Professional accounting isn't just about filing your taxes once a year; it’s a crucial investment that can become a powerful tool for growing your business. It provides the financial clarity you need to make smart decisions, stay compliant with UK regulations, and keep your cash flow healthy. Think of it as upgrading from a basic paper map to a live GPS for your business journey.

Running a small business in the UK means navigating some seriously complex financial waters. Many owners try to juggle the books themselves, only to find that DIY accounting eats up precious time and opens the door to significant risks. It’s a familiar story: missed tax deadlines, messy financial data, and a nagging lack of insight that can stall growth and pile on the stress.

This is where bringing in a professional makes all the difference. An accountant is more than just a number-cruncher; they're a seasoned navigator for your business. Their expertise helps you steer clear of hidden financial icebergs, like unexpected tax bills or cash flow shortages, while spotting the clearest routes to sustainable growth. They can transform your accounting from a painful chore into your most valuable strategic asset.

To put this into context, let's look at the real-world hurdles that small businesses often face and how professional support offers a direct solution.

Ultimately, a good accountant helps you sidestep these common pitfalls, turning potential weaknesses into strengths and providing a solid foundation for growth.

A common pain point for entrepreneurs is getting stuck in a reactive cycle—only dealing with financial problems after they’ve already hit. A professional accounting partner helps you flip that script and get proactive. Instead of frantically digging through a shoebox of receipts come tax season, you’ll have clean, organised books all year round.

By outsourcing your accounting, you are not just offloading a task; you are investing in financial stability and peace of mind. This allows you to reclaim your time and focus on what you do best: running and growing your business.

This proactive approach is vital for survival and success. Small businesses are the backbone of the UK economy, with 5.45 million small enterprises making up over 99% of all businesses. Yet, many operate on shaky ground. For instance, a staggering 44% of UK SMEs have no commercial insurance, leaving them dangerously exposed. This highlights just how crucial sound financial management is, and professional accounting plays a key role in spotting and mitigating risks before they become disasters. You can discover more insights about UK business statistics on money.co.uk.

Making this shift empowers you to make smarter decisions based on accurate, real-time data. You can confidently plan for expansion, manage your stock levels, and secure funding—all because you have a crystal-clear picture of your financial health. Engaging an expert ensures your business isn't just compliant, but also competitive and resilient for the long haul.

