On the surface, accounting and bookkeeping might seem like two sides of the same coin. They’re the engine room of your company’s finances, covering everything from day-to-day transactions to high-level strategic planning. Bookkeeping tracks every pound coming in and going out, while accounting tells you what all that data actually means for your business.

To get the most out of professional financial management, you first need to know the difference between its two core functions. Many business owners use “bookkeeping” and “accounting” interchangeably, but they are two very distinct—yet deeply connected—disciplines. Get them working together, and you get a crystal-clear picture of your company's performance.

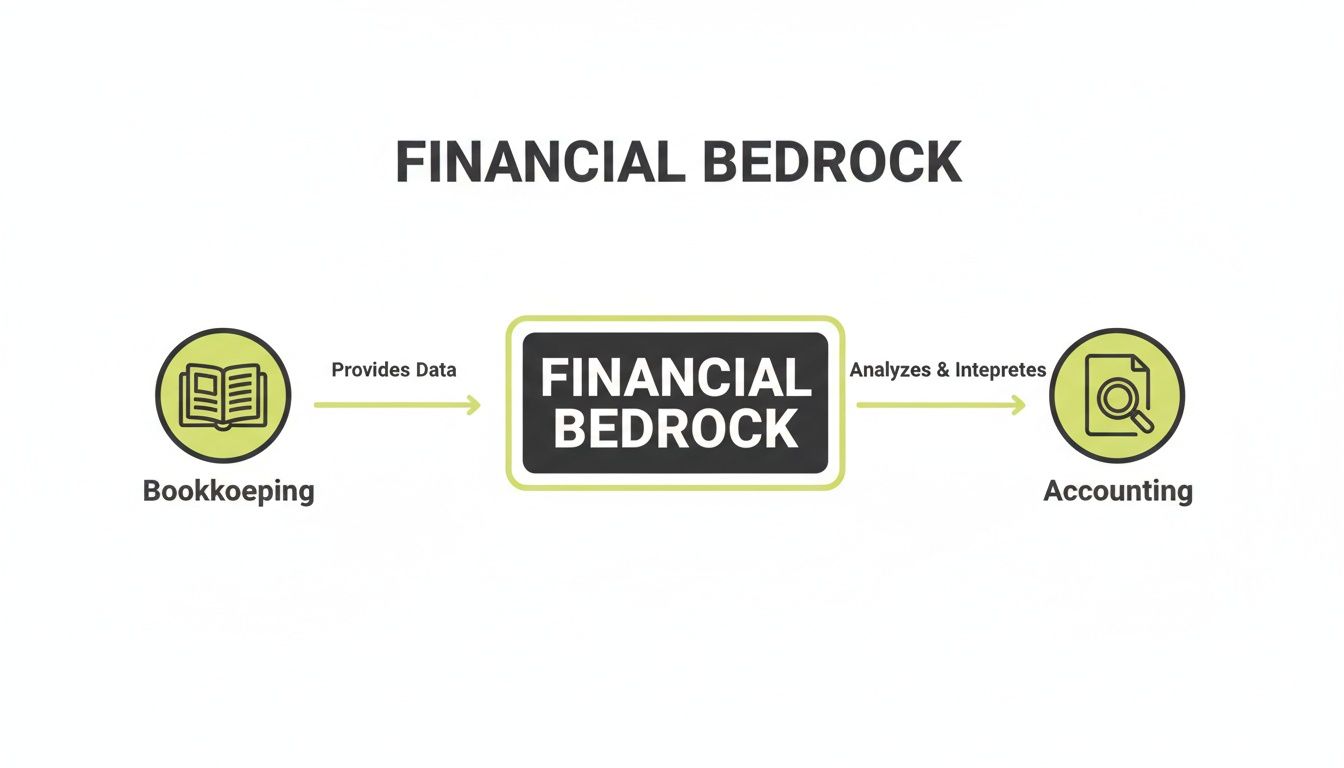

Think of it like building a house. Bookkeeping is the painstaking work of sourcing, measuring, and cutting every single brick and piece of timber. It’s the precise, daily grind of recording financial transactions—sales, purchases, payments, and receipts. This process makes sure every bit of data is accurate and filed away correctly. Without that solid foundation, the whole structure would be unstable.

Accounting, on the other hand, is the architect’s job. The accountant takes all those perfectly prepared materials (your bookkeeping data) and uses them to design and build the house. They analyse, summarise, and interpret the financial records to create reports like profit and loss statements and balance sheets. This is the big-picture view that tells the story behind the numbers.

