Using AI for your VAT, PAYE, and payroll isn't just a clever trick; it’s a powerful way to slash your administrative risk. Tools like QuickBooks and Xero have built-in, HMRC-friendly automations that catch anomalies before they snowball into costly errors, ensure calculations are spot on, and automate tedious data entry. This isn't about replacing people—it's about minimising human mistakes and winning back your time.

Let's be honest: keeping up with VAT, PAYE, and payroll rules feels more complicated by the day. For so many UK businesses, what should be straightforward financial admin has become a major headache, pulling focus away from actually growing the business. The pressure to get it right is immense, and the consequences of getting it wrong can be severe.

This shift towards digital, while a good thing overall, brings its own hurdles. Manual data entry is still the number one culprit behind errors that can quickly escalate into serious compliance problems. One tiny typo in a VAT return or a simple miscalculation on a PAYE submission is all it takes to trigger an HMRC enquiry, leading to fines and a lot of sleepless nights.

The sheer administrative load of staying compliant is staggering. Business owners and their teams pour countless hours into repetitive tasks that are far better suited to a machine.

Think about it. Are you still:

These jobs aren't just time-sinks; they're magnets for risk. The threat of human error hangs over every single spreadsheet and manual calculation, just waiting for a moment of distraction.

The real cost of manual tax admin isn't just the hours you lose—it's the ever-present risk of non-compliance. A single mistake can cost you more in penalties than a year's worth of accounting software. That makes automation an essential investment, not a luxury.

HMRC is pushing hard for digitalisation, and it's fundamentally changing how businesses handle their finances. Initiatives like Making Tax Digital (MTD) are leading the charge, making digital records and software-based VAT submissions mandatory. The adoption has been swift; in the 2024-2025 fiscal year, over 83% of VAT claims were filed digitally. This isn't a future trend; it's happening right now.

This is exactly where AI-powered accounting tools come in. They aren't some far-off, futuristic concept but an essential partner for today's business. We’re here to show you how to use the AI that’s already inside platforms like QuickBooks and Xero to cut through the complexity.

If you’re getting ready for the next wave of changes, you might find our guide on Making Tax Digital for Self Assessment a useful starting point.

The term ‘AI’ can sound a bit intimidating, but inside your accounting software, it’s really all about making your day-to-day tasks simpler, faster, and much more accurate. Forget the sci-fi stuff; the real power of AI for VAT, PAYE, and payroll is in the practical features quietly working away to cut down your administrative risk.

At its heart, the AI in platforms like QuickBooks and Xero is built on machine learning. This simply means the software learns from how you work. Every time you categorise an expense or match up a payment, the system is watching and remembering. Before long, it starts to anticipate what you’re going to do and automates those repetitive jobs with pinpoint accuracy.

Let's say you regularly buy fuel from the same petrol station. The first couple of times, you manually categorise the receipts as 'Vehicle Expenses' for your VAT records. The software picks up on this pattern. Soon enough, it will automatically suggest that same category for any future payments to that supplier, saving you a click every single time.

One of the biggest game-changers AI brings to the table is intelligent bank reconciliation. Instead of you having to manually tick off hundreds of lines on a bank statement against your invoices and receipts, the software does the heavy lifting for you.

It scans all the transaction details—the amount, date, and reference—to find and suggest matches automatically. This feature alone turns one of the most tedious bookkeeping jobs into a quick review process.

This kind of automation dramatically reduces the chance of human error. A miscategorised expense can easily lead to an incorrect VAT claim, but by learning from your own correct entries, the AI helps keep your books accurate. To get a better handle on the tech behind this, it's worth understanding how an AI agent for accounting operates.

AI also helps you manage the money coming in and going out. When a supplier invoice lands in your inbox, tools with Optical Character Recognition (OCR) can scan the document, pull out key details like the supplier name, invoice number, and amount, and then pre-populate a bill for you to approve. Easy.

The benefits are particularly clear when it comes to payroll, a critical area for staying on the right side of HMRC.

Think of AI as a second pair of eyes on your payroll. It can flag an unusually high salary payment or spot a duplicated expense claim, prompting a human review before a costly mistake is made. This is one of the most fundamental ways AI helps reduce your admin risk.