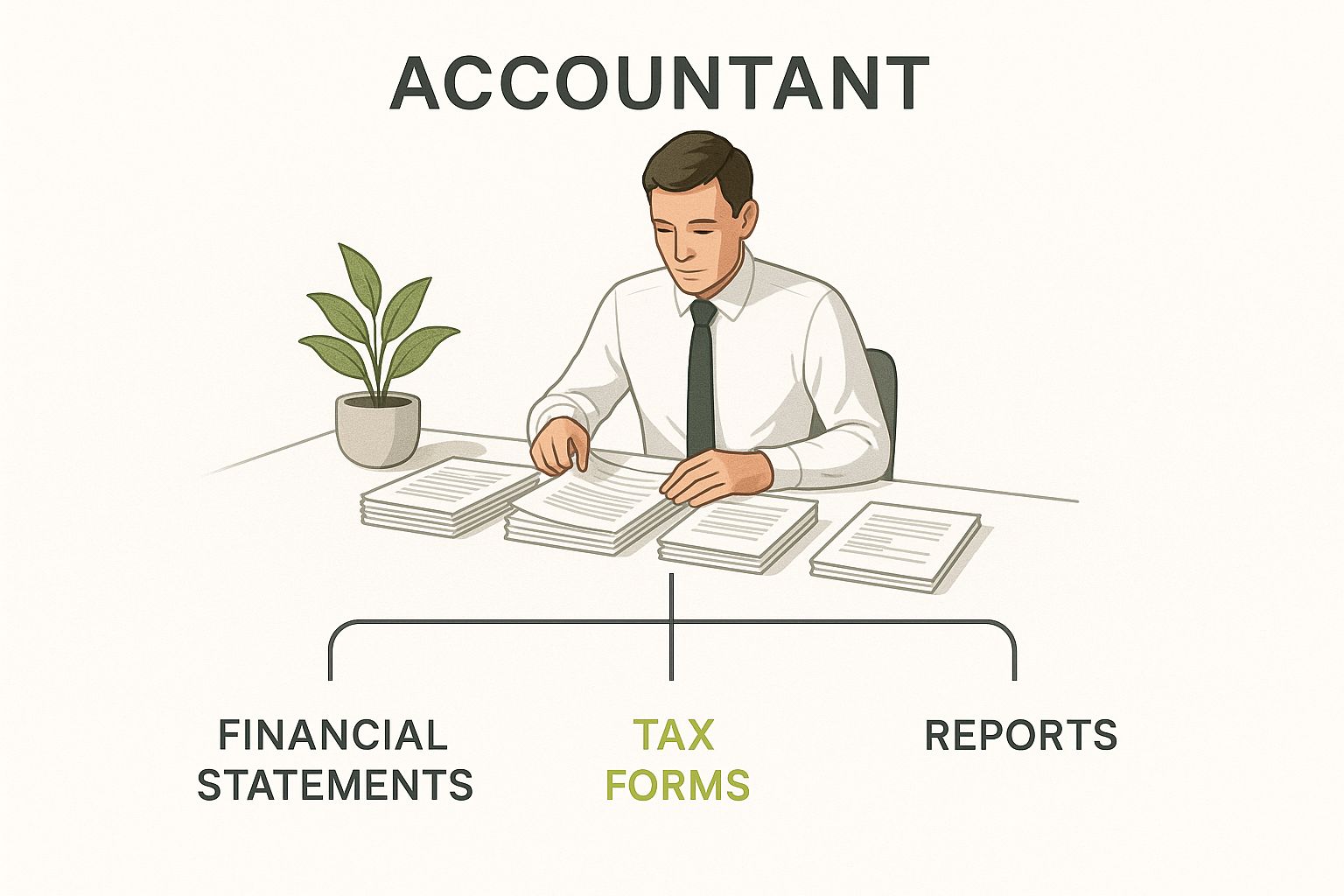

To build a business that can weather any storm, you need a rock-solid financial foundation. Think of professional accounting less as a single task and more as a system of interconnected services, where each one plays a distinct but crucial role. Nailing these four core areas gives you the clarity and control to handle challenges and jump on opportunities.

When you understand how these services fit together, you start to see the complete picture of your financial health. This infographic shows how a good accountant structures these functions to make sense of it all.

This organised approach turns what can feel like a mess of data into a powerful tool, showing how each service builds on the last to create a comprehensive financial system.

Bookkeeping is where all financial clarity begins. Think of it as the daily health diary for your business, meticulously logging every single transaction—every sale, every purchase, every payment. It’s the disciplined practice of recording your financial life as it happens.

Without accurate bookkeeping, everything else simply falls apart. Your tax returns become a dangerous guessing game, and your financial reports are practically useless. It’s the fundamental process that ensures every piece of data entering your financial system is correct, organised, and up-to-date.

A clean set of books is the single source of truth for your business finances. It provides the raw material from which all strategic insights are drawn, making it the most critical daily habit for financial health.

This non-negotiable task is the bedrock of reliable financial management.

If bookkeeping is the daily diary, tax preparation and planning is your annual health check-up and future-proofing plan rolled into one. This service goes far beyond just filling out forms for HMRC at the end of the year; it’s all about strategic foresight.

Effective tax planning means looking ahead to legally minimise what you owe. An expert will help you take advantage of every available relief, allowance, and credit, making sure you never pay a penny more in tax than you absolutely have to. This proactive approach can save your business thousands over the years.

Given how complex the UK tax system is, it’s no surprise that outsourcing has become standard practice. Data shows that 71% of small businesses outsource their tax preparation, and 30% bring in external help for strategic tax planning. It just goes to show how much value experts bring to the table when it comes to navigating the rules.