At its heart, bookkeeping is all about collecting and organising data. It’s the very first, and most critical, step in managing your finances properly. A bookkeeper’s main jobs include:

This is a continuous, detail-heavy job. Clean books aren’t just nice to have; they're the non-negotiable starting point for any meaningful financial analysis.

If bookkeeping is about recording the past, accounting is about using that past to build a better future. An accountant takes the organised data from the bookkeeper and turns it into intelligence you can actually use. Their work is much more analytical, focused on turning raw numbers into strategic insights that help you grow.

An accountant’s real job is to give you a clear financial story. They help you understand not just what happened, but why it happened and what you should do next. This is what turns a simple record of transactions into a powerful tool for making smart decisions.

This strategic oversight includes preparing essential financial statements and making sure your business is meeting all its legal duties. For instance, when an accountant prepares your detailed year-end accounts, they aren't just ticking a compliance box. They're giving you a comprehensive summary of your annual performance that provides a solid foundation for next year's planning.

Right, so we've untangled the difference between bookkeeping and accounting. Now, let's get into the nitty-gritty of the actual services that keep your business financially sound and on the right side of the law. These aren't just tick-box exercises; they're the engine room of your financial operations. Getting them right directly impacts your ability to make smart decisions, manage your cash, and grow sustainably.

Think of it this way: daily bookkeeping lays the foundation by capturing all the raw data. Accounting then takes that solid base and builds strategic insights on top of it.

As you can see, you simply can't have high-quality accounting without meticulous, consistent bookkeeping propping it all up.

To give you a clearer picture, here's a quick rundown of the key services and what they actually do for your business.

Each of these plays a vital role. Let's break them down a bit further.

At its heart, bookkeeping is the disciplined act of recording every single financial transaction your business makes. It’s the meticulous, day-in-day-out work of logging every invoice, receipt, and payment accurately. This isn't just about punching numbers into a spreadsheet; it's about creating a bulletproof record of your company's financial life.

Done properly, this gives you a real-time view of your cash flow. You know exactly what money is coming in and where it’s going out. This clarity is what stops those nasty surprises, like an unexpected cash crunch, and keeps your financial records trustworthy.

Think of your bookkeeper as the guardian of your financial data. Their work ensures that the numbers are not just recorded, but are accurate, organised, and ready for analysis. This diligence is what transforms a simple ledger into a powerful business tool.

Without this foundational work, everything else crumbles. Tax returns become a guessing game, financial reports are unreliable, and any strategic planning is built on shaky ground. For a deeper look, check out our guide on professional bookkeeping services that build that solid base.

Preparing year-end accounts is a legal must for all limited companies in the UK. This process rolls up your entire financial year's activity into a set of formal statements, like the balance sheet and the profit and loss account. These documents are the definitive snapshot of your company's health and performance over the last 12 months.

These accounts get filed with Companies House and HMRC, ticking that big compliance box. But their value goes way beyond just staying legal. Year-end accounts are crucial for:

Hand-in-hand with this is filing your corporation tax return. This is the critical task of calculating your company's taxable profit and working out how much tax you owe HMRC. A good accountant ensures you claim every allowable expense and tax relief possible, cutting your liability down as much as legally possible. Managing the money owed to you is also key; a strong accounts receivable process can seriously boost your year-end profits, as this comprehensive guide to receivable management services explains.

Value Added Tax (VAT) can be a real headache. If your business turnover crosses the government threshold, you’re legally required to register for VAT. This means you have to charge VAT on your sales and then pay what you owe to HMRC. It sounds simple, but the rules can be incredibly complex.

Professional VAT services take this entire mess off your plate. This typically includes:

A huge part of VAT management now is Making Tax Digital (MTD). MTD for VAT means you have to keep digital records and submit your returns using compatible software. An accountant makes sure you’re using the right tools and following the right processes to avoid any penalties from HMRC.

Paying your team correctly and on time is non-negotiable. But payroll is so much more than just sending a bank transfer. It’s a complex job with heavy legal responsibilities, from calculating income tax and National Insurance to handling student loan and pension contributions.

A dedicated payroll service completely removes this burden. They handle every aspect, from generating payslips and processing payments to submitting real-time information (RTI) reports to HMRC with every single pay run.

On top of that, payroll management also covers auto-enrolment for workplace pensions. It’s a legal duty for employers to enrol eligible staff into a pension scheme and make contributions. Getting this wrong can lead to hefty fines from The Pensions Regulator. Outsourcing your payroll means your team gets paid perfectly, and your business meets all its legal duties as an employer.

