When people talk about end of the year accounting, they're really talking about the process of double-checking, squaring up, and verifying every financial transaction from the last financial year to get the final reports ready. For most UK businesses, this is a make-or-break time of year. It’s all about getting your records in order, finalising the books, and prepping your tax submissions to keep everything accurate and compliant with HMRC.

Honestly, the secret to a smooth and stress-free financial close isn't some magic formula; it's just getting a head start well before any deadlines are breathing down your neck.

The financial year-end doesn't have to be a mad scramble of late nights and rising panic. The key to a seamless closing process is all in the preparation. It’s not about a frantic sprint in the final weeks, but about consistently building a solid foundation of organised records and clear processes throughout the entire year.

I often tell clients to think of it like building a house. You wouldn't dream of putting up walls without first laying a strong, level foundation. In accounting, your data integrity is that foundation. Get this right from the start, and the whole structure won't wobble when it's time to file.

First things first: you need a thorough collection of all your financial documents. And I mean everything—every single sales invoice, purchase receipt, and expense claim needs to be accounted for. Forgetting even small transactions can create inaccuracies that quickly snowball into much bigger problems.

Picture a growing e-commerce store. Over a year, they'll rack up hundreds of supplier invoices, software subscription receipts, and shipping fee statements. If these are just left languishing in an email inbox or a random physical folder, the year-end process turns into a painful treasure hunt.

A simple digital filing system can make a world of difference. Create dedicated folders for each month, and within those, categorise everything:

This methodical approach means that when you need a specific document, you know exactly where to find it. Trust me, it saves countless hours of frustrating searching.

Once your documents are gathered and organised, the next crucial job is reconciliation. This is where you match the transactions in your accounting software with your bank and credit card statements. The goal is simple: make sure the numbers in your books perfectly match the numbers in your bank account.

Reconciliation is your best friend when it comes to catching errors. It can uncover all sorts of issues, from duplicate payments and missed invoices to, in some rare cases, fraudulent activity. Doing this monthly, rather than leaving it all to the year-end, transforms a massive project into a manageable routine. It also gives you a much clearer, real-time picture of your cash flow.

A consistent monthly reconciliation process is the single most effective habit a business can adopt for a stress-free year-end. It turns a monumental task into a series of small, manageable steps, ensuring accuracy and preventing last-minute surprises.

Before you even think about the final reports, a bit of prep goes a long way. This checklist covers the core tasks you'll want to tick off to make the whole process smoother.

Task AreaKey ActionsWhy It's ImportantDocument GatheringCollect all sales invoices, supplier receipts, and bank/credit card statements.Ensures no transactions are missed, preventing inaccuracies in your final accounts.Bank ReconciliationMatch all transactions in your accounting software to your bank statements.Catches errors like duplicate payments or missed invoices early on.Payroll FinalisationProcess final salaries, bonuses, and expense claims for all employees.Guarantees that your payroll records are complete and accurate for tax purposes.Stocktake (if applicable)Conduct a physical count of all inventory and value it correctly.Provides an accurate inventory figure for your balance sheet, affecting your asset valuation.Debtors & CreditorsChase outstanding customer payments and log all supplier bills.Gives a clear picture of what you're owed (accounts receivable) and what you owe (accounts payable).

Getting these basics sorted is the groundwork that allows your accountant—or a service like ours—to hit the ground running.