The moment you hire your first employee, payroll management becomes a critical function. Think of it as the engine that powers your team, responsible for making sure everyone is paid accurately and on time, every single time. It's a complex area, full of legal duties like calculating income tax and National Insurance, and managing pensions and statutory pay.

Mistakes in payroll can be incredibly costly. They don't just lead to unhappy employees; they can also attract hefty penalties from HMRC for non-compliance. Getting it right is absolutely essential for keeping team morale high and protecting your business.

A professional payroll service handles all these moving parts for you, including:

This frees you up from a time-sucking administrative headache, letting you focus on leading your team instead of getting bogged down in calculations.

Finally, with clean data from your bookkeeping and compliant tax and payroll processes, you can unlock the most powerful service of all: financial reporting and analysis. This is your business’s GPS, turning raw numbers into actionable insights that guide your most important decisions.

An accountant doesn’t just hand you a Profit & Loss statement; they help you understand what the numbers mean. They’ll analyse trends, highlight opportunities, and flag potential issues before they grow into serious problems. For instance, they might spot that your cost of goods sold is creeping up, prompting a review of your suppliers.

These reports help you answer the big questions:

This is where accounting stops being a chore and starts being a true strategic partner, giving you the intelligence you need to grow your business sustainably. You can explore the full range of accounting services available for your business to see how all these pieces fit together.

Once your core financial jobs like bookkeeping and tax filings are humming along smoothly, you can unlock the next level of value from accounting services for small businesses. This is where your accountant stops being a historian, just recording past events, and becomes a genuine strategic partner helping you shape the future.

These advisory services are all about looking forward. They turn your financial data from a rear-view mirror into a powerful tool for growth. This is what separates a standard number-cruncher from a true growth partner. Instead of just telling you where your money went, they help you decide where it should go next.

One of the most powerful advisory services you can get is cash flow forecasting. Think of it as a detailed weather forecast for your bank account. It uses your past performance and known future costs to project your cash position weeks, and even months, ahead. This helps you prepare for both sunny spells and potential storms.

Having this foresight is a game-changer. It means you can spot a cash surplus on the horizon and plan to use it for something productive, like a new marketing push or a piece of equipment you’ve had your eye on.

Crucially, it also warns you about potential shortfalls long before they become a crisis. This gives you plenty of time to arrange a line of credit or trim your spending to avoid sleepless nights.

A cash flow forecast is your financial early warning system. It replaces guesswork with solid predictions, letting you manage your money with confidence.

With this kind of clarity, you stop reacting to financial emergencies and start proactively managing your cash cycle. It ensures you always have the funds you need to operate smoothly and jump on opportunities when they pop up.

Beyond predicting cash flow, a good advisor helps with budgeting and financial strategy. This isn't about penny-pinching; it's about building a financial roadmap that’s directly linked to your business goals. It makes sure every pound you spend is working hard to push your business forward.

Your accountant will work alongside you to create a detailed budget that acts as a blueprint for your year. This involves setting realistic sales targets and smartly allocating your resources across the business, from marketing and sales to operations.

This strategic approach helps you:

This is a continuous loop of planning, measuring, and adjusting. Your advisor helps you understand why you might be off-track and refine your strategy, keeping your financial plan relevant as your business grows.

Ultimately, advisory services are about turning numbers into a story about growth. An experienced advisor helps you read between the lines of your financial reports. They can analyse profitability by product line, spot opportunities to improve your margins, and model the financial impact of big decisions, like hiring a new team member.

This kind of strategic input is priceless. For instance, an advisor might dig into your reports and find that 20% of your clients are actually generating 80% of your profit. This one insight could spark a major strategic shift, focusing your sales and marketing on finding more of these high-value clients.

That's how data-driven advice leads to real, tangible improvements in your business. These strategies become even more powerful when combined with smart tax planning. For a deeper dive, you can find helpful tax advice for small businesses in our detailed guide.