For startups still weighing up their options, features like these are a massive plus. It's a good idea to explore a comparison of the best cloud accounting software for startups to see which platform best suits your automation needs. At the end of the day, these smart features deliver real, tangible results: less time spent on data entry, far fewer errors, and a much clearer picture of your finances.

Right, let’s move from theory to practice. This is where you’ll see the real power of using AI for your VAT, PAYE, and payroll. Getting these automations set up in QuickBooks or Xero isn't just about flicking a switch. It’s a case of carefully building a workflow that’s robust, reliable, and completely compliant with HMRC’s rules. This is your opportunity to build a system that actively cuts down your admin risk from day one.

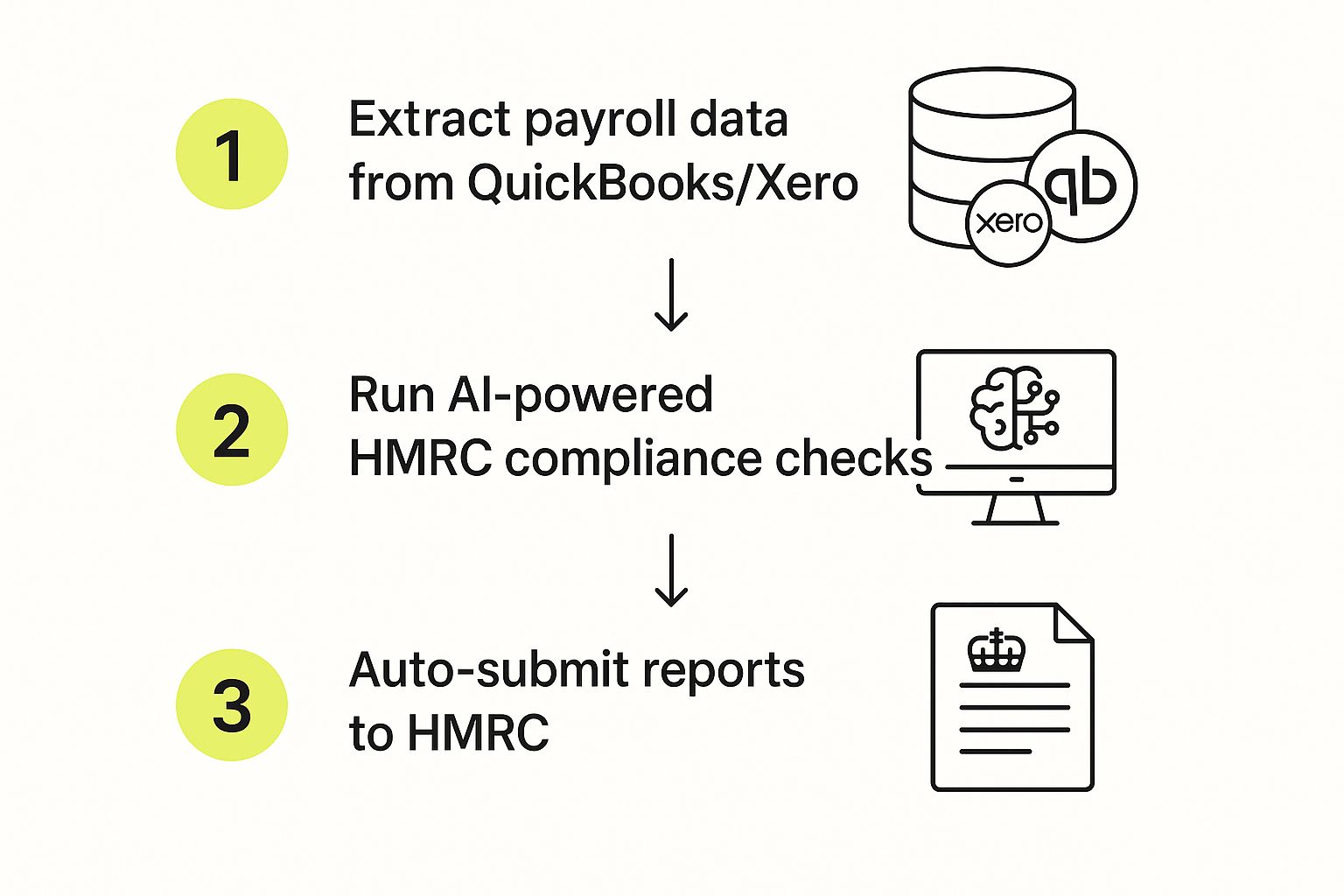

The first job is to connect your accounting software directly to HMRC's systems. This is a must-have for Making Tax Digital (MTD) for VAT, as it lets your software fire off returns directly without you having to manually upload files. Once it’s linked up, the platform can pull the data it needs, fill out the VAT return, and have it ready to submit with just a couple of clicks for your final sign-off.

This image gives you a good idea of the process, from pulling the data all the way through to HMRC submission.

The crucial thing to grasp here is how AI works as a compliance filter. It runs checks over your data before it ever gets near HMRC, which dramatically lowers the chance of costly errors slipping through.

Your payroll module is where AI can have the biggest impact, both on your workload and your risk profile. Get the configuration right, and every single payslip will automatically calculate the correct PAYE tax and National Insurance contributions using the latest HMRC rates.

Here’s what you need to nail for a successful setup:

These kinds of automations are becoming essential for managing UK payroll and PAYE, particularly for slashing admin risks. The move towards automated PAYE has already made a huge difference; the PAYE tax gap for small businesses has shrunk by two-thirds in recent years as more companies get on board with software like QuickBooks and Xero.

Making a successful switch is about more than just the technical setup; it demands a bit of careful planning. A classic mistake is to ditch the old system too quickly. My advice? Run your old payroll system alongside the new one for the first month. This way, you can compare the outputs and confirm every calculation is identical, giving you total peace of mind before you commit fully.

Crucial Checkpoint: Always, always verify your opening balances when you move to a new system. If your starting figures for things like outstanding VAT liabilities or employee loan balances are wrong, it will throw off every automated report from then on. Get this right, and everything else tends to fall into place.