While year-end accounts look backwards, management accounts are all about looking forward. These are internal financial reports, usually created monthly or quarterly, designed to give you the clarity you need to make strategic decisions. They dig much deeper than a basic profit and loss statement.

Management accounts can include:

This is where raw data becomes actionable intelligence. It helps you spot trends, clamp down on overspending, and make proactive decisions that steer your business towards its goals. Management accounts are the bridge between daily bookkeeping and high-level strategy, giving you the confidence to lead.

Remember the days of drowning in a sea of paper receipts and wrestling with clunky spreadsheets? Thankfully, those are long gone. Technology has completely overhauled the world of accounting and bookkeeping, making financial management faster, more accurate, and genuinely more valuable for business owners.

The old, cumbersome manual processes have been replaced by powerful cloud-based platforms like Xero and QuickBooks. These tools give you a live dashboard showing your company’s financial pulse in real-time. This instant access means you and your accountant are literally on the same page, looking at the same up-to-the-minute information, making collaboration seamless.

This digital shift has made modern accountancy firms far more efficient. In fact, UK practices are seeing remarkable growth, with 79% reporting increased revenue and 74% seeing higher profits. This success is driven by optimising workflows (35%) and using tech to build deeper client relationships, which has boosted client satisfaction by an impressive 87%.

Modern accounting software automates many of the tedious tasks that once ate up hours of manual work. Bank transactions are automatically imported and categorised, invoices are generated and sent with a few clicks, and payment reminders go out without you lifting a finger.

Grasping the concept of workflow automation is key here. It’s not just about saving time; it’s about slashing the risk of human error and freeing up your accountant to focus on strategic advice instead of just punching in numbers.

With real-time data at your fingertips, financial management becomes proactive, not reactive. You no longer have to wait until the end of the month to find out where you stand. You can spot a cash flow issue early, identify your most profitable services instantly, and make confident decisions based on what’s happening right now.

This immediate clarity is a game-changer. It turns your financial data from a historical record into a powerful tool for future growth. Implementing the right tools is a critical part of this journey, and a smart approach to technology transformation can unlock massive operational benefits.

This leap in efficiency has also transformed how accounting services are priced. The old model of hourly billing often created a frustrating dynamic—you might hesitate to call your accountant for fear of racking up a huge, unpredictable bill.

Today, forward-thinking firms have moved to a fixed monthly pricing model. This approach gives you complete transparency and predictability, letting you budget effectively without any nasty surprises at the end of the month.

Here’s why a fixed-fee structure creates a much better partnership:

This modern approach ensures your accountant is a true partner invested in your long-term success, not just a service you pay for by the hour.

Just like a sapling needs different care than a mature oak tree, your business’s financial needs will evolve dramatically as you grow. The right accounting and bookkeeping support isn’t a one-size-fits-all product; it has to be matched to your specific stage of the journey. Think of it as a catalyst for growth, not just a box-ticking exercise for HMRC.

Figuring out what you need, and when you need it, is the secret to building a robust financial strategy that actually supports your ambitions. Let's walk through the typical business journey and the services that make sense at each phase.

When you’re just getting started, the name of the game is survival. Your financial priorities are all about control, compliance, and clarity. Getting these basics right from day one saves you from monumental headaches later on and builds a solid foundation for everything that comes next.

At this early stage, your core needs are pretty straightforward:

Example in Action:

A freelance graphic designer kicks off her business. She brings an accountant on board for basic bookkeeping and to handle her annual self-assessment. By keeping her personal and business finances separate and her books clean from the start, she dodges a common pitfall that trips up countless new entrepreneurs. This simple move gives her a clear view of her profitability on each project and means no nasty surprise tax bills.

Once your business starts to gain real momentum, moving from a small operation to a Small or Medium-sized Enterprise (SME), the complexity ramps up fast. You might be hiring staff, taking on bigger contracts, or launching new products. Your financial services have to evolve to manage this growth and give you the deeper insights you now need.

The focus shifts from pure survival to strategic expansion. This is where your service needs broaden:

When your business is well-established, the game changes again. You’ve got solid processes in place, but now the focus shifts towards optimisation, high-level strategy, and long-term financial planning. Your relationship with your accountant should become a genuine strategic partnership, aimed squarely at maximising efficiency and profitability.

At this stage, you’re looking for more sophisticated support:

We've got years of experience helping businesses at every single point in this journey. You can learn more about the specific sectors and business types we help on our website. This tailored approach means you always get the most relevant and impactful accounting and bookkeeping services for your unique situation.