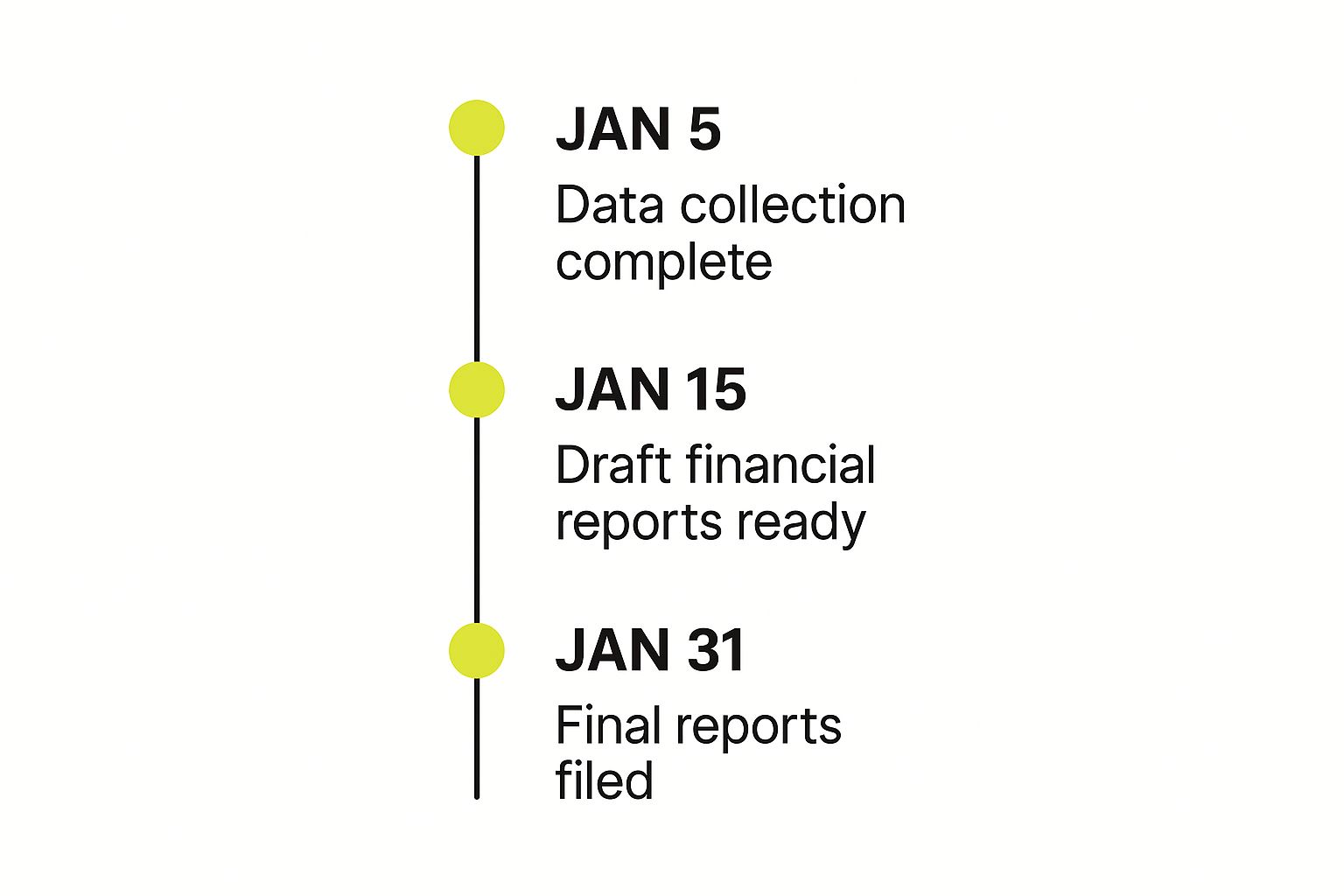

Waiting for HMRC deadlines to start looming is a recipe for disaster. Successful year-end accounting relies on setting your own internal deadlines well in advance. A clear timeline creates accountability and breaks the entire process down into achievable milestones.

Your timeline should map out target dates for key activities, such as:

By setting these internal goals, you build momentum and ensure all the necessary information is ready for your accountant. For businesses looking for expert guidance in preparing their statutory filings, GenTax offers comprehensive support on their company accounts services page. This kind of groundwork is exactly what enables a smooth transition from data collection to final report generation.

Your financial statements aren't just a box-ticking exercise for HMRC. They tell the story of your business's journey over the past twelve months—the wins, the challenges, and the bottom-line performance. Getting to grips with these reports is essential for smart end of the year accounting and planning what comes next.

The big three—the Profit and Loss, the Balance Sheet, and the Cash Flow Statement—work as a team. Each gives you a different angle on your financial health, but together, they paint the full picture you need to make genuinely informed decisions.

Let's think about a local café. By looking at these three documents, the owner doesn't just see if they made money. They see how they made it, where it all went, and what they've got left in the tank to grow the business.

Often called the P&L or Income Statement, this is the most direct of the three reports. It simply adds up all your income and subtracts all your expenses over your financial year to show your net profit or loss. It answers that one crucial question: "Is my business actually profitable?"

To get an accurate P&L, you have to be meticulous. Every income stream and every single business expense needs to be correctly categorised.