By linking your financial strategy with tax efficiency, you create a powerful engine for sustainable growth. You’ll know your business isn't just getting bigger—it's getting more profitable, too.

Picking a provider for accounting services for small businesses is a much bigger decision than just finding someone to file your tax return once a year. Think of it less like hiring a supplier and more like bringing on a financial partner who will get a front-row seat to your entire operation. It’s a choice that deserves real thought, looking past a simple price list to find someone who’s a genuine fit for where you want to take your company.

A great accountant acts as a trusted advisor, helping you steer through the inevitable challenges and spot opportunities you might otherwise miss. The wrong one? That can quickly lead to missed deadlines, flimsy advice, and expensive compliance headaches. Your mission is to find a partner who doesn't just see the numbers, but understands your industry and your vision for the future.

First things first: you need to verify their professional qualifications. Here in the UK, that means looking for accountants who are members of recognised professional bodies. This is your guarantee of their expertise, their commitment to ethical standards, and the fact they’re keeping their skills sharp.

A few key qualifications to look for include:

These letters aren’t just for show; they signify a serious level of training and a promise to uphold the highest professional conduct. Don’t ever feel shy about asking a potential firm about the qualifications of the specific person who will be managing your account.

Next up, dig into their experience within your specific industry. An accountant who lives and breathes eCommerce will instinctively get the complexities of inventory management and payment gateways. Likewise, one who specialises in construction will be an expert in things like the Construction Industry Scheme (CIS).

Choosing an accountant with experience in your niche is like hiring a guide who already knows the terrain. They can anticipate sector-specific challenges, identify relevant tax reliefs, and provide benchmarks that a generalist might overlook.

This kind of specialised knowledge is priceless. An industry expert will already be familiar with your key performance indicators, common financial hurdles, and the specific regulations you have to navigate. That lets them offer proactive, relevant advice that goes way beyond basic bookkeeping.

Modern accounting runs on technology. It is absolutely essential that your partner is fluent in the leading cloud accounting platforms like Xero, QuickBooks, and Sage. These tools are the bedrock of efficient collaboration and give you a real-time pulse on your finances.

A tech-savvy accountant will help you automate the grind of tasks like bank reconciliation and invoice processing, which frees you up to focus on what you do best. They should be able to get your systems set up properly, show you the ropes, and integrate other apps to create a seamless financial workflow. Their comfort with technology is a huge clue about their commitment to efficiency and providing you with up-to-the-minute data.

Finally, a strong accounting partnership is built on two things: clear communication and transparent pricing. As you have your initial chats, pay close attention to how they explain complex financial ideas. Do they use plain English, or are they hiding behind a wall of jargon? You need an advisor who can make the numbers make sense.

Be sure to ask about their communication style:

Just as important is a fee structure you can understand. Look for firms that offer fixed monthly pricing, as this helps you budget properly and avoids the shock of a surprise bill. This model also encourages you to pick up the phone with questions without worrying you’re on the clock. That open line of communication is vital for building a strong, lasting relationship.

And as your business grows, your needs will evolve—especially when you start hiring. To get ahead of the curve, you can read our guide on payroll services for small businesses to understand what that involves.

Switching accountants can feel like a massive job, but with a bit of prep work, it's a surprisingly quick and painless process. A well-organised transition sets the stage for a strong partnership from day one, making sure your new accountant can start adding value immediately.

Think of it like packing before you move house. The more organised you are upfront, the easier it is to unpack and get settled. The aim here is to keep disruption to a minimum and get you and your new advisor working together effectively from the get-go.

It really comes down to gathering the right documents, understanding their onboarding process, and ensuring a clean handover. Let’s break down the steps to make this change as seamless as possible.

Before your first proper meeting, your new accountant will need to get their hands on your historical financial data. This information gives them the context they need to understand your business's financial health, tax history, and where things currently stand. Getting these documents ready will dramatically speed things up.