Picking the right financial partner is one of the most important decisions you'll make for your business. This isn't just about finding someone to file your taxes once a year; it's about finding an expert who will help you grow. This practical checklist is designed to help you look past the sales pitch and find the perfect fit.

A great accounting firm should feel like an extension of your own team. They need to get your industry, speak your language, and be genuinely invested in seeing you succeed. Here’s what to look for.

First things first, check their credentials. Are their accountants accredited by recognised UK bodies like the ACCA (Association of Chartered Certified Accountants) or ICAEW (Institute of Chartered Accountants in England and Wales)? This is your baseline guarantee of quality and professional standards.

Next, dig into their specific industry experience. An accountant who knows eCommerce inside-out will understand payment gateways and stock management, while someone focused on construction will be a pro at the Construction Industry Scheme (CIS). Don't be shy—ask for real-world examples of their work with businesses like yours.

Here’s an overlooked but crucial point: ask about team stability. High staff turnover at an accounting firm can mean inconsistent service and a constant loss of knowledge about your business. It's perfectly fine to ask how they look after their team.

In this day and age, your accountant has to be tech-savvy. They should be fluent in cloud accounting software like Xero or QuickBooks, because these tools are the foundation of any modern, efficient finance operation.

Ask them how they use technology to make your life easier. Do they have a client portal for sharing documents securely? Do they use apps to automate the painful process of capturing receipts and entering data? Their answers will tell you whether they’re a forward-thinking firm or one that's stuck in the past.

Finally, get a feel for their communication style and pricing. You need someone who is responsive and can break down complex financial topics into plain English. Pay attention during your first few chats—do they listen properly? Are their answers clear and direct?

You also need to demand total transparency on fees. Look for a firm that offers fixed monthly pricing. This simple change aligns their goals with yours, encouraging them to be proactive without you having to worry about a massive surprise bill every time you pick up the phone. It builds a genuine partnership focused on value, not billable hours.

Finding the right provider is a serious investment in your company’s future. The UK accounting industry is facing its own challenges; a recent UK accounting industry report found that 78% of firms rank recruitment as a top concern, which can directly impact the quality of service you receive. Vetting a provider's team and expertise is more important than ever. By using this checklist to evaluate the full range of accounting and bookkeeping services on offer, you can find a partner who won’t just manage your finances—they’ll actively help you smash your business goals.

Alright, let's wrap up by tackling some of the most common questions business owners have when they're on the fence about getting professional financial help. This is where we cut through the jargon and give you the straight answers you need to decide what’s next for your business.

We’ll dig into the big three that come up time and time again. Getting your head around these will give you the clarity you need to invest in the right support.

This is always the first question, but the honest answer is: it depends. The cost of accounting and bookkeeping services is tied directly to your business's size, its complexity, and exactly what you need help with. A sole trader needing a simple self-assessment return will pay a fraction of what a growing SME needs for monthly management accounts, payroll for ten employees, and quarterly VAT returns.

But the pricing model is just as important as the price tag. My advice? Steer clear of traditional hourly billing. It creates unpredictable costs and can make you think twice before picking up the phone to ask a quick question. Instead, look for an accountant who offers fixed monthly pricing.

This model just makes more sense for a modern business:

As a ballpark, a typical package for a small limited company might range from £100 to £300 per month. This would usually cover the core compliance stuff, like your year-end accounts and tax returns. The more support you need, the more you can expect to invest.

Lots of founders start out doing their own books, and that's fine for a while. But there are clear signals that it’s time to call in an expert. Wait too long, and you risk costly mistakes, missed opportunities, and a whole lot of stress.

You should seriously consider hiring an accountant when you hit these milestones:

Absolutely. This is probably the biggest myth out there—that accounting is just another cost on the P&L. The reality? A great accountant is an investment that should pay for itself, often several times over. They save you money in ways you can see and in ways you can't.

A proactive accountant does more than just keep you compliant; they become a strategic partner who actively finds ways to improve your financial health. Their value is measured not just by the tax they save you, but by the costly errors they prevent and the growth they help you achieve.

Here’s how they deliver that return:

Ultimately, they free you up to focus on what you're brilliant at—running and growing your business.

Ready to turn your financial data into a powerful tool for growth? At GenTax Accountants, we provide tech-driven accounting and bookkeeping services with fixed monthly pricing, so you always know where you stand. Get in touch with our team today to see how we can help your business thrive.