For our café owner, income is more than just coffee sales. It also includes things like:

On the flip side, expenses need to be broken down to see where the money is really going. This covers everything from the cost of coffee beans and milk (your Cost of Goods Sold) to rent, staff wages, utility bills, and marketing spend (your Operating Expenses). A well-kept P&L makes it obvious which parts of your business are driving profits and which costs are nibbling away at your margin.

While the P&L tells a story over a period of time, the Balance Sheet is a snapshot. It shows your company's financial position on a single day, usually the last day of your financial year. It all boils down to one simple but powerful formula: Assets = Liabilities + Equity. The two sides must always, well, balance.

Think of it as a financial photograph. It captures everything you own (Assets), everything you owe (Liabilities), and what’s left for the owner (Equity).

Let's break that down for our café:

The Balance Sheet is the first thing lenders and investors look at to judge your financial stability and whether you can handle your debts.

A healthy Balance Sheet does more than show you’re solvent. It proves your business has the financial resilience to handle economic curveballs and fund its own growth.

It's also worth looking at the bigger picture. For example, recent UK National Accounts data showed a tiny 0.1% growth in real GDP, suggesting the economy is a bit sluggish. Yet, the same data revealed a 1.9% increase in real households’ disposable income, thanks to wage rises. For a business owner finalising accounts, that's gold. It hints at potential shifts in customer spending, which directly impacts your forecasts. You can dig into the full report and learn more about these quarterly economic trends.

Finally, we have the Cash Flow Statement, which tracks the actual cash moving in and out of your business. It's a crucial reality check, because being profitable on your P&L doesn't guarantee you have cash in the bank. This statement explains the difference.

It’s usually split into three main activities:

Our café might have a great P&L but this report could show that cash is tight. Why? Perhaps they just spent a chunk of cash on a new outdoor seating area (an investing activity) or made a big loan repayment (a financing activity). This is the kind of insight you absolutely need to manage your money day-to-day and avoid any nasty surprises.

Let's be honest, for any UK business, juggling HMRC's deadlines is a non-negotiable part of end of the year accounting. Getting these dates wrong isn't just a minor admin headache; it can quickly spiral into automatic penalties, interest on late payments, and the kind of attention from HMRC that nobody wants.

Staying on the right side of the tax authorities is all about knowing exactly what's due, and when.

A common tripwire for many business owners is the sheer variety of deadlines. There's no single, universal calendar. VAT, PAYE, Self Assessment, and Corporation Tax all march to the beat of their own drum, each with unique filing rhythms you need to keep up with all year round.

Getting your head around the main deadlines is the first step to a stress-free year-end. A simple oversight can be surprisingly expensive – late filing penalties for Corporation Tax start at a punchy £100 and climb steeply the longer you delay.

To help you stay organised, here’s a quick overview of what you’ll be dealing with.

Keeping track of multiple tax obligations can be a challenge. This table breaks down the essential filing and payment dates you need to know.

Tax TypeFiling DeadlinePayment DeadlineCorporation TaxWithin 12 months of your company's accounting period end.9 months and 1 day after your accounting period end.Self AssessmentMidnight on 31 January for online returns.Midnight on 31 January for the previous tax year.VATUsually 1 month and 7 days after the end of the VAT period.The same day as the filing deadline.PAYEOn or before each payday (via RTI submission).22nd of the following month (19th for postal payments).

This table provides a clear snapshot, but remember that the specifics can vary based on your business structure and circumstances. Always double-check what applies to you.

One of the most crucial distinctions that catches out countless directors is with Corporation Tax. You have 12 months to file your Company Tax Return (CT600), but the deadline to actually pay your tax bill is much sooner – typically 9 months and one day after your year-end.

For sole traders and directors filing a personal tax return, the big one is 31 January. That’s your final chance to file online and settle up any tax you owe.

As you can see, the window between gathering your final year-end numbers and hitting that all-important January filing date is incredibly tight. It's a sprint, not a marathon.

Hitting the deadline is only half the battle. The information you submit has to be spot on. This is the whole idea behind HMRC's Making Tax Digital (MTD) initiative – they want to minimise errors by making sure businesses keep digital records and use approved software to file.

For sole traders and landlords, getting to grips with this digital shift is now essential. We've put together a detailed guide to help you understand the new rules, and you can learn more about Making Tax Digital for Self Assessment here. It’s a clear signal of HMRC's direction towards greater accuracy and transparency.