If you’re interested in the broader picture of how AI can help with your admin, it's worth exploring different methods for streamlining business processes using AI. While you can manage this process yourself, getting it right is paramount. If you need an expert eye on it, our team is here to help you navigate the complexities of https://www.gentax.uk/services/vat-returns.

Once your basic automations are in place and ticking over nicely, you can start to think bigger. We're moving beyond simply processing transactions and into the realm of proactively managing financial risk. This is where using AI for VAT, PAYE, and payroll really shows its worth. It’s all about using the data your system is already collecting to make smarter, more strategic decisions that protect your business for the long haul.

This direct line to HMRC isn't just for show; it highlights the digital-first approach now demanded for UK tax compliance. It makes automated systems more crucial than ever. Thankfully, the tools baked into platforms like QuickBooks and Xero are built from the ground up to meet these tough digital standards without you breaking a sweat.

Honestly, one of the most powerful features you can tap into is using AI-driven insights to forecast your future tax liabilities. Instead of getting caught off guard by a massive VAT bill, your software can crunch the numbers from historical data and current sales to predict what you'll owe down the line.

This gives you a vital runway to manage your cash flow properly, making sure you have the funds ring-fenced when HMRC comes calling.

Picture this: the AI spots a seasonal spike in sales based on last year's performance. It can then project a proportionally higher VAT liability for the next quarter. This kind of foresight lets you plan your finances instead of constantly reacting to them.

Perhaps the single greatest benefit of a properly automated system is the digital audit trail it creates. It’s always on. Every single transaction, invoice, and payroll run is logged with a timestamp and user details, becoming your definitive source of truth and your best line of defence during an HMRC inquiry.

This level of digital record-keeping isn't just good practice anymore—it's fast becoming a necessity. HMRC's new Guidelines for Compliance (GfC13) specifically call out the critical role of automation in managing VAT. In fact, manual processes are now seen as inherently high-risk, so having a solid digital trail is essential. You can get a deeper understanding of how HMRC is tightening its VAT reporting standards and why this shift is happening.

Beyond just looking ahead, AI can act as a vigilant watchdog over your day-to-day accounts. It's brilliant at spotting irregularities that a human, no matter how diligent, could easily miss. This dramatically cuts down the risk of both internal mistakes and external fraud.

Think about these real-world examples:

These smart checks shift you from a reactive to a proactive mindset with your finances. By getting these capabilities working for you, you’re not just 'doing the books'; you’re building a truly resilient financial operation. For businesses wanting to take this a step further, our experience in technology transformation can map out a clear path forward.

Jumping into automation is a brilliant move, but it's important to remember that technology isn't a magic wand. When you're using AI for VAT, PAYE, and payroll, knowing where things can go wrong is half the battle. Just trusting the system blindly without getting to grips with its limits is the quickest way to turn a time-saver into a source of expensive mistakes.

One of the biggest traps I see is the "set it and forget it" mindset. A business owner sets up their bank rules in Xero or QuickBooks and just assumes every single transaction will be categorised perfectly from then on. But things change—you start buying from new suppliers, or have different types of expenses crop up. An old, overly broad rule can easily miscode these, leading to a real mess with your VAT claims.

Another classic slip-up happens right at the beginning. If you get your tax codes wrong during setup, the AI will diligently copy that mistake across hundreds of transactions. This gets particularly dicey when you're dealing with the finer points of UK VAT.

A perfect example is the common confusion between 'zero-rated' and 'exempt' supplies. On the surface, they look the same because you apply 0% VAT. But for your VAT return, they're worlds apart.

If you accidentally tell your software an exempt supply is zero-rated, the AI might wrongly include the input VAT in your reclaim calculation. Suddenly, you've over-claimed VAT—a serious compliance breach that HMRC will not look kindly upon.

The golden rule of automation is simple: trust, but verify. Treat your AI like a very keen but very junior accountant. It needs a bit of supervision, especially when it's just starting out. Going over the first few automated VAT returns with a human eye is non-negotiable; it's the only way to be sure the system has learned the unique quirks of your business.

To avoid falling into these traps, you need to actively manage your automation, not just switch it on and walk away.

Here’s how you can stay on top of it:

By taking these small, consistent steps, you'll build real confidence in your system. You’ll move from simply using a tool to mastering it, making certain your HMRC-friendly automations are genuinely cutting your admin risk, not adding to it.

Switching to a more automated way of handling your finances is a big step, so it’s only natural to have a few questions. Let's tackle some of the most common queries we hear from business owners about using AI for their VAT, PAYE, and payroll.

The number one concern? It’s always data security. And rightly so. The good news is that platforms like QuickBooks and Xero pour huge resources into bank-grade security to keep your financial information locked down. They use top-tier encryption and multi-factor authentication, making sure only authorised people can get near your data. Plus, their systems are built from the ground up to comply with UK data protection laws.

Another common question is about the time it takes to get everything set up. While there’s always a bit of a learning curve, you might be surprised at how quickly it all comes together. The AI is designed to learn from your existing books, so a lot of the initial "training" is done automatically when you link your bank accounts and pull in your transaction history.

Your financial data is some of the most sensitive information you have, and the reputable cloud accounting platforms treat it that way. Security isn’t just a feature they bolt on at the end; it's right at the core of what they do.

Here’s a quick breakdown of the protections in place:

This is a really important point. No system is ever going to be 100% perfect, and you should think of the AI as a powerful assistant, not a complete replacement for human judgement.

If the software miscategorises a payment or gets a calculation wrong, the legal responsibility for what gets submitted to HMRC still rests with you, the business owner.

This is exactly why having a human review process is non-negotiable. The best way to work is to treat the AI-generated reports—whether it's a VAT return or a payroll summary—as a very accurate first draft. Your job is to give it a final, common-sense check before you hit 'submit'. For a deeper look at how we build these essential checks into our processes, you can learn about our expert-led payroll services.

The AI's job is to wipe out 95% of the tedious manual work and flag anything that looks out of place. Your job is to provide that final, critical 5% of human validation. This partnership between machine efficiency and human expertise is what truly cuts down administrative risk.

Once you get your head around these key ideas, you can bring AI into your VAT, PAYE, and payroll processes with a clear strategy, not apprehension.

Ready to transform your financial admin and reduce risk with expert guidance? Contact GenTax Accountants today to see how our tech-focused approach can support your business. Find out more at https://www.gentax.uk.