In the world of business finance, what you owe is just as important as what you own. Liabilities, the financial obligations a company holds, are a fundamental component of the balance sheet and a critical indicator of financial health. For many business owners, contractors, and landlords, however, the various types of liabilities can seem like a complex puzzle. Mismanaging these obligations can lead to cash flow problems, compliance issues, and stunted growth.

This guide demystifies the topic by providing clear, practical examples of liabilities in accounting. We will break down seven common liabilities, from Accounts Payable to Sales Tax Payable, exploring not just what they are, but how they impact your company's financial standing.

By understanding these concepts, you can move beyond simple bookkeeping and begin to strategically manage your obligations. This knowledge is the first step towards transforming financial duties into opportunities for better control, enhanced planning, and sustainable business success. You will learn to recognise, measure, and handle these debts effectively, ensuring your business remains robust and compliant. Let's explore the specific liabilities every business owner needs to master.

Accounts Payable (AP) represents the short-term financial obligations a business has to its suppliers or creditors for goods and services acquired on credit. This is one of the most fundamental examples of liabilities in accounting, appearing as a current liability on the balance sheet because it is typically due within one operating cycle, often 30 to 90 days. It reflects the day-to-day operational purchasing a company undertakes to maintain its inventory, supplies, and services.

For instance, a UK-based construction company owes £50,000 to a building materials supplier for a recent delivery of concrete and steel. This amount is recorded as accounts payable until the invoice is paid. Similarly, a local café with a £2,000 balance due to its coffee bean roaster has an AP liability.

Effective management of accounts payable is crucial for maintaining healthy cash flow and strong supplier relationships. It is more than just paying bills; it is a strategic function that can impact a company's financial stability and reputation.

To turn AP management into a strategic advantage, consider implementing the following tactics:

Properly managing these liabilities is a core component of sound financial administration. For more detailed support with your company's bookkeeping, explore professional accounts services from gentax.uk.

Notes Payable are formal written promises to repay a borrowed amount of money on a specific future date or over a set period. Unlike the more informal accounts payable, notes payable are documented through a promissory note, which typically includes the principal amount, interest rate, and repayment terms. This is a common example of examples of liabilities in accounting that can be classified as either a current or non-current liability on the balance sheet, depending on whether the repayment is due within one year or longer.

For instance, a small technology start-up secures a £50,000 bank loan to purchase new servers; this formal loan agreement is recorded as a note payable. Similarly, if a larger corporation needs funding for a major expansion project and issues a £10 million bond to investors, this creates a long-term note payable liability on its books. These formal credit agreements are fundamental for financing significant investments and managing working capital.

Managing notes payable effectively is critical for maintaining a company's financial health and creditworthiness. It involves more than simply making scheduled payments; it requires careful planning and a deep understanding of the loan's terms and covenants to avoid default and costly penalties.

To manage notes payable strategically and support business growth, business owners should adopt these practices:

Accrued expenses are costs a business has incurred but has not yet paid or formally recorded through an invoice. They are recognised at the end of an accounting period to ensure financial statements accurately reflect all obligations. This makes them crucial examples of liabilities in accounting, upholding the matching principle by aligning expenses with the revenues they helped generate in the same period. They appear as current liabilities on the balance sheet as they are typically settled within the next year.

For example, a UK marketing agency's employees worked the last week of December, earning £15,000 in wages. However, payday isn't until the first week of January. To ensure December's financial statements are accurate, the company must record a £15,000 accrued salary expense. Similarly, a business might estimate and accrue £2,500 for electricity used in the month, even though the official utility bill has not yet arrived.

Properly managing accrued expenses is vital for accurate financial reporting and internal decision-making. It prevents the understatement of liabilities and overstatement of profits, providing a true and fair view of a company's financial health.

To effectively manage accrued expenses and enhance financial integrity, business owners should implement the following practices:

Accurate tracking of these liabilities is a cornerstone of diligent financial management. For professional assistance with maintaining precise financial records, consider expert bookkeeping services from gentax.uk.

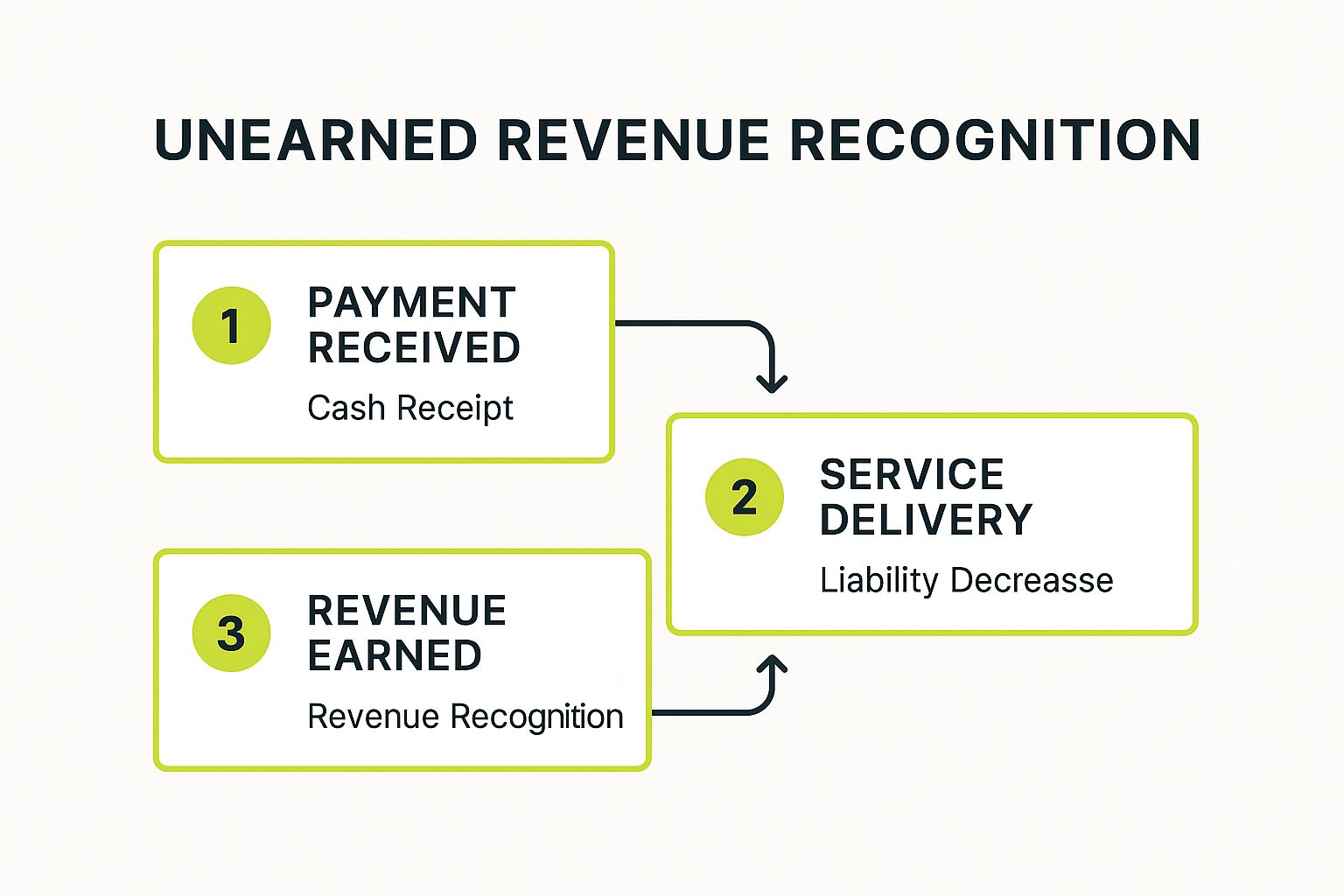

Unearned revenue, also known as deferred revenue, represents payments received by a company from its customers for goods or services that have not yet been delivered or rendered. This is one of the key examples of liabilities in accounting, appearing on the balance sheet as a liability because it signifies the company's obligation to its customers. The cash has been received, but the company owes a service or product in the future.

For instance, a software-as-a-service (SaaS) company in the UK receives an annual subscription fee of £1,200 from a client at the beginning of the year. This entire amount is initially recorded as unearned revenue. Each month, as the service is provided, the company will recognise £100 of this liability as earned revenue. Similarly, a magazine publisher who collects a £60 annual subscription fee has an unearned revenue liability that decreases by £5 each month as the magazine is delivered.

This infographic illustrates the standard process flow for recognising unearned revenue.

The diagram clearly shows how the transaction transitions from a cash receipt to a liability on the balance sheet, and finally to recognised revenue on the income statement as the company fulfils its obligation.

Properly managing unearned revenue is critical for accurate financial reporting and provides insights into future revenue streams. It is particularly vital for subscription-based business models, where it acts as an indicator of future performance and customer commitment.

To manage unearned revenue effectively and turn it into a financial advantage, business owners should consider the following:

Payroll Liabilities include all financial obligations a company owes related to employee compensation that has been earned but not yet paid. These are significant examples of liabilities in accounting, encompassing not just the net pay due to employees but also amounts withheld for taxes and other deductions. This category appears on the balance sheet as a current liability, as these obligations must typically be settled in a short period, often within weeks or a month.

For example, a UK tech firm's payroll register shows gross wages of £100,000. From this, it withholds £20,000 for PAYE (Income Tax and National Insurance), £5,000 for employee pension contributions, and £1,000 for student loan repayments. The company also owes its own employer National Insurance contributions of £13,800. The total payroll liability is £39,800 owed to HMRC and pension providers, plus the £64,000 net pay owed to employees.

Managing payroll liabilities effectively is a critical compliance and operational function. It involves much more than just paying staff; it requires meticulous record-keeping and timely remittance to various government agencies to avoid severe penalties, interest charges, and legal issues. Proper management ensures both employee satisfaction and regulatory adherence.

To transform payroll liability management from a complex chore into a streamlined process, business owners should consider these tactics:

Navigating the complexities of employee compensation is a vital part of financial stewardship. For expert assistance in managing your company's obligations, consider professional payroll services from gentax.uk.

The Current Portion of Long-Term Debt (CPLTD) is a liability that represents the principal amount of a long-term debt obligation that must be settled within the next 12 months. This is a crucial reclassification among examples of liabilities in accounting, where a portion of a non-current liability is moved to the current liabilities section of the balance sheet. This adjustment provides a more accurate view of a company's immediate cash requirements and its ability to meet short-term obligations.

For example, a manufacturing firm in Manchester has a £1,200,000 loan for a new piece of equipment, with principal payments of £120,000 per year. The £120,000 due in the upcoming financial year is classified as the CPLTD. The remaining £1,080,000 stays categorised as a long-term liability. This distinction is vital for liquidity analysis.

Effectively managing the current portion of long-term debt is essential for maintaining liquidity and financial stability. It requires proactive financial planning to ensure that sufficient cash is available to meet these significant, scheduled outflows without disrupting daily operations or strategic investments. Accurate forecasting and classification of CPLTD are key to avoiding solvency issues.

To manage upcoming debt obligations strategically, business owners should integrate the following practices into their financial management routine:

Careful management of these liabilities is a hallmark of sophisticated financial leadership. For expert guidance in strategic financial planning, consider the benefits of a fractional finance director to help navigate these complexities.

Sales Tax Payable represents the amount of sales tax a business collects from its customers on behalf of a governing tax authority. This is a classic example of a current liability because the business is simply acting as a collection agent for the government. The collected funds do not belong to the company and must be remitted, typically on a monthly or quarterly basis, to the appropriate state or local tax agency.

For instance, a retail clothing shop in Manchester collects Value Added Tax (VAT) from customers on every sale. This collected VAT is recorded as a liability on its balance sheet until it is paid to HMRC. Similarly, an e-commerce company selling products across Europe must navigate and remit various VAT rates, creating a complex but critical sales tax payable liability.

Properly managing sales tax payable is not just a bookkeeping task; it is a crucial compliance function that protects a business from significant penalties, audits, and legal issues. For businesses operating in multiple jurisdictions, this becomes a key strategic challenge that demands robust systems and processes to ensure accuracy and timeliness.

To manage sales tax obligations effectively and avoid common pitfalls, business owners should consider the following strategies:

Managing these liabilities is a fundamental aspect of financial compliance. For expert assistance with VAT and other tax obligations, you can explore professional guidance on VAT returns from gentax.uk.

The journey through these fundamental examples of liabilities in accounting reveals a powerful truth: obligations are not merely financial drains but strategic instruments. Understanding liabilities goes beyond simple bookkeeping; it is a core competency for any business owner, from a sole trader managing accrued expenses to a limited company director overseeing long-term debt covenants. Each liability, whether it's the short-term rhythm of accounts payable or the long-term commitment of a business loan, tells a story about your company's operational health, its relationships with suppliers, and its capacity for future growth.

Viewing these obligations through a strategic lens transforms them from passive entries on a balance sheet into active levers for optimisation. Proactive management of your liabilities is central to maintaining liquidity, strengthening stakeholder trust, and ensuring robust regulatory compliance.

Mastering the nuances of liabilities empowers you to make smarter, more informed decisions. Here are the core principles to integrate into your financial strategy:

To translate this understanding into tangible results, focus on implementing a robust system for liability management. Start by conducting a thorough review of your current liabilities. Categorise them, analyse their due dates, and assess the interest or penalties associated with each.

Leverage accounting software to automate tracking and set reminders for payment deadlines. This simple step can prevent costly oversights and provide a clear, real-time overview of your company’s financial commitments. By embracing these practices, you shift from a reactive to a proactive stance, turning financial obligations into a source of competitive advantage and sustainable growth for your UK business.

Ready to transform your approach to financial management? The team at GenTax Accountants specialises in helping UK businesses navigate the complexities of accounting liabilities with precision and strategic insight. Our digital-first approach and expert guidance ensure you can manage your obligations effectively, optimise your financial health, and focus on scaling your business. Discover how GenTax Accountants can empower your financial strategy today.