Staying organised is the cornerstone of HMRC compliance. It's not just about avoiding penalties; it's about maintaining a clean, transparent financial record that builds trust with tax authorities and stakeholders alike.

Ultimately, solid preparation is your best defence against compliance headaches. This is where a service like GenTax really makes a difference. We manage the entire process, making sure your records are meticulously kept and that every submission is filed correctly and on time.

By pairing expert oversight with smart, efficient systems, we take the anxiety and guesswork out of your HMRC obligations. It frees you up to focus on what you do best: running your business.

Beyond just ticking the compliance boxes, your end of the year accounting is genuinely the best chance you have to legally and proactively lower your tax bill. This isn’t about dodgy loopholes; it’s about making smart, strategic decisions before your financial year officially slams shut. Think of it as actively steering your finances, not just reporting on what’s already happened.

A classic mistake I see all the time is business owners treating tax planning as an afterthought—something they get to once the numbers are all in. The real savings, though, come from the moves you make in that final quarter. By looking ahead, you can make savvy choices about spending, investments, and expenses that will directly improve your bottom line.

One of the most powerful tools in the shed for UK businesses is the Annual Investment Allowance (AIA). This lets you deduct the full value of qualifying plant and machinery from your profits before tax. With the permanent AIA limit set at a very generous £1 million, it’s a massive opportunity to invest back into your business while slashing your tax liability.

Timing is everything here. If you’ve been mulling over buying new equipment—whether it’s new laptops, machinery, or even a company vehicle—pulling the trigger before your year-end can be a very shrewd move.

Take a small graphic design agency, for instance. They might be planning to upgrade their computer systems but could easily put it off until the new financial year. However, by bringing that purchase forward, they can claim the full cost against the current year's profits. This could lead to a substantial tax saving that gives their immediate cash flow a healthy boost.

Strategic asset acquisition isn't just an operational decision; it's a core tax planning strategy. By aligning major purchases with your year-end, you can turn necessary investments into immediate tax relief.

For limited company directors, popping money into a pension via the company is an incredibly tax-efficient way to get profit out of the business. These employer contributions are usually an allowable business expense, which means they reduce your company's profit and, as a result, its Corporation Tax bill.

The rules are different from personal contributions. The company can contribute up to the annual allowance (currently £60,000 for most people) as long as the payment passes the 'wholly and exclusively' test for business purposes. It’s a complete win-win: you’re building your personal retirement pot while simultaneously cutting your company's tax burden.

Honestly, it’s a far smarter method than just drawing a higher salary, which would get hit with both employer's and employee's National Insurance, plus Income Tax.

This one might sound obvious, but you would be absolutely amazed at how many legitimate business expenses get missed. A proper end-of-year accounting review involves a fine-tooth comb approach, making sure every single pound spent to generate profit is claimed.

Some of the most commonly overlooked expenses include:

Let's say you're a freelance consultant. You might pay for an annual software subscription every January. By simply renewing it in December before your year-end, you can claim that expense against the current year's income. Small tweaks like this, when you apply them across the board, create some serious savings. For more ideas, our guide on tax advice for small businesses has plenty of other tips.

For directors of limited companies, finding that sweet spot between salary and dividends is a classic year-end tax planning puzzle. The goal is simple: get profits out of the company in the most tax-efficient way you can. The usual playbook involves paying a small salary up to the National Insurance threshold, then taking the rest as dividends.

This strategy works so well because dividends aren't subject to National Insurance, and they're taxed at lower rates than salary income. Taking a moment to review this balance before the year closes ensures you’ve squeezed every last drop of value out of your personal tax-free allowances and the dividend allowance.

This kind of personal planning is part of a bigger picture. Look at the UK's savings habits, for example. In the 2022-2023 tax year, subscriptions to tax-efficient Adult ISAs climbed to 12.4 million. It shows people are actively using government schemes to manage their personal tax, a trend that's important to be aware of. Proactive planning, for both your business and yourself, is what turns a good year-end into a great one.

Once the final returns are filed and you’ve clicked submit, it's tempting to shove all that paperwork in a drawer and forget about it. Job done. But your completed end of the year accounting documents are much more than a box-ticking exercise for HMRC; they're a goldmine of information.

Treating this data as a historical record is a missed opportunity. The real magic happens when you use it to look forward, transforming those numbers into a proper roadmap for the year ahead. This is what separates businesses that just get by from the ones that genuinely grow. It all comes down to asking the right questions.