It’s a good idea to create a digital folder and start gathering these key items:

A smooth handover is built on organised information. By preparing your key financial documents in advance, you empower your new accountant to get up to speed quickly, avoiding delays and unnecessary back-and-forth communication.

This preparation not only makes a great first impression but helps your new partner dive straight into providing valuable accounting services for small businesses without chasing down old paperwork. It's especially important for different business structures; you can learn more about the unique needs of the self-employed in our helpful guide for sole traders.

Once you’ve handed over the initial documents, the formal onboarding can begin. This is much more than a simple welcome call; it’s a structured introduction designed to align your goals and set clear expectations for how you’ll work together.

That first meeting is crucial. It’s your chance to discuss your business objectives, your biggest financial headaches, and what you’re hoping to achieve with their support. You’ll also nail down practical details like how often you'll communicate and when you'll receive reports.

A typical onboarding journey looks something like this:

This structured process ensures nothing gets missed and builds a solid foundation for your partnership.

Choosing the right accounting help for your business is a big decision, and it’s completely normal to have questions. Getting clear, straightforward answers is the best way to move forward with confidence, making sure you put your money into a service that genuinely helps you grow. This section tackles the most common queries we hear from entrepreneurs just like you, breaking down everything from costs to the roles different professionals play.

Our goal here is to demystify the whole process. Let's dive into the questions that are probably on your mind.

This is usually the first question business owners ask, and the honest answer is: it depends entirely on your needs. The cost of accounting services isn't a one-size-fits-all figure; it scales with the complexity of your business and how much support you're looking for. Think of it like vehicle maintenance—servicing a small car is always going to cost less than servicing a huge commercial lorry.

To give you a clearer picture, here’s a typical breakdown of monthly costs in the UK:

Always ask for a detailed, fixed-fee quote before you sign anything. This should clearly itemise every single service included, so there are no hidden charges or surprise bills down the line. Transparency is the bedrock of a good partnership.

So many business owners wonder if they're "big enough" to need an accountant. The best advice I can give is to get one on board much earlier than you think. Ideally, you should start talking to an accountant as soon as you register your business, especially if you’re setting up as a limited company.

Getting expert advice from day one helps you build a solid financial foundation and avoid common, costly mistakes. That said, there are also a few specific trigger points that scream, "it's time to bring in a professional":

Acting on these triggers stops small issues from snowballing into major headaches.

Accounting software is an incredibly powerful tool, but it's vital to understand its limits. Platforms like Xero and QuickBooks are brilliant for organising your financial data, automating invoicing, and tracking expenses. They are the digital filing cabinets and calculators of modern business.

But software only handles the "what"—it records the transactions you tell it to. It can't give you the "why" or the "what next." That's where a human expert comes in. An accountant interprets the data that the software organises.

Think of it like this: software can give you a map, but an accountant is the experienced guide who helps you read it, choose the best route, and navigate around unexpected roadblocks. They provide strategic tax planning, make sure you stay compliant with ever-changing rules, and translate your financial reports into actionable business advice. The best approach is always a combination of efficient software and the expertise of a professional accountant. For more on this, check out our guide on the best cloud accounting software for startups, which explores how these tools fit into a broader financial strategy.

This is a fantastic question because the two roles are distinct but work hand-in-hand. Knowing the difference helps you hire the right person at the right time.

A bookkeeper is all about the day-to-day recording of your financial transactions. Their job is to maintain accurate and up-to-date financial records—your "books." Their tasks include:

In short, a bookkeeper makes sure the data going into your financial system is clean, organised, and accurate.

An accountant, on the other hand, takes a higher-level, more strategic view. They use the organised data from the bookkeeper to perform more complex functions. These include:

Essentially, the bookkeeper manages the historical records, while the accountant interprets those records to help you plan for the future and grow your business. Many firms, including ours, offer both services for a seamless financial solution.

At GenTax Accountants, we provide the clarity and expert guidance you need to navigate these questions and more. Our dedicated team is here to help you build a strong financial foundation, so you can focus on what you do best. Discover how our accounting services can support your business growth today.