digital tools that make capturing and sharing information almost effortless. Apps like Dext or AutoEntry let you snap a photo of a receipt the moment you get it, instantly sending the data straight to your bookkeeper.

This process is a game-changer for a few key reasons:

Beyond just choosing the right partner, you can get ahead by implementing some of your own internal processes, like these practical small business bookkeeping tips. Adopting these digital habits also simplifies compliance with government initiatives like Making Tax Digital. You can find out more by checking out our guide on Making Tax Digital for Self Assessment.

Your bookkeeper is much more than a number-cruncher. They're a key advisor who can offer brilliant insights into your business's performance, but that can only happen if you talk to them. Don't just wait for a problem to pop up before getting in touch.

Try scheduling regular, brief check-ins—maybe once a month or every quarter—to go over your financial reports together. This is your chance to ask questions, discuss spending trends, and chat about your future goals. This kind of proactive dialogue helps your bookkeeper understand the story behind the numbers, allowing them to provide more relevant and strategic advice. Ultimately, a strong working relationship built on trust and open communication is the key to a truly successful financial partnership.

Stepping into the world of business finance can feel like learning a new language. To make things clearer, here are some straightforward answers to the questions we hear most often from small business owners.

This really depends on your business. For a sole trader with fairly simple finances, you could be looking at anywhere from £100-£250 a month. If you’re running a limited company with employees and VAT returns to think about, that figure is more likely to be in the £250 to £600+ per month range.

Ultimately, the price tag comes down to how many transactions you have, how complex your business is, and exactly what services you need help with.

It’s best to think of it as day-to-day versus the big picture. Your bookkeeper is in the trenches with you, managing the daily financial records. They’re tracking every sale and expense, making sure the bank accounts line up, and handling things like payroll.

An accountant then takes all that beautifully organised data and uses it for higher-level thinking. They'll handle your tax planning, offer strategic advice on growth, and help you understand what the numbers mean for your business's future.

A bookkeeper builds the accurate financial foundation, while an accountant uses that foundation to help you build your future. Both roles are essential for robust financial health.

Absolutely, especially when you’re just starting out and things are simple. Modern tools like Xero and QuickBooks have made DIY bookkeeping much more manageable.

But as your business grows, the paperwork and complexity tend to grow with it. Many business owners reach a point where the hours spent wrestling with spreadsheets are better spent actually running and growing their company. That's when handing it over to a professional becomes a very smart investment.

This can vary, but a monthly check-in is a great rule of thumb. It’s the perfect opportunity to go through your financial reports, flag any unusual spending, and get answers to any questions you have.

A good bookkeeper will always be available for a quick query when something pops up, so you never feel out of the loop. The goal is to feel confident and in control of your finances at all times.

Ready to gain complete clarity and control over your business finances? The expert team at GenTax Accountants is here to provide the dedicated bookkeeping support you need to thrive. Get in touch with us today for a free consultation!