Your Profit and Loss (P&L) statement is the best place to start. Don't just glance at the net profit at the bottom. The real story is in the details, showing you what’s truly driving your business forward.

Take a hard look at your revenue streams. Which services or products actually brought in the best margins? A digital marketing agency, for instance, might find that big, one-off web design projects look great on paper, but it’s the smaller, monthly SEO retainers that are far more profitable over a twelve-month period. That's a massive clue about where to focus your sales efforts next year.

At the same time, you need to hunt for 'cost creep'. Have your software subscriptions quietly spiralled? Did a key supplier hike their prices without you really noticing? Spotting these slow leaks allows you to take action, whether that's renegotiating a contract or switching to a cheaper alternative.

If the P&L tells a story, the Balance Sheet gives you a powerful snapshot of your company's financial stability right now. It lays out what you own (assets) and what you owe (liabilities), giving a crystal-clear picture of your solvency. This is the report you need when you're thinking about making any major investments.

Ask yourself a few honest questions while you review it:

Imagine a small construction firm whose Balance Sheet shows that most of its asset value is tied up in old, tired machinery. That data makes a rock-solid case for investing in newer, more efficient equipment that will pay for itself through increased productivity.

Your year-end figures are the most reliable source of truth you have. Using them to build your next budget and forecast isn't just good practice—it's the foundation of sustainable financial strategy.

Now that you have a firm grip on your past performance, you can build a budget for the coming year that’s actually based on reality. Instead of just guessing, your P&L gives you a solid baseline for projecting your income and outgoings.

Break it down month by month. Be sure to factor in things you already know are coming, like planned price rises, a new hire starting in spring, or that big marketing push you’ve scheduled for autumn. This detailed approach helps you see the financial peaks and troughs before they happen.

From this budget, you can create a cash flow forecast. For any small business, this is arguably the single most important planning document you can have. It helps you answer critical questions like, "Will we have enough cash to make payroll in six months?" or "When’s the best time to afford that big purchase?" Having that kind of foresight lets you navigate the year with confidence, not anxiety.

Keeping this level of financial clarity all year round is tough, but it's where ongoing support really pays off. If you're looking to turn financial data into actionable strategy, see how GenTax's ongoing bookkeeping services can provide the real-time insights you need to make smarter decisions.

Even with the best prep in the world, the end of the year accounting process throws up curveballs. Getting these final details right is what separates a smooth, stress-free close from a frantic scramble.

We get asked a lot of the same questions this time of year, so we’ve pulled together some of the most common ones. Our goal is to give you clear, straight-up answers so you can wrap up your books with confidence.

Honestly, the biggest pitfall we see is messy record-keeping. Trying to hunt down missing receipts or make sense of unreconciled bank statements in the final stretch is a nightmare. It’s a surprisingly common problem that causes unnecessary stress and costly errors.

Another frequent slip-up is miscategorising expenses. For example, booking a hefty equipment purchase as a day-to-day expense instead of a capital asset can completely skew your profit figures. It also means you could miss out on valuable capital allowances.

And, of course, there’s the classic mistake of leaving it all too late. What should be a manageable process turns into a mad dash against the clock.

Legally, yes. As a limited company director, you can prepare and file your own statutory accounts and tax returns. The real question isn't can you, but should you?

Company accounts have to be prepared according to very specific UK accounting standards. A simple mistake could lead to a rejection from Companies House or, much worse, an investigation from HMRC.

The whole process is complex. Every hour you spend trying to get your head around accounting rules is an hour you’re not spending on growing your business. Using a professional accountant or a service like GenTax ensures everything is compliant, accurate, and tax-efficient. In our experience, the savings often outweigh the fee.

Your time is one of your business's most valuable assets. Investing in professional accounting support frees you to focus on growth, confident that your compliance and tax obligations are being managed expertly.

Once you’ve hit 'submit' with HMRC and Companies House, you’re not quite done. HMRC is very clear about how long you need to keep your financial records. For a limited company, you’re required to hold onto them for at least six years from the end of the financial year they relate to.

This isn’t just your final accounts summary, but all the paperwork that backs it up:

Ready to take the stress out of your end-of-year accounting? GenTax Accountants combines expert advice with smart technology to provide a seamless, fixed-price service that keeps you compliant and tax-efficient. Visit us online to book your free consultation today.