End-of-year accounting is the process of tying up all your financial loose ends from the past twelve months. It's a bit like an annual health MOT for your business, where you review, reconcile, and double-check every transaction to make sure everything adds up. The end goal is to produce official financial statements for stakeholders and the tax man.

Think of your business's financial year like a story with a beginning, middle, and end. Throughout the year, you have your ups and downs—periods of great sales, and other times when cash flow feels a bit tight. The end-of-year process is where you take a step back and read that story from start to finish.

This isn't just a box-ticking exercise for HMRC. It's a crucial strategic moment that reveals the true health of your company. The final reports tell you exactly where your business is strong, where it's vulnerable, and what you need to focus on for the year ahead.

At its heart, closing your books is about creating a single, accurate narrative of your business's financial journey over the last year. It’s a process where several key activities build on one another to paint a reliable and honest picture.

The main objectives are pretty straightforward:

The government's focus on accuracy is serious. In the 2024-2025 financial year, for instance, HMRC collected a staggering £875.9 billion in revenue and protected another £48.0 billion through its compliance work. That number tells you how much emphasis is placed on getting the figures right. You can find more details on HMRC’s compliance efforts on their official site.

Before we dive deeper, let's break down the main components of this process. The table below provides a quick overview of the key activities and why each one matters.

Each of these steps feeds into the next, ensuring the final reports are built on a solid foundation of verified data.

Closing the books is more than an accounting task; it’s the moment you translate a year’s worth of transactions into a clear narrative of performance, risk, and opportunity. It sets the foundation for every strategic move you'll make in the coming year.

Ultimately, the goal is to make sure every penny is accounted for. It's a thorough process, and getting expert help can make all the difference. Understanding the full scope of available accounting services ensures you have the support needed to get it right. This financial "MOT" isn't just a requirement—it's one of your most powerful tools for building a resilient and successful business.

Getting your end-of-year accounting done is one thing, but filing everything on time is a completely different ball game. In the UK, missing a deadline isn't just a minor slip-up; it triggers automatic penalties and can draw unwanted attention from HMRC. Staying organised is the only way to avoid last-minute stress and unnecessary costs.

Think of HMRC and Companies House deadlines as fixed appointments in your business calendar that you simply cannot miss. Every business structure has its own set of dates and required documents, whether you're a private limited company, a sole trader, or in a partnership. Getting your head around this timeline is the first step towards a smooth, compliant year-end.

If you run a limited company, you're answering to two main government bodies: Companies House and HMRC. They work in tandem, but their deadlines are distinct and equally important to hit.

Your company's Accounting Reference Date (ARD) is the pivotal date that defines your financial year-end. It’s usually the last day of the month your company was incorporated. Once that date passes, the clock starts ticking on two critical submissions:

Missing the Companies House deadline triggers automatic penalties, starting at £150 for being up to one month late and rocketing to £1,500 for filings over six months late. Late payment of Corporation Tax also racks up interest charges, so being prompt isn't just good practice—it's a financial necessity.

For sole traders and partnerships, your world revolves around the UK tax year, which runs from 6th April to 5th April. Your main task is filing the Self Assessment tax return, which is a full rundown of your income and expenses for that period.

The deadlines for Self Assessment are fixed and apply to everyone:

These dates are non-negotiable. It’s why so many business owners seek professional help to make sure everything is filed accurately and on time. To get a clearer picture of your own responsibilities, you can learn more about filing your tax returns and see what support is available.

Failing to meet these deadlines results in an immediate £100 penalty—even if you have no tax to pay or have already paid it. Further delays lead to even more penalties, which can quickly spiral. Building your year-end accounting schedule around these key dates is essential for protecting your business's financial health and reputation.

Trying to tackle your end-of-year accounting can feel like you're building a massive piece of flat-pack furniture with the instructions missing. It’s a big job, but it doesn't have to be a nightmare.

To help you get it right, we’ve put together a step-by-step checklist. Think of it as your roadmap, breaking down a daunting project into a series of clear, manageable tasks you can tick off one by one. Following these steps will help you build a solid foundation for accurate accounts and a much less stressful tax season.

Before you can even think about running reports, you need to get all your paperwork in one place. This is the bedrock of the entire process, so being thorough here will save you a world of pain later. A single missing invoice can throw everything off.

Start by rounding up all the essential documents for the financial year.

A classic mistake is underestimating just how long this takes. You'd be surprised how much time accountants spend just chasing down missing bits of paper. Start this step early—it gives you a crucial buffer to find that elusive receipt without a deadline breathing down your neck.

To help you keep track, here’s a quick rundown of the most important documents you'll need to pull together.

A checklist of the key financial documents and reports needed to complete the end-of-year accounting process accurately.

Having this information organised from the outset will make the next steps infinitely smoother.

Once you have your statements, it’s time for reconciliation. This is where you match the transactions in your accounting software with what your bank and credit card statements say. It’s a bit like being a financial detective—your mission is to make sure the money your books say you have is exactly what the bank knows you have.

This step is your best defence against errors and potential fraud. Go through each account, line by line, ticking off the entries that match and immediately investigating anything that doesn’t add up. Most modern accounting software helps automate this, but a final manual check is always a smart move.

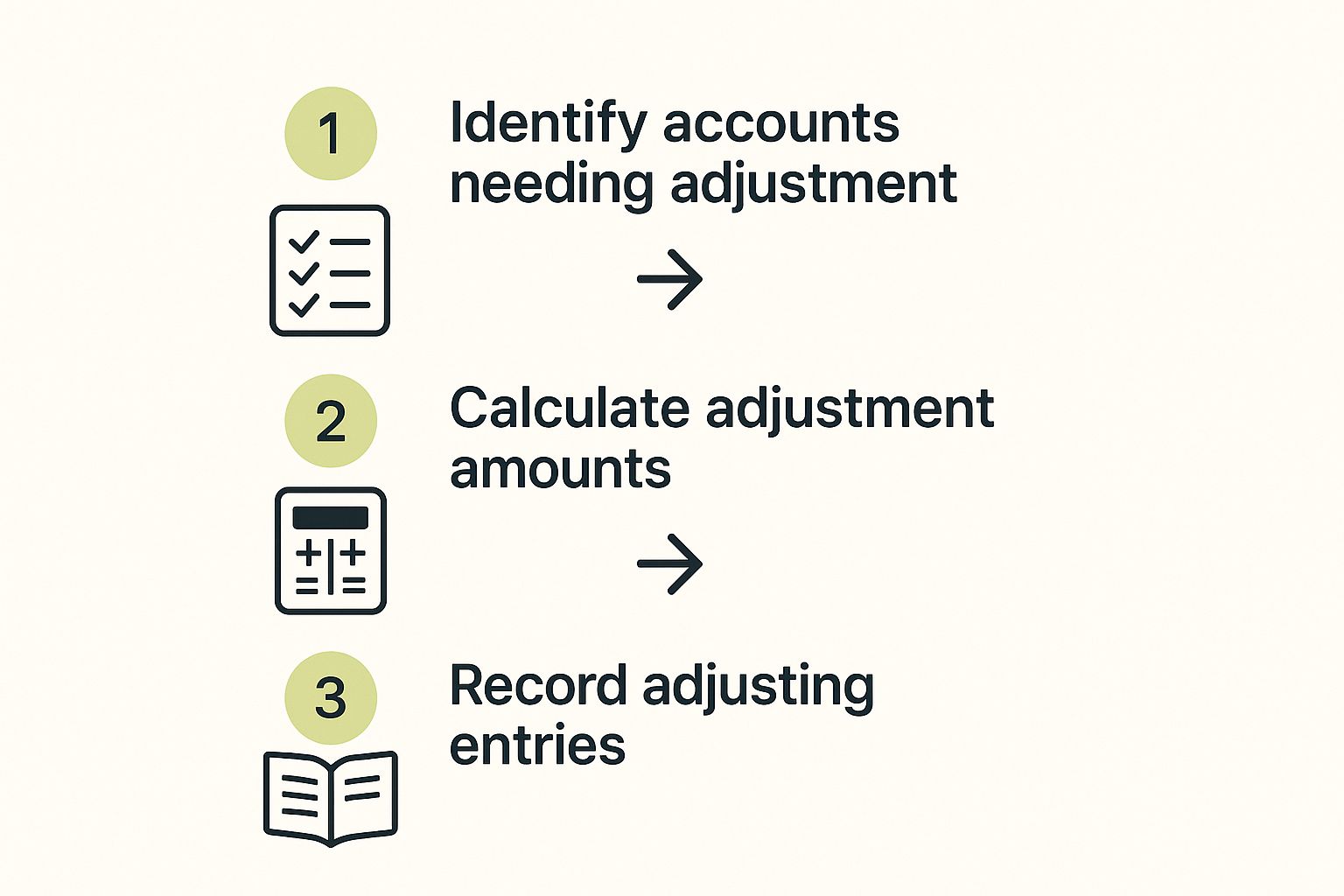

The image below shows the basic workflow for making adjustments when you spot a discrepancy.

It's a simple but vital loop: find the problem, figure out the right number, and then formally record the adjustment in your books.

With your bank accounts squared away, it's time to look at who owes you money and who you owe money to.

First, your accounts receivable. This is all the money your customers owe you. Run a report of all outstanding invoices and pinpoint any that are getting old. You’ll need to chase those up or, if an invoice is clearly never going to be paid, make the tough call to write it off as bad debt.

Next, look at your accounts payable. This is everything you owe to suppliers. Double-check that every single supplier invoice has been entered into your system, even if you haven’t paid it yet. Getting this right is fundamental to reporting your expenses and liabilities accurately.

If your business holds any kind of stock, a physical count at the end of the year isn't optional—it's essential. Your records might claim you have 100 widgets, but after accounting for breakages, theft, or simple human error, the real number could be quite different.

This step ensures both your "Cost of Goods Sold" on the profit and loss statement and your "Inventory" value on the balance sheet are spot on.

Your long-term business assets—things like vehicles, machinery, and office equipment—lose value over time. This loss is an expense called depreciation, and you have to record it every year.

Pull out your fixed asset register, which should list all your major assets. For each one, you'll need to calculate the depreciation for the year based on your company's accounting policy. Recording this correctly provides a much more realistic picture of your company's profitability and overall worth.

Working through these steps properly is key to producing financial statements you can actually rely on. For many businesses, especially limited companies, getting professional help to prepare the final statutory accounts is the best way to guarantee everything is accurate and compliant. It’s a complex field where an expert eye can provide real peace of mind.

Even with the best intentions and a solid checklist, year-end accounting can feel a bit like navigating an obstacle course. Roadblocks are common, but the good news is they're nearly always predictable. Knowing what these hurdles are is the first step to clearing them and getting your books closed without any drama.

From pesky missing receipts to the nasty shock of an unexpected tax bill, these issues can throw a serious spanner in the works, causing delays and a lot of stress. The trick is to stop being reactive—fixing problems as they pop up—and start being proactive. If you can anticipate the common tripwires, you can prevent them from ever being a problem.

This simple shift in mindset turns the year-end from a frantic scramble into a calm, controlled process.

One of the most frequent and frustrating issues is the last-minute hunt for missing receipts and invoices. A single purchase without a paper trail can hold up reconciliations for hours. It’s like trying to solve a puzzle with a crucial piece missing; you just can't see the full picture until it's found.

This headache usually comes from not having a decent system for capturing expenses as they happen. When everyone has to remember to hand in a pile of crumpled receipts at month's end, things are bound to get lost. The solution? Go digital and centralise your records throughout the year, not just at the end.

"A proactive approach to bookkeeping throughout the year is the single most effective strategy for a painless year-end. The goal is to make the year-end close a review process, not a recovery mission."

Another massive hurdle is discovering that your accounts haven't been reconciled for months. When your own records don't line up with your bank statements, it creates a tangled mess that’s incredibly time-consuming to unravel.

Every discrepancy forces you to play detective, tracing its origin. Was it a simple data entry error? A sneaky bank charge? A duplicate transaction?

To dodge this bullet, make bank reconciliation a non-negotiable monthly task. By tackling it in small, regular chunks, you can spot and fix errors right away. This turns a monumental year-end chore into a simple, routine check-in, keeping your financial data accurate and reliable all year long.

Miscategorised expenses are a silent threat to accurate financial reporting. Shoving a marketing expense into the "office supplies" category might seem minor, but these little mistakes add up. Before you know it, your reports are distorted, and you have no real idea where your money is actually going. This leads to flawed budgets and even missed opportunities for tax deductions.

Payroll errors are another common pitfall. Incorrectly calculating PAYE, National Insurance, or pension contributions can land you in hot water with HMRC and lead to some very unhappy employees. Getting this right is critical. For more on this, check out our expert guidance on payroll services for small businesses in the UK to keep your processes spot-on.

The best strategy here is to set up a crystal-clear chart of accounts and make sure anyone involved in bookkeeping knows how to use it. A quick monthly review of your profit and loss statement can also help you spot expenses that look out of place.

Finally, let’s talk about the big one. There’s nothing more stressful than getting to the end of the year and being slapped with a tax bill that’s way bigger than you expected. This "tax shock" is almost always down to poor planning and not having a clear view of your profitability during the year.

The best way to prevent this is to treat your finances like a health check-up—do it regularly. By preparing periodic management accounts, you can:

This continuous monitoring turns your tax bill from a nasty surprise into a predictable, manageable business expense. It gives you the clarity and control you need to plan effectively, not just react.

Trying to handle your end-of-year accounting with manual spreadsheets is a bit like trying to build a house with only a hammer. Sure, it’s possible, but it’s painfully slow, exhausting, and leaves far too much room for costly mistakes. Modern technology turns this process from a stressful marathon into a much more manageable sprint.

The right software doesn’t just store your numbers; it actively works for you. Cloud-based platforms like Xero, QuickBooks, and Sage have become indispensable for keeping accurate, real-time financial records. They give you a single source of truth for your business finances, making the year-end close a process of simple review rather than a frantic scramble to gather data.

The biggest game-changer with modern accounting software is its ability to automate the most repetitive and error-prone tasks. Instead of losing days to manual data entry, these platforms do the heavy lifting. This frees you up to focus on what the numbers actually mean for your business.

Key automated features include:

These tools slash the risk of human error. One study found that manual data entry can have an error rate as high as 4%, which can snowball into significant discrepancies over a full year. Automation almost completely wipes out this risk, ensuring your foundational data is clean and reliable from the get-go.

With several excellent options out there, picking the right platform really comes down to what your business needs. While platforms like Xero and QuickBooks are popular for their user-friendly interfaces, it's crucial to look beyond the surface.

When choosing software, think about your entire financial workflow. The best tool isn't just about bookkeeping; it's about creating an efficient system that seamlessly connects banking, invoicing, payroll, and reporting.

Keep these essential features in mind when you're making your decision:

Adopting the right tech is one of the most powerful things you can do to simplify your end of year accounting. It builds a foundation of accuracy and efficiency that pays you back all year round, transforming a once-dreaded task into a valuable strategic review of your business.

It’s easy to breathe a sigh of relief once your end-of-year accounting is done and dusted. But while it might feel like crossing a finish line, the real value isn’t just in closing the books—it’s in using them to open new doors.

Think of your financial statements as the detailed story of your business’s performance over the last twelve months. This data is the foundation for smart, forward-looking decisions. Instead of guessing what might work next year, you can see exactly what did work. It’s the difference between navigating with a rough sketch and having a satellite map showing every twist and turn of the road behind you.

Your key financial reports—the Profit and Loss Statement, Balance Sheet, and Cash Flow Statement—each offer a unique window into your business. When you look at them together, you can uncover some powerful insights to drive growth. It's a bit like how a doctor uses different diagnostic tools to get a full picture of your health.

Start by looking for trends and patterns in your data:

Your year-end reports are the most honest feedback you'll ever get. They cut through assumptions and show you the unfiltered reality of your financial performance, giving you the clarity needed to plan effectively.

The real magic happens when you use this analysis to shape your strategy for the year ahead. This backward-looking data is your most reliable tool for forecasting and setting meaningful goals. It allows you to build a budget based on reality, not just optimism.

This principle of meticulous financial reporting is just as vital at a national level. For instance, UK public sector finances for July 2025 showed total debt at 96.1% of GDP, with net financial liabilities hitting over £2.5 trillion. That kind of accounting is essential for the government to manage such vast sums and make informed policy decisions.

For your own business, this data helps you set ambitious but achievable targets. By understanding your profit margins, you can make smarter decisions on pricing. By identifying your biggest expenses, you can spot opportunities to save money. For more ideas on this, our guide on tax advice for small businesses offers some practical tips.

Ultimately, turning your end-of-year accounting from a chore into a strategic review is how you turn historical data into future growth.

Even the most detailed guide can leave you with a few head-scratchers. When it comes to the nitty-gritty of year-end accounting, some questions pop up time and time again. Let’s tackle some of the most common queries from UK business owners to help you iron out the last few details.

If you’ve just set up a limited company, you get a bit of breathing room. Your very first set of accounts isn’t due until 21 months after your company was incorporated. This gives you a longer-than-usual accounting period to get your ducks in a row.

But don’t get too comfortable. Your first Corporation Tax return is due 12 months after your accounting period ends. It’s vital to get these dates lined up from day one to avoid any surprise penalties from HMRC.

Ah, the classic dilemma. The honest answer? It really depends on how complex your business is and how confident you feel with the numbers.

Going DIY with software: If your business is fairly simple – maybe you’re a sole trader with straightforward income and expenses – then modern accounting software like Xero or QuickBooks can be brilliant. They're cost-effective and put you in the driver's seat, but you have to be disciplined enough to keep your bookkeeping up to date.

Bringing in an accountant: As soon as your business starts to grow, or if you’re running a limited company, an accountant becomes a game-changer. They’re not just about compliance; a good accountant offers strategic tax advice that software simply can't, saving you a huge amount of time, stress, and potentially, money.

Many business owners find a happy middle ground. They use software for day-to-day bookkeeping and then hand everything over to an accountant for the final year-end submissions and some forward-thinking advice. It’s often the best of both worlds.

Think of it like this: software is a fantastic tool for recording what’s already happened. An accountant is an expert who helps you shape what happens next. They use that historical data to spot opportunities and steer you away from costly mistakes.

The secret to a stress-free year-end isn’t a secret at all: treat it as a year-round habit, not a last-minute panic. The single best thing you can do is start building good habits right now.

Make a non-negotiable rule to reconcile your bank accounts every single month. Use digital tools to snap photos of receipts the moment you get them, so you can ditch that frantic, end-of-year paper chase. When you keep your books clean and current all year, the final process transforms from a major headache into a simple review.

At GenTax Accountants, we blend expert knowledge with smart technology to make your end-of-year accounting feel effortless. Let us handle the complexities so you can stay focused on growing your business. Explore our services and get started today at https://www.gentax.